Does Cheaper Credit Really Improve Credit Acceptance’s (CACC) Risk‑Return Balance in Non‑Prime Auto?

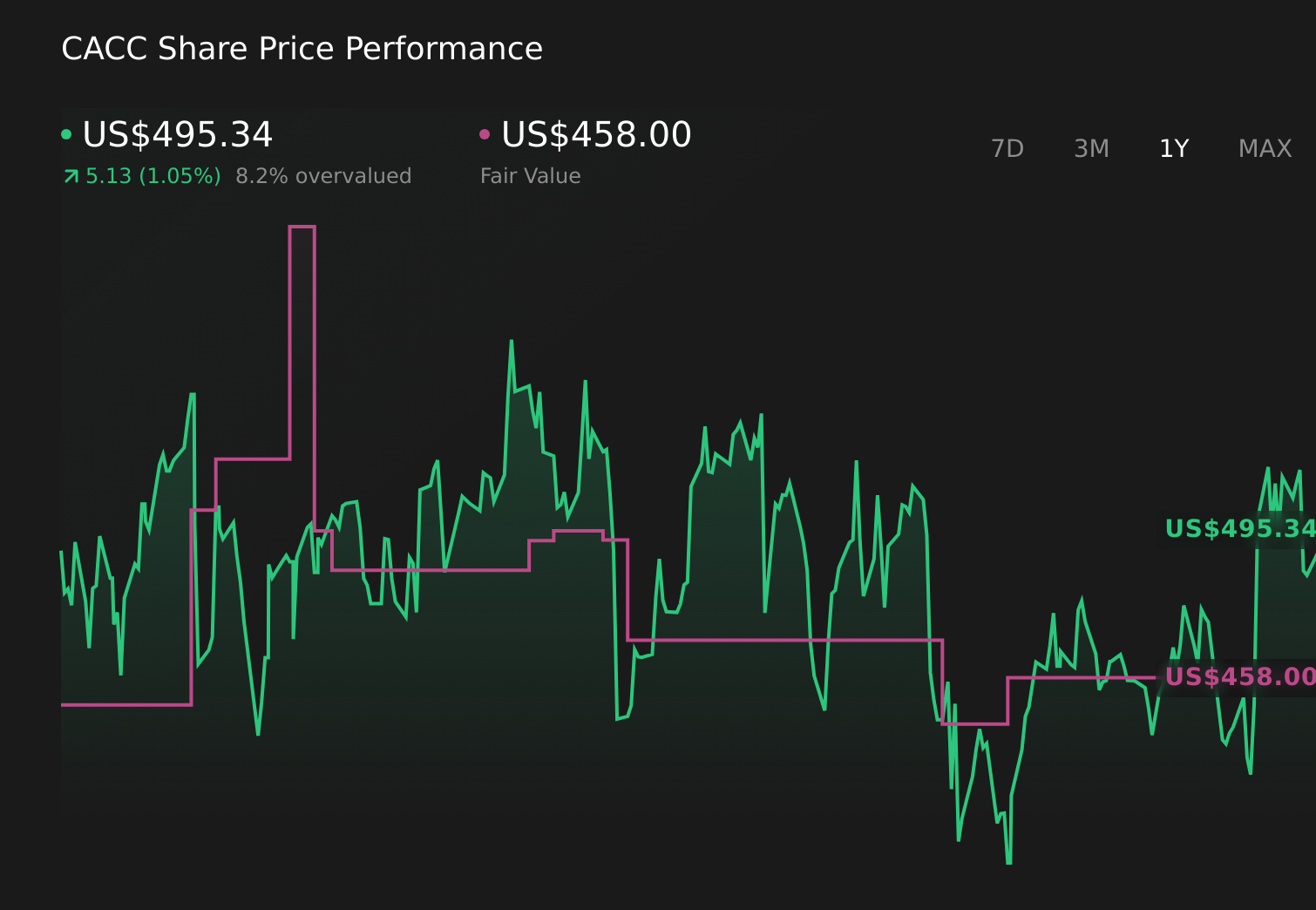

Credit Acceptance Corporation CACC | 0.00 |

- In June 2026, Credit Acceptance Corporation entered into the Fifteenth Amendment to its Sixth Amended and Restated Credit Agreement, extending the revolving secured line of credit facility’s revolving period from June 22, 2028 to June 22, 2029 and reducing the interest margin on SOFR-based borrowings from 197.5 to 175.0 basis points, with US$270.5 million outstanding as of June 9, 2026.

- This extension and lower borrowing spread modestly improve funding flexibility and interest costs, which matter given the company’s reliance on credit facilities to support its non-prime auto loan portfolio.

- We’ll now examine how the extended, cheaper credit facility may influence Credit Acceptance’s investment narrative and its evolving risk-return profile.

The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Credit Acceptance Investment Narrative Recap

To own Credit Acceptance, you need to be comfortable with a leveraged, non prime auto lender where everything hinges on loan performance and funding access. The extended, slightly cheaper revolving facility helps liquidity but does not change the near term focus on credit outcomes and competitive pressure in subprime auto, which remain the key catalyst and the biggest risk.

The recent US$450.0 million asset backed financing completed in May 2026 sits alongside this amended bank facility, reinforcing how central funding costs and availability are to the story. Together, these moves frame how investors may weigh any improvement in liquidity against concerns about loan vintage performance and origination volumes.

Yet even with cheaper funding in place, investors should be aware of how quickly weaker 2022 to 2024 loan vintages could...

Credit Acceptance's narrative projects $3.6 billion revenue and $671.0 million earnings by 2029. This requires 40.8% yearly revenue growth and about a $217.6 million earnings increase from $453.4 million today.

Uncover how Credit Acceptance's forecasts yield a $536.67 fair value, a 14% downside to its current price.

Exploring Other Perspectives

Two members of the Simply Wall St Community currently bracket Credit Acceptance’s fair value between US$350 and US$537, underscoring how far apart individual views can be. As you weigh those opinions against the company’s greater funding flexibility from the extended credit facility, it is worth considering how funding terms might interact with any future shifts in loan performance and competitive intensity.

Explore 2 other fair value estimates on Credit Acceptance - why the stock might be worth 44% less than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Credit Acceptance research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Credit Acceptance research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Credit Acceptance's overall financial health at a glance.

Looking For Alternative Opportunities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Capitalize on the AI infrastructure supercycle with our selection of the 50 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.