Does Carvana’s 5-for-1 Stock Split and Delivery Push Reframe the Bull Case for CVNA?

Carvana Co. Class A CVNA | 302.04 | +0.22% |

- Carvana recently announced that its board approved a 5-for-1 stock split, subject to shareholder approval on May 5, 2026, alongside expanding same-day vehicle delivery to more markets including greater Los Angeles.

- The split, aimed at keeping shares attainable for employees while the company scales its e-commerce and logistics network, spotlights how corporate structure decisions intersect with Carvana’s operational expansion and shareholder governance debates.

- We’ll now examine how Carvana’s first-ever 5-for-1 stock split could influence its investment narrative and long-term growth assumptions.

AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Carvana Investment Narrative Recap

To own Carvana today, you need to believe it can keep scaling its used car e-commerce model while protecting margins as volumes grow. The most important short term catalyst remains execution in reconditioning and logistics, where missteps could quickly pressure profitability. The newly announced 5 for 1 stock split does not materially change that operational risk, but it may sharpen attention on governance and capital allocation choices as the business continues to expand.

Among the recent announcements, the expansion of same day delivery in greater Los Angeles feels most relevant. It connects directly to Carvana’s core growth thesis that faster delivery and a fully online experience can attract more buyers and sellers, improving unit economics as volumes move through its ADESA enabled network. If these high density markets scale efficiently, they could support the bullish growth assumptions that underpin many investors’ expectations for Carvana.

Yet behind the optimism, the possibility that rising logistics and compliance costs could quietly compress margins is something investors should be aware of...

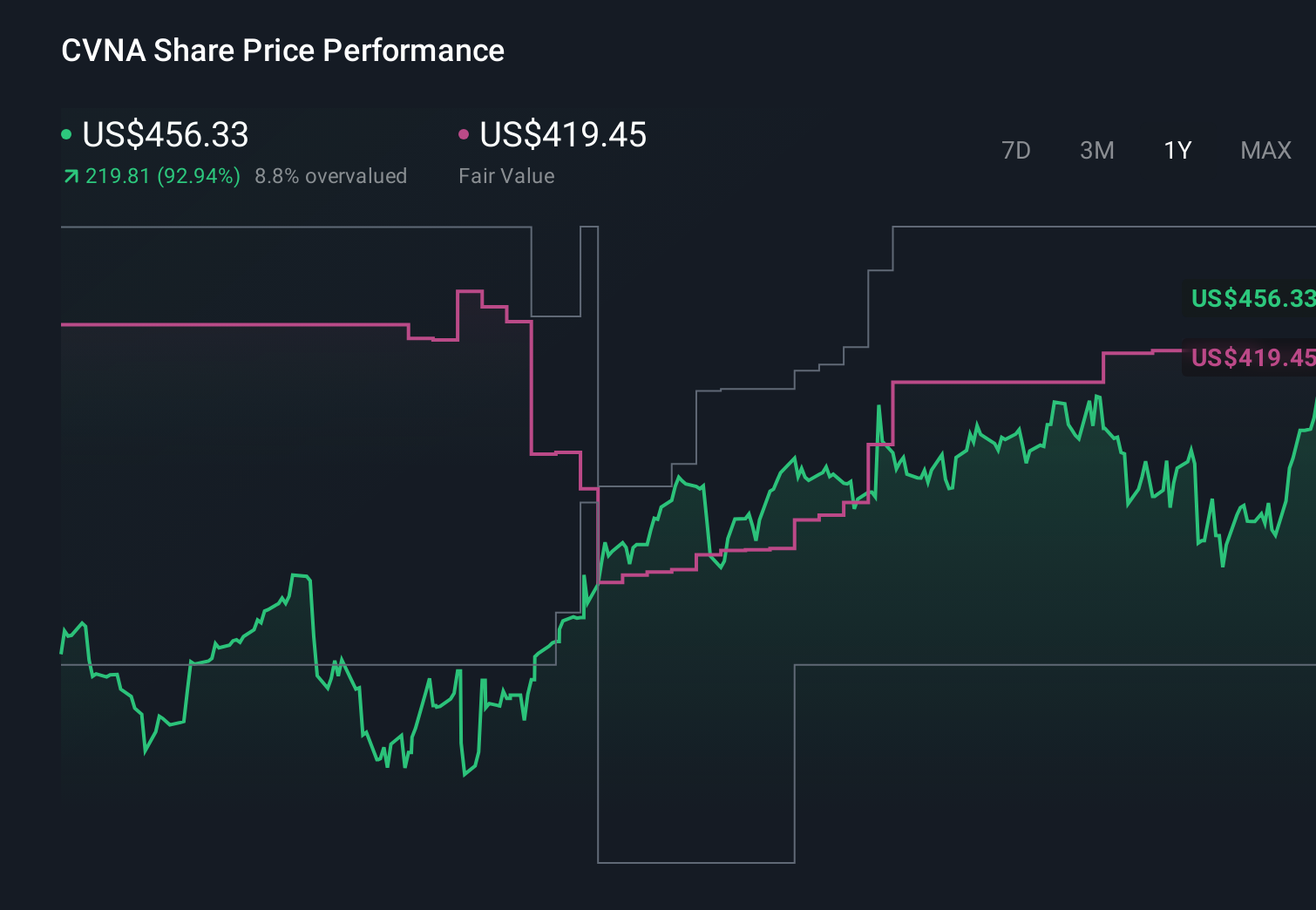

Carvana's narrative projects $33.2 billion revenue and $2.2 billion earnings by 2028.

Uncover how Carvana's forecasts yield a $481.27 fair value, a 64% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts paint a much harsher picture, even before this news, expecting revenue of about US$26.8 billion and earnings near US$1.1 billion by 2028, which they argue might not justify the implied high P E multiple, so if you are excited by the stock split and delivery expansion it is worth comparing that optimism with these more cautious forecasts and considering how new developments could shift either side of the debate.

Explore 14 other fair value estimates on Carvana - why the stock might be worth less than half the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Carvana research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Carvana research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Carvana's overall financial health at a glance.

Curious About Other Options?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 22 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Uncover the next big thing with 32 elite penny stocks that balance risk and reward.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.