Does CACI (CACI) Elevate Its Defense Edge With Dave Young’s Operational Playbook?

CACI International Inc Class A CACI | 0.00 |

- CACI International Inc. recently appointed Dr. Dave Young, age 45, as Executive Vice President and Chief Operating Officer, adding him to the executive leadership team reporting directly to the CEO after senior roles at Lockheed Martin, CAES, and Northrop Grumman.

- Young’s prior responsibility for a roughly US$7.00 billion national security space business and thousands of staff could meaningfully influence how CACI runs its operations and executes on complex defense and intelligence programs.

- Next, we’ll examine how Young’s deep national security and space-technology background may shape CACI’s existing investment narrative and future positioning.

Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

CACI International Investment Narrative Recap

To own CACI, you need to believe in its role as a key technology partner to U.S. defense and intelligence agencies, with long term demand anchored in mission critical work. The most important near term catalyst is converting this demand into profitable contract execution, while the biggest risk remains budget and procurement volatility. Young’s appointment looks supportive for execution on complex programs, but does not by itself remove funding, competition, or talent pressures.

Among recent announcements, the April 2026 earnings release and guidance raise are most relevant here. CACI lifted its full year revenue outlook to US$9.5 billion to US$9.6 billion and guided higher net income, which puts even more focus on operational follow through. Young’s background running a roughly US$7.0 billion national security space business may matter if CACI increasingly leans on advanced space and defense tech programs to support those targets.

Yet behind the stronger guidance, investors should not overlook how exposed CACI remains to U.S. budget swings and contract timing...

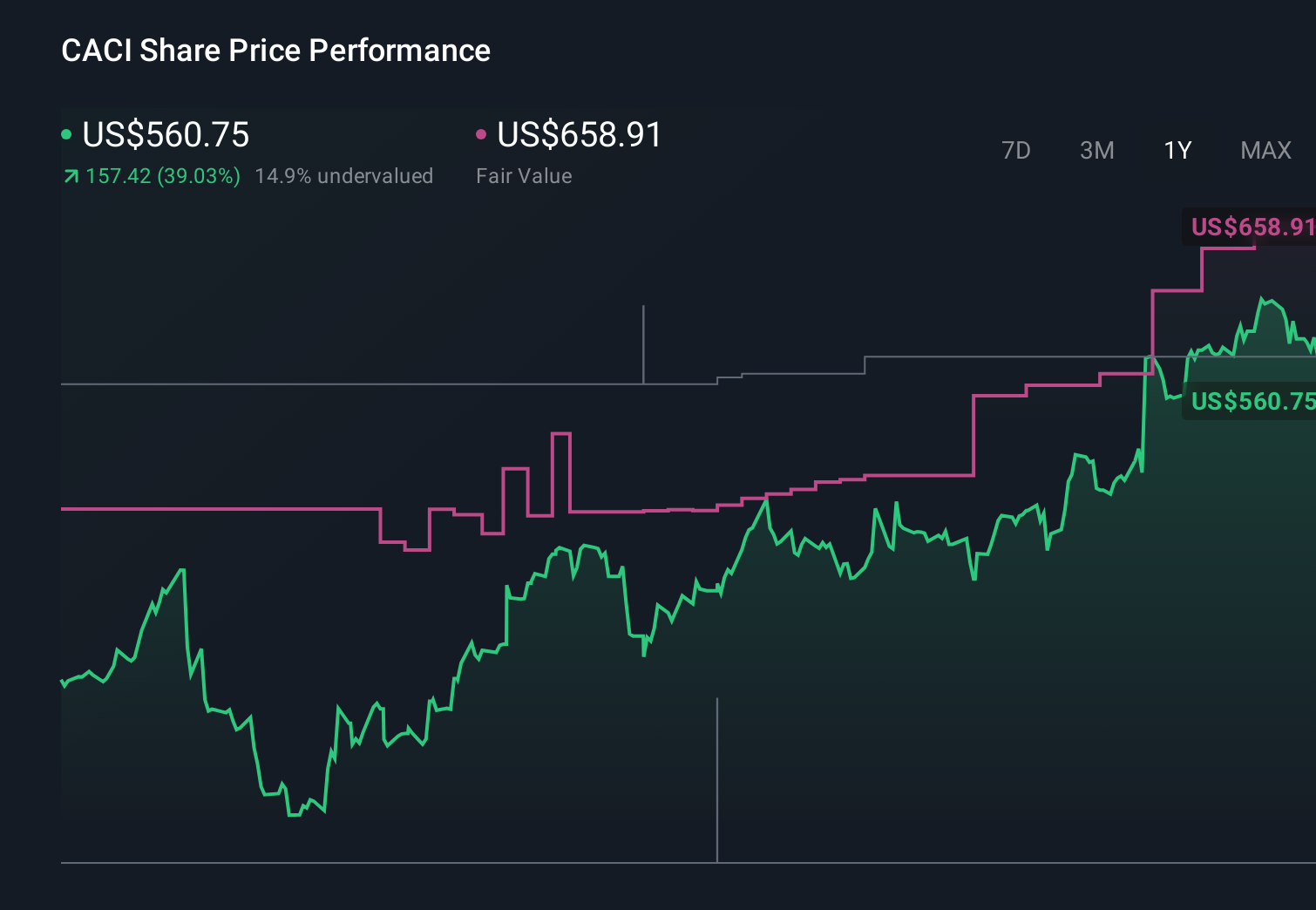

CACI International's narrative projects $11.9 billion revenue and $744.0 million earnings by 2029. This requires 10.0% yearly revenue growth and a $225.6 million earnings increase from $518.4 million today.

Uncover how CACI International's forecasts yield a $709.23 fair value, a 52% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already assuming only about 8.8% annual revenue growth and shrinking margins by 2029, so compared with concerns about automation eroding legacy services, they paint a far more cautious picture that this new leadership move could eventually challenge or reinforce.

Explore 3 other fair value estimates on CACI International - why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your CACI International research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free CACI International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CACI International's overall financial health at a glance.

Ready For A Different Approach?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- This technology could replace computers: discover 30 stocks that are working to make quantum computing a reality.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.