Does Analyst Turnaround Optimism And Portfolio Shifts Change The Bull Case For UnitedHealth Group (UNH)?

UnitedHealth Group Incorporated UNH | 277.26 | +1.20% |

- In recent days, analysts including Evercore ISI have reiterated positive views on UnitedHealth Group’s turnaround, highlighting 2026 as a transition year while investors await the company’s January 27, 2026 release of full-year 2025 results and 2026 guidance.

- Alongside this renewed analyst optimism, the pending sale of Optum’s UK arm and the appointment of former FDA Commissioner Dr. Scott Gottlieb to the board underscore how UnitedHealth is reshaping its portfolio and governance as it works through its Medicare and cost challenges.

- Against this backdrop of growing analyst confidence in a turnaround, we’ll examine how these developments may reshape UnitedHealth Group’s investment narrative.

These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

UnitedHealth Group Investment Narrative Recap

To own UnitedHealth Group, you need to be comfortable with a large, complex health insurer working through elevated Medicare costs and execution issues while retaining its scale advantages. The key short term catalyst is the 27 January 2026 update on full year 2025 results and 2026 guidance, and the recent analyst optimism does not materially change that, while the biggest near term risk remains higher than expected care utilization in Medicare and related margin pressure.

The most relevant recent announcement here is UnitedHealth’s plan to sell Optum’s UK operation to TPG, which would modestly simplify the portfolio while the company focuses on US Medicare and cost issues. For investors watching the January guidance closely, this move sits in the background, but it helps frame how management is concentrating attention and resources on the core areas that matter most for near term earnings resilience.

Yet behind the renewed analyst confidence, investors still need to be aware of the risk that Medicare care activity remains elevated and...

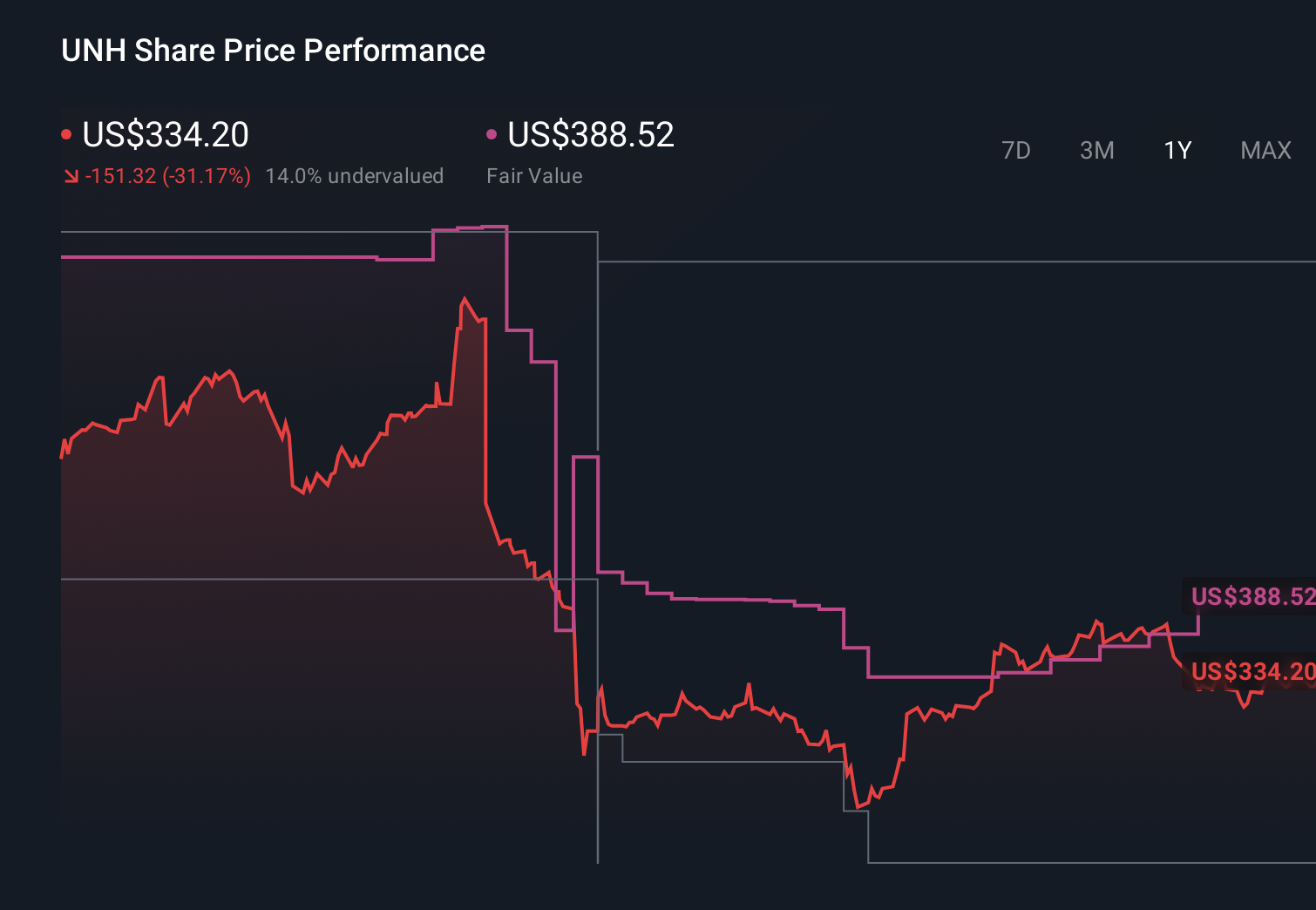

UnitedHealth Group's narrative projects $501.1 billion revenue and $20.0 billion earnings by 2028. This requires 5.8% yearly revenue growth and a $1.3 billion earnings decrease from $21.3 billion today.

Uncover how UnitedHealth Group's forecasts yield a $392.24 fair value, a 15% upside to its current price.

Exploring Other Perspectives

Across 88 fair value estimates from the Simply Wall St Community, views on UnitedHealth’s worth span roughly US$305 to US$821 per share. When you set those opinions against the current concerns about unexpected care activity in Medicare, it becomes clear why many market participants are approaching UnitedHealth’s recovery with their own time frames and risk tolerances in mind.

Explore 88 other fair value estimates on UnitedHealth Group - why the stock might be worth over 2x more than the current price!

Build Your Own UnitedHealth Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your UnitedHealth Group research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free UnitedHealth Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate UnitedHealth Group's overall financial health at a glance.

Ready For A Different Approach?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- AI is about to change healthcare. These 29 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've found 12 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.