Does Chip Wilson’s Activist Push to Recast lululemon’s Brand and Board Change The Bull Case For LULU?

lululemon athletica inc. LULU | 0.00 |

- In early May 2026, lululemon athletica founder Dennis “Chip” Wilson intensified his activist campaign with letters, proxy filings, and social media urging shareholders to elect his three independent board nominees and criticizing the company’s creative direction, brand positioning, and governance.

- This confrontation, centered on whether lululemon has shifted from a premium innovator to a more generic athletic retailer, puts the brand’s identity and future leadership under shareholder scrutiny.

- We’ll now examine how Wilson’s push to reshape lululemon’s board and creative direction could influence the company’s existing investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

lululemon athletica Investment Narrative Recap

To own lululemon today, you need to believe the brand can refresh its product engine, reignite U.S. demand, and keep expanding internationally while managing margin pressure from tariffs and promotions. Chip Wilson’s activist push challenges the company’s creative direction and governance, but on its own does not yet change the near term catalyst, which is whether the Spring 2026 product reset actually lifts traffic and full price sell through. The biggest current risk remains brand fatigue in North America.

The news around Wilson’s proxy campaign lands just weeks after lululemon named former Nike executive Heidi O’Neill as incoming CEO for September 2026, and added former Unilever marketing leader Esi Eggleston Bracey to the board. That combination of a planned leadership transition and an activist fight over creative control directly intersects with the core catalyst of product innovation and brand positioning, and could influence how quickly the company executes its planned assortment reset.

Yet beneath the brand debate, investors should also be aware that...

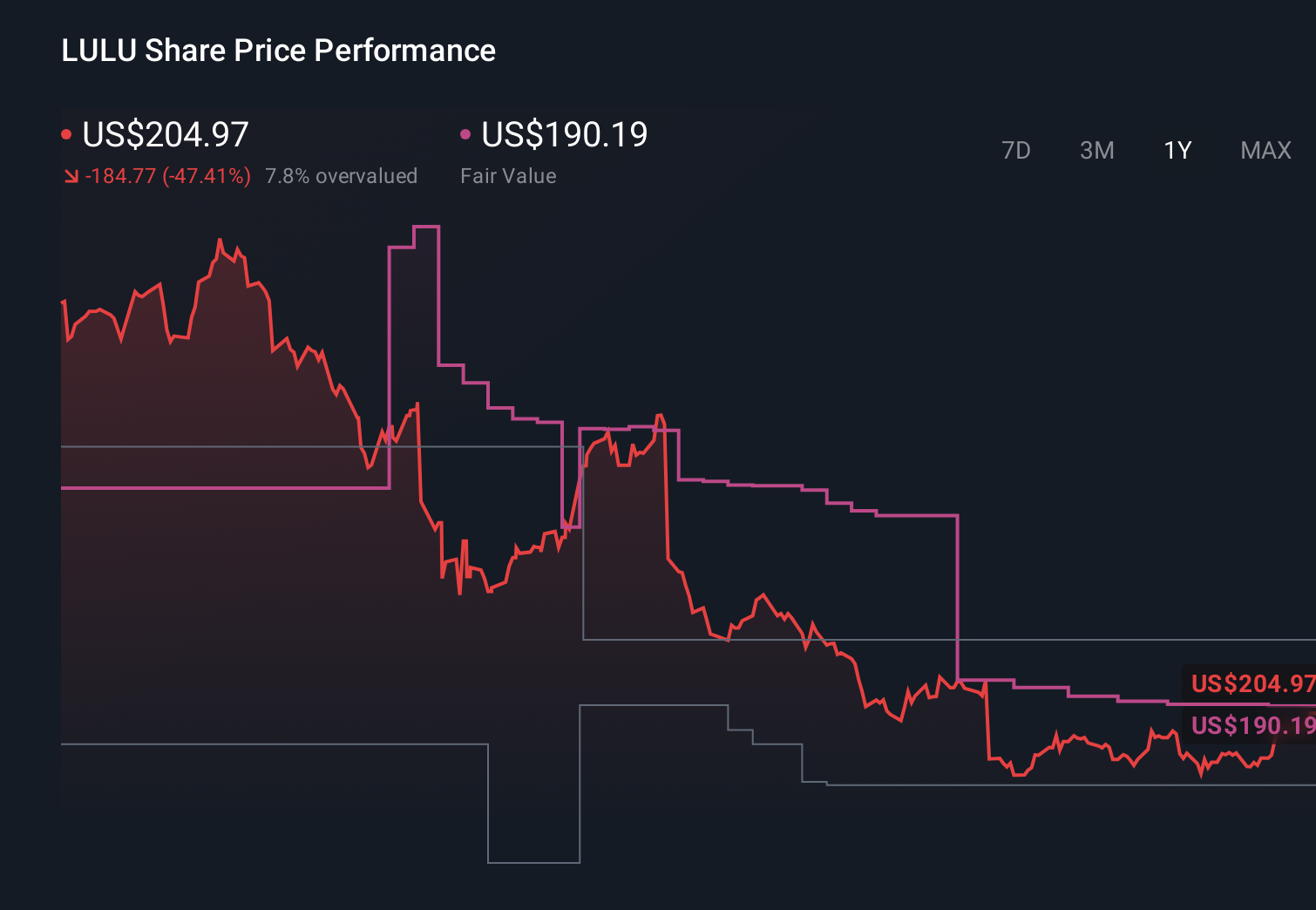

lululemon athletica's narrative projects $12.6 billion revenue and $1.6 billion earnings by 2029. This requires 4.3% yearly revenue growth with earnings remaining flat from $1.6 billion today.

Uncover how lululemon athletica's forecasts yield a $181.08 fair value, a 36% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming revenue would grow only about 2.7 percent a year and earnings slip to roughly US$1.5 billion, so Wilson’s challenge and the CEO transition could either reinforce that bearish view or prompt a rethink if the board and product changes play out differently than they expected.

Explore 40 other fair value estimates on lululemon athletica - why the stock might be worth just $141.61!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your lululemon athletica research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free lululemon athletica research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate lululemon athletica's overall financial health at a glance.

Want Some Alternatives?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Find 51 companies with promising cash flow potential yet trading below their fair value.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 33 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.