Does ARKA-Focused Debt Reshaping Change The Bull Case For CACI International (CACI)?

CACI International Inc Class A CACI | 0.00 |

- CACI International recently completed additional debt financing, issuing US$500 million of unsecured 6.375% Senior Notes due 2033 and arranging US$800 million in incremental term loans, primarily to refinance credit facility borrowings used to acquire ARKA Group L.P.

- This combination of unsecured notes and secured term loans materially reshapes CACI’s capital structure, tying higher leverage directly to its ARKA acquisition and long-term government technology growth ambitions.

- We’ll now examine how this sizeable ARKA-related debt raise, and its shift between secured and unsecured borrowing, affects CACI’s investment narrative.

We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

CACI International Investment Narrative Recap

To own CACI, you need to be comfortable with a business tied closely to U.S. national security budgets and increasingly to higher-tech, acquisition-fueled growth like ARKA. The new US$500 million unsecured notes and US$800 million term loans materially lift leverage but mainly reshuffle how the ARKA deal is financed, so they do not change the core near term catalyst of converting large contract wins into earnings, or the key risk of heavy reliance on federal spending and contract timing.

The most relevant recent announcement here is CACI’s higher FY2026 guidance, with revenue now expected at US$9.3 billion to US$9.5 billion and net income at US$524 million to US$539 million. That outlook was issued before the latest ARKA related financing, so investors may want to watch how interest expense from the combined US$1.5 billion in senior notes and new secured term loans tracks against those profit expectations and any future guidance updates.

Yet even with these positive signals, investors should be aware that higher debt tied to ARKA could amplify CACI’s exposure to...

CACI International’s narrative projects $10.4 billion revenue and $634.1 million earnings by 2028. This requires 6.5% yearly revenue growth and about a $134.3 million earnings increase from $499.8 million today.

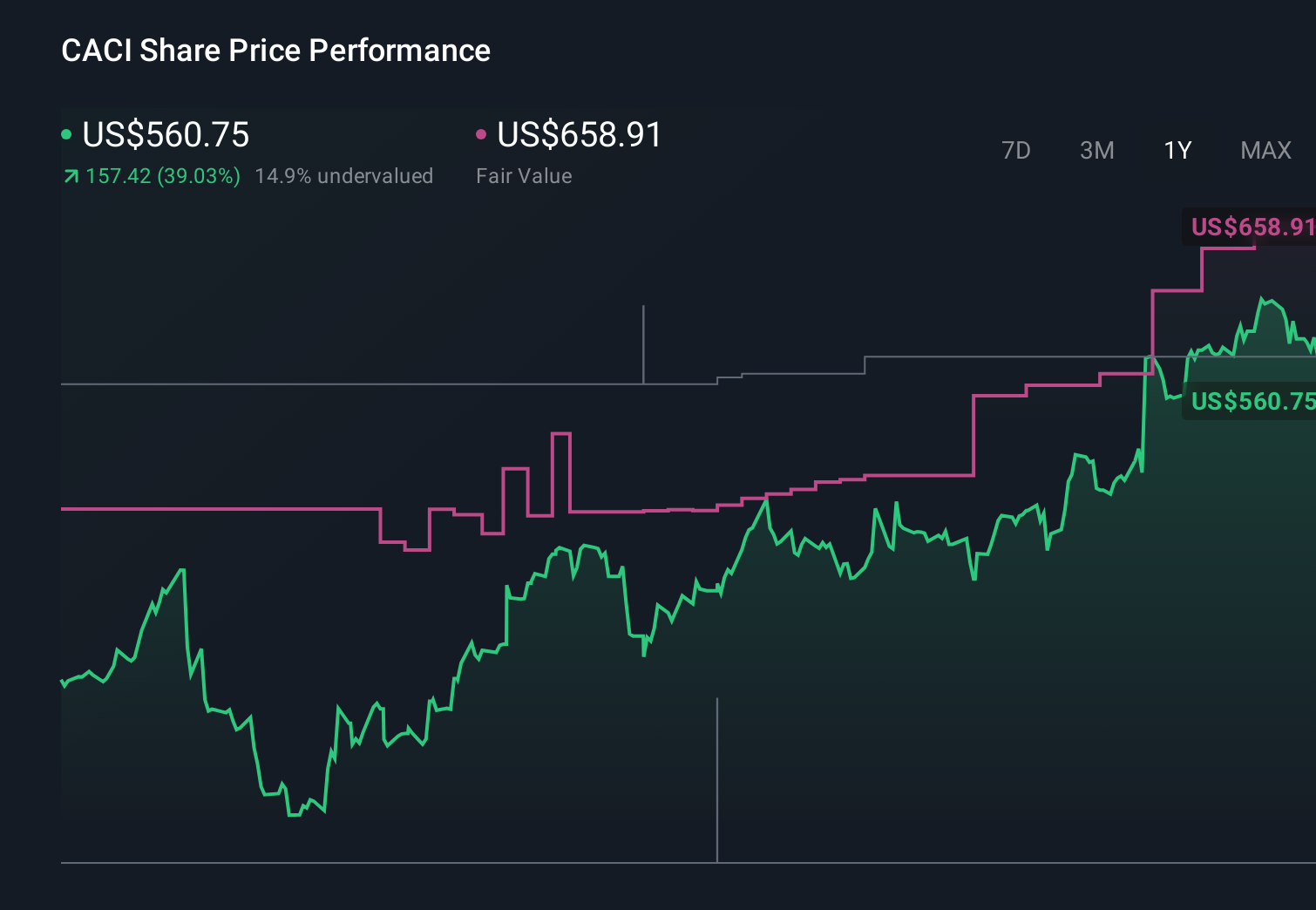

Uncover how CACI International's forecasts yield a $718.08 fair value, a 17% upside to its current price.

Exploring Other Perspectives

While baseline estimates already assumed steady growth, the most optimistic analysts saw revenue reaching about US$10.9 billion and earnings near US$684 million, so this new ARKA related leverage could either reinforce or challenge that more ambitious view of CACI’s ability to offset budget and automation risks with higher margin tech work.

Explore 4 other fair value estimates on CACI International - why the stock might be worth just $670.00!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your CACI International research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free CACI International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CACI International's overall financial health at a glance.

Interested In Other Possibilities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Find 49 companies with promising cash flow potential yet trading below their fair value.

- This technology could replace computers: discover 24 stocks that are working to make quantum computing a reality.

- AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.