Does CACI’s New Manufacturing EVP Appointment Reshape Its Margin and Execution Story (CACI)?

CACI International Inc Class A CACI | 0.00 |

- CACI International recently appointed Christopher Monoski as Executive Vice President, Manufacturing, putting him in charge of a centralized operation producing secure, mission-critical technologies such as RF systems, photonics, optical communications, space-based EO/IR payloads, mixed-signal electronics, and integrated electro-mechanical solutions for defense and national security customers.

- Monoski’s extensive experience running large-scale manufacturing and supply chains at L3Harris Technologies could reshape how efficiently CACI turns advanced technology development into reliable, repeatable hardware delivery for complex government programs.

- We’ll now examine how Monoski’s centralized manufacturing leadership may influence CACI’s existing investment narrative around margins, execution, and defense technology scale.

Outshine the giants: these 15 early-stage AI stocks could fund your retirement.

CACI International Investment Narrative Recap

To own CACI, you need to believe in its role as a core provider of secure, advanced technologies to U.S. defense and intelligence customers, with execution and contract performance front of mind. The biggest near term catalyst remains converting its technology portfolio into dependable, higher margin hardware programs, while key risks center on federal budget volatility and production execution. Monoski’s appointment directly targets CACI’s manufacturing and supply chain risk, but its impact will take time to show up in results.

The Bank of America Industrials conference on May 12, 2026, is the most relevant recent event, as it gives CFO Jeff MacLauchlan a platform to explain how CACI’s centralized manufacturing push fits with its updated 2026 guidance and capital decisions around debt-funded acquisitions like ARKA. Investors watching margins, backlog conversion, and manufacturing execution will likely listen for any early read-through on how Monoski’s organization could affect those metrics.

Yet even as CACI strengthens manufacturing, investors should be aware that government budget turbulence and procurement delays could still...

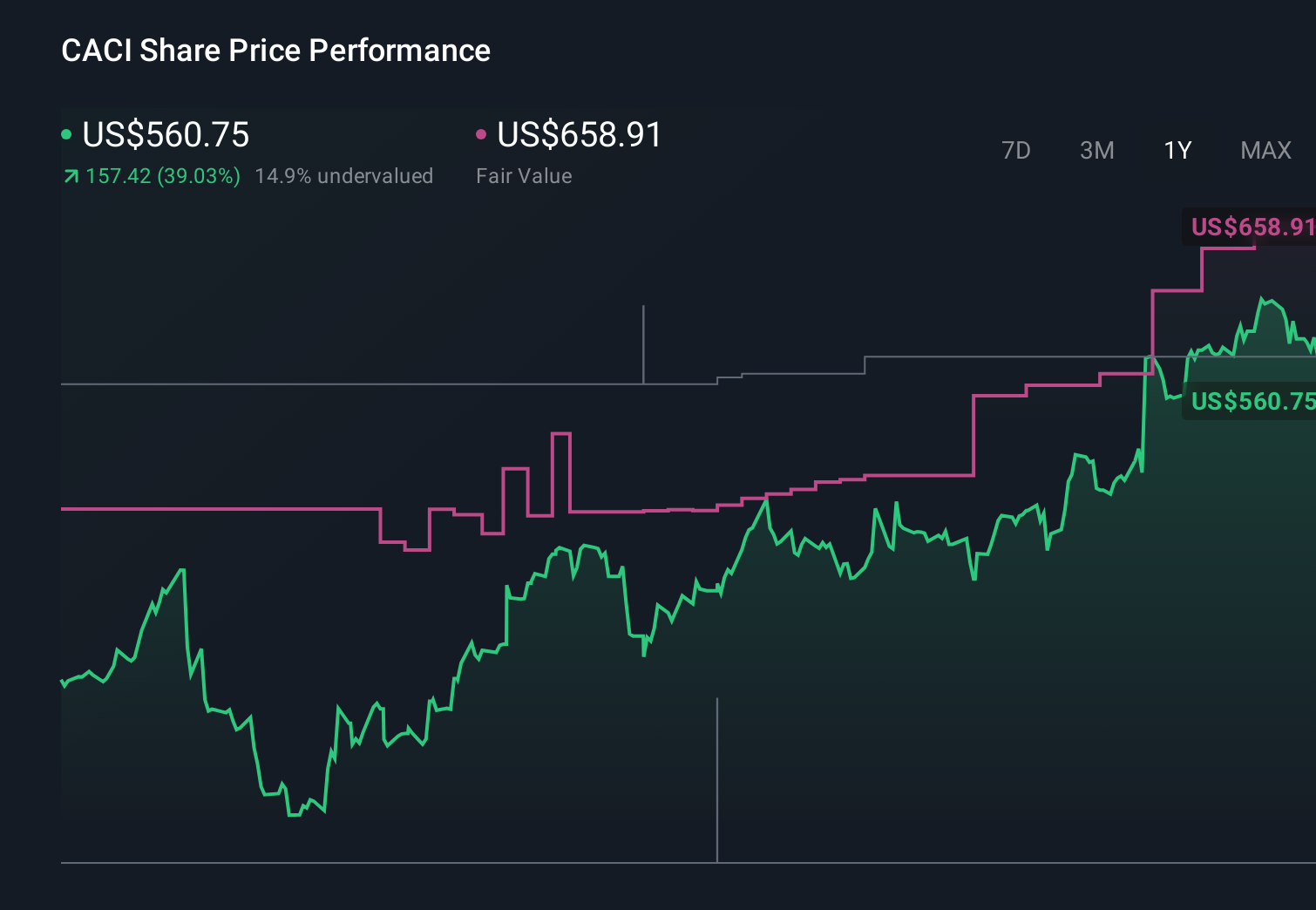

CACI International's narrative projects $11.9 billion revenue and $744.0 million earnings by 2029. This requires 10.0% yearly revenue growth and a roughly $225.6 million earnings increase from $518.4 million today.

Uncover how CACI International's forecasts yield a $709.23 fair value, a 42% upside to its current price.

Exploring Other Perspectives

Compared with the baseline story, the most bearish analysts were already baking in slower revenue growth near 8.8 percent and thinner margins, so you should treat Monoski’s centralized manufacturing push as a potential swing factor that could either reinforce or challenge those more pessimistic expectations.

Explore 3 other fair value estimates on CACI International - why the stock might be worth just $709.23!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your CACI International research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free CACI International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CACI International's overall financial health at a glance.

Ready For A Different Approach?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are the new gold rush. Find out which 33 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.