Does Carvana’s (CVNA) Sarasota Hub Reveal a Deeper Shift in Its Operating Playbook?

Carvana CVNA | 0.00 |

- Earlier this week, Carvana announced it is adding Inspection and Reconditioning Center capabilities to its long‑running ADESA Sarasota wholesale auction site in Bradenton, Florida, creating extra reconditioning capacity, a new local retail inventory pool and around 100 new jobs over time.

- By layering its CARLI software platform onto the 60‑acre Sarasota facility, Carvana is effectively turning a traditional auction site into a dual‑purpose hub that can support faster local delivery, richer retail selection and enhanced services for wholesale buyers on the Florida Gulf Coast.

- We’ll now examine how converting ADESA Sarasota into a dual wholesale‑retail reconditioning hub could influence Carvana’s broader investment narrative.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Carvana Investment Narrative Recap

To own Carvana, you need to believe its mix of online retailing and physical infrastructure can keep scaling while protecting margins. The Sarasota IRC expansion fits neatly into that thesis by adding reconditioning capacity and local inventory, but it does not fundamentally change the key near term catalyst, which is how efficiently Carvana can ramp its growing ADESA footprint without letting unit costs creep up. It also does not remove the execution risk around underutilized facilities and higher operating costs.

The Sarasota move sits alongside a broader wave of IRC integrations, such as the April 2026 addition of reconditioning capabilities at ADESA Syracuse in New York. Taken together, these projects are central to the bullish catalyst that Carvana’s national network of IRC enabled ADESA sites can lower transport and processing costs and support faster delivery. They also magnify the risk that any delays or inefficiencies in filling this new capacity could pressure margins just as expectations have risen.

Yet even as Carvana leans into this build out, investors should be aware that underutilized reconditioning centers could...

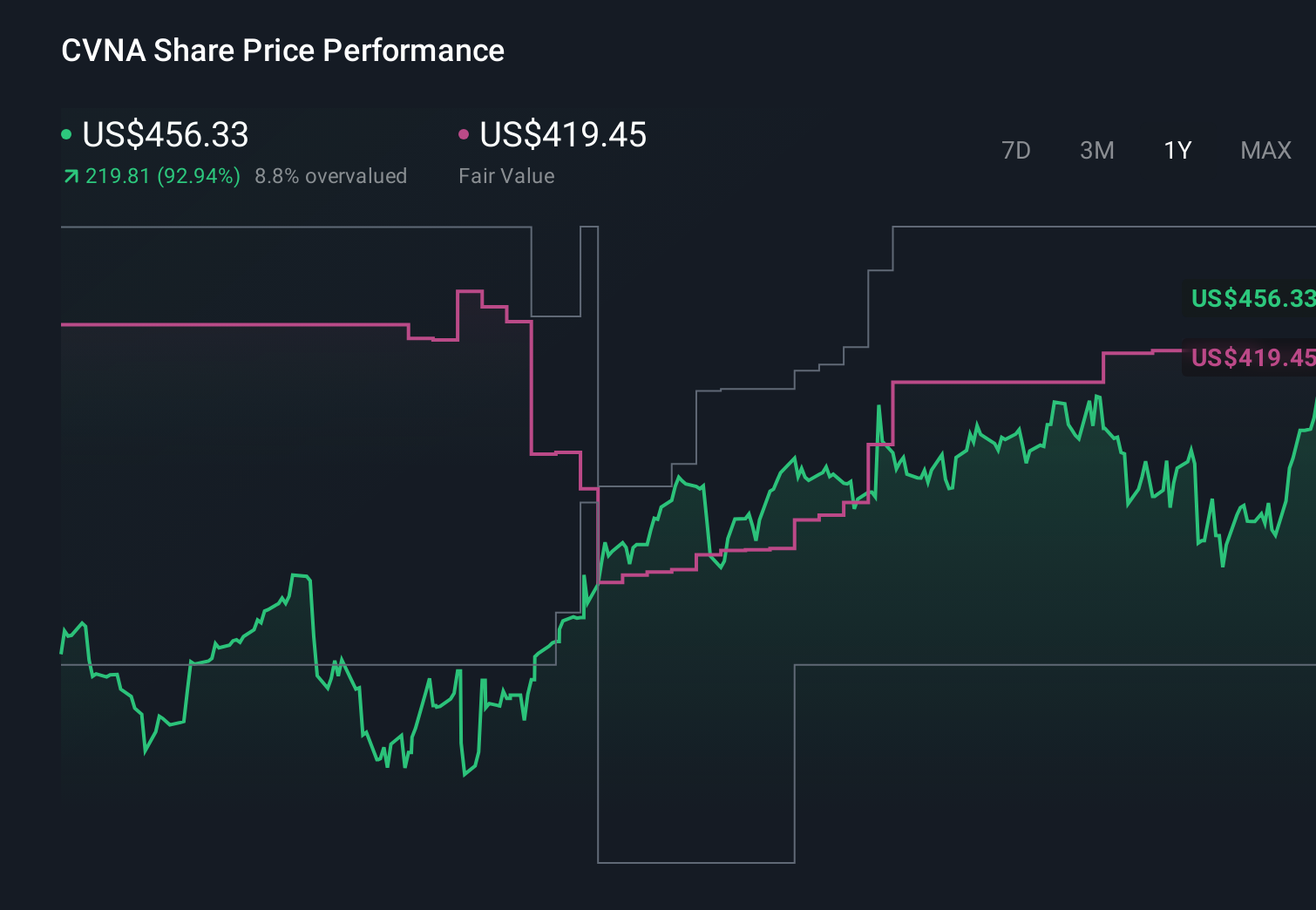

Carvana's narrative projects $44.2 billion revenue and $3.0 billion earnings by 2029. This requires 25.2% yearly revenue growth and a roughly $1.6 billion earnings increase from $1.4 billion today.

Uncover how Carvana's forecasts yield a $92.10 fair value, a 39% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming Carvana could reach about US$50.0 billion in revenue and US$3.7 billion in earnings by 2029, which is a far more aggressive path than the consensus view, and the Sarasota IRC news may either reinforce that upside story or highlight how much must still go right for those projections to hold.

Explore 9 other fair value estimates on Carvana - why the stock might be worth over 4x more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Carvana research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Carvana research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Carvana's overall financial health at a glance.

Seeking Other Investments?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Find 43 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.