Does Booz Allen (BAH) Joining the S&P MidCap 400 Change Its Government-Heavy Investment Narrative?

Booz Allen Hamilton Holding Corporation Class A BAH | 80.37 80.00 | +3.00% -0.46% Pre |

- Booz Allen Hamilton’s inclusion in the S&P MidCap 400 index, announced as part of a recent S&P indices rebalancing, has prompted large index-tracking funds to adjust portfolios to reflect the company’s new status.

- This index entry highlights how benchmark membership can influence trading activity and investor attention without any immediate change in Booz Allen’s underlying operations or contracts.

- We’ll now explore how Booz Allen’s S&P MidCap 400 inclusion may influence its investment narrative, particularly its government-focused revenue base.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Booz Allen Hamilton Holding Investment Narrative Recap

To own Booz Allen Hamilton, you need to believe in the durability of its government-focused consulting and technology business, especially in defense, AI, and cybersecurity. The S&P MidCap 400 inclusion mainly affects trading flows and visibility, but does not materially change the near term catalysts around federal technology spending or the key risk from budget-driven contract delays and civil funding pressure.

The recent Q2 earnings-driven share pullback, tied to weaker civil spending and budget cuts, is more directly relevant to the index news. It underlines how dependent the company’s results are on government budgets at a time when its new index status is drawing in fresh attention from benchmarked funds and reinforcing the focus on how quickly its large contract backlog converts to revenue.

Yet behind the index headlines, investors should be aware that heavy reliance on a limited set of government clients and evolving contract terms could materially influence...

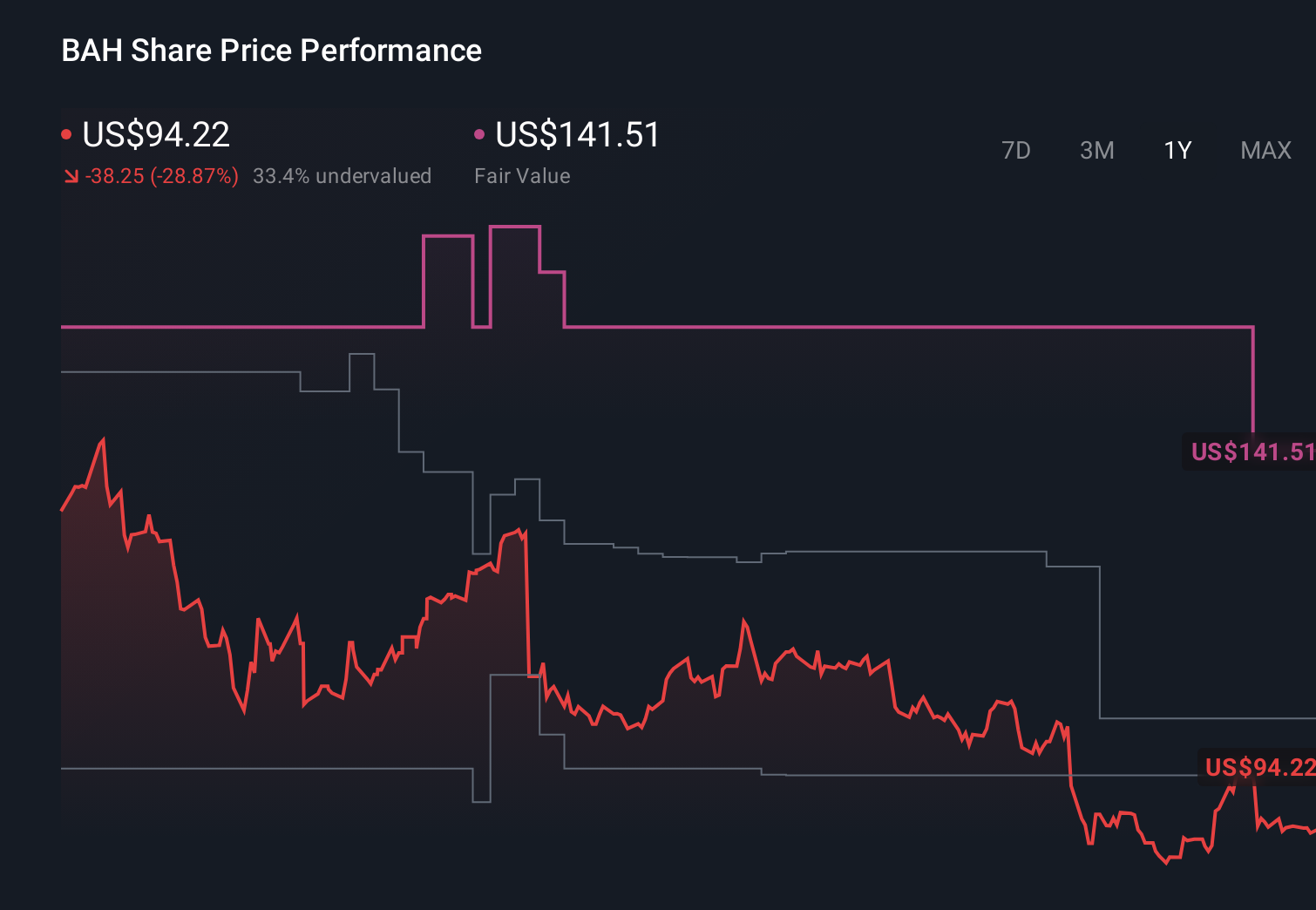

Booz Allen Hamilton Holding's narrative projects $13.5 billion revenue and $775.2 million earnings by 2028.

Uncover how Booz Allen Hamilton Holding's forecasts yield a $101.50 fair value, a 9% upside to its current price.

Exploring Other Perspectives

Eight fair value estimates from the Simply Wall St Community span roughly US$89 to about US$170 per share, showing how far apart individual views can be. When you weigh those opinions against Booz Allen’s dependence on timely government contract awards and budget decisions, it becomes clear why exploring several alternative viewpoints can reshape how you see the company’s prospects.

Explore 8 other fair value estimates on Booz Allen Hamilton Holding - why the stock might be worth as much as 82% more than the current price!

Build Your Own Booz Allen Hamilton Holding Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Booz Allen Hamilton Holding research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Booz Allen Hamilton Holding research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Booz Allen Hamilton Holding's overall financial health at a glance.

Seeking Other Investments?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- We've found 12 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.