Does Centene’s (CNC) Shift Into Russell Growth Indexes Redefine Its Core Investment Narrative?

Centene Corporation CNC | 0.00 |

- On 27 June 2026, Centene Corporation (NYSE:CNC) was reclassified into several Russell growth benchmarks, including the Russell 1000 Growth, Russell 3000 Growth, Russell 3000E Growth, and Russell Midcap Growth, while being removed from the Russell 1000 Defensive and Russell 1000 Value-Defensive indexes.

- Alongside this index reshuffle, Centene added experienced financial, audit, and human capital executive Lauren M. Tyler to its Board, signaling an emphasis on governance and growth-oriented positioning.

- We’ll now examine how Centene’s broad inclusion in Russell growth indexes could influence the company’s existing investment narrative and outlook.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 15 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Centene Investment Narrative Recap

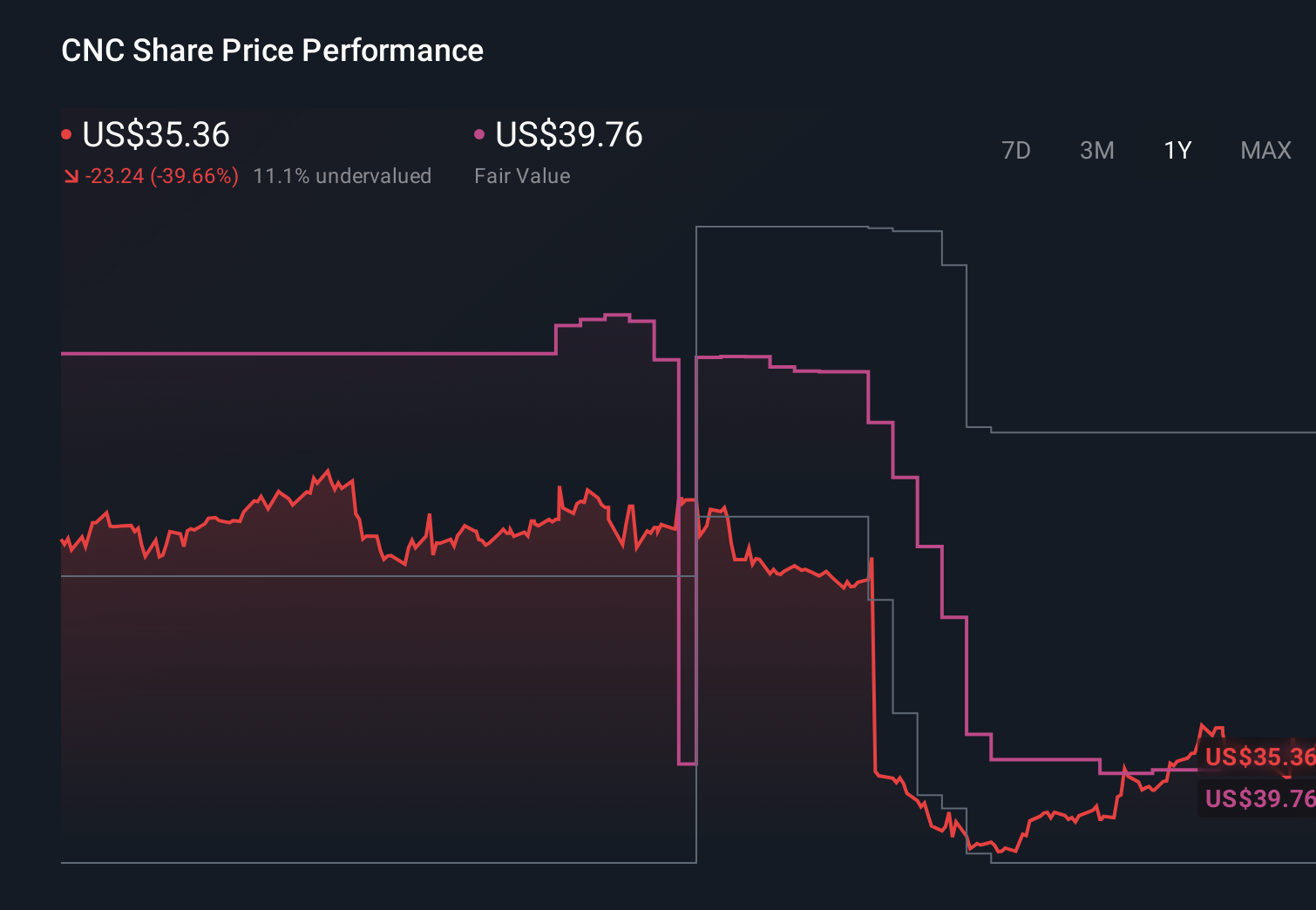

To own Centene today, you need to believe its core government-backed health plans can translate contract wins and margin recovery efforts into sustainable earnings, while policy and medical cost volatility remain manageable. The recent shift into Russell growth indexes may support liquidity and awareness, but it does not materially change near term fundamentals. The most important near term catalyst still centers on Medicaid and Medicare margin improvement, while reimbursement and medical cost pressures remain the key risk.

The appointment of Lauren M. Tyler to the Board looks most relevant here, given Centene’s increased visibility in growth indexes and its ongoing earnings recovery efforts. Her audit and financial background, combined with human capital expertise, may matter for how Centene steers cost discipline, risk oversight, and talent in Medicaid, Medicare Advantage, and Marketplace operations, which all sit at the heart of the company’s margin recovery catalysts.

Yet against this constructive setup, investors still need to watch how exposed Centene is to changing healthcare policy and reimbursement terms...

Centene's narrative projects $200.3 billion revenue and $2.7 billion earnings by 2029. This requires 4.0% yearly revenue growth and a $9.1 billion earnings increase from -$6.4 billion today.

Uncover how Centene's forecasts yield a $61.83 fair value, a 10% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming Centene could reach about US$209.5 billion in revenue and US$3.7 billion in earnings by 2029, so you should expect that this growth index inclusion and the risks around government reimbursement could reshape those expectations in different ways.

Explore 14 other fair value estimates on Centene - why the stock might be worth over 3x more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Centene research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Centene research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Centene's overall financial health at a glance.

Contemplating Other Strategies?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The latest GPUs need a type of rare earth metal called Terbium and there are only 31 companies in the world exploring or producing it. Find the list for free.

- Uncover the next big thing with 21 elite penny stocks that balance risk and reward.

- Find 41 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.