Does Chubb (CB) Have More Upside After Its $7.5b Buyback?

Chubb Limited CB | 0.00 |

Chubb stock has delivered a 146.2% total return over the past 5 years, and the Excess Returns intrinsic value estimate currently points to meaningful upside relative to the market price. However, the company still carries a low overall value score, which suggests the broader checks do not see it as a straightforward bargain.

- Over 5 years Chubb has returned 146.2%, which puts current buyers in the position of judging whether that strong run has already reflected most of the good news in the price.

- The launch of a $400m marine war risk insurance facility and continued capital return through dividends and buybacks can support the earnings and cash flow story, while exposure to geopolitical risk and capital market conditions may weigh on how investors price that growth.

- Chubb scores 2 out of 6 on our valuation checks, which points to a stock that leans expensive on several measures rather than screening as clearly cheap.

For investors, the debate is whether Chubb's current share price already reflects the intrinsic value implied by the Excess Returns model or if there is still a margin of safety.

Does Chubb Look Undervalued on Excess Returns?

The Excess Returns model evaluates how efficiently Chubb turns its equity base into profits above its own cost of capital. On this view, Chubb’s book value is $189.93 per share and is projected to rise to a stable $227.37 per share, while stable EPS is estimated at $30.46 per share based on analyst expectations.

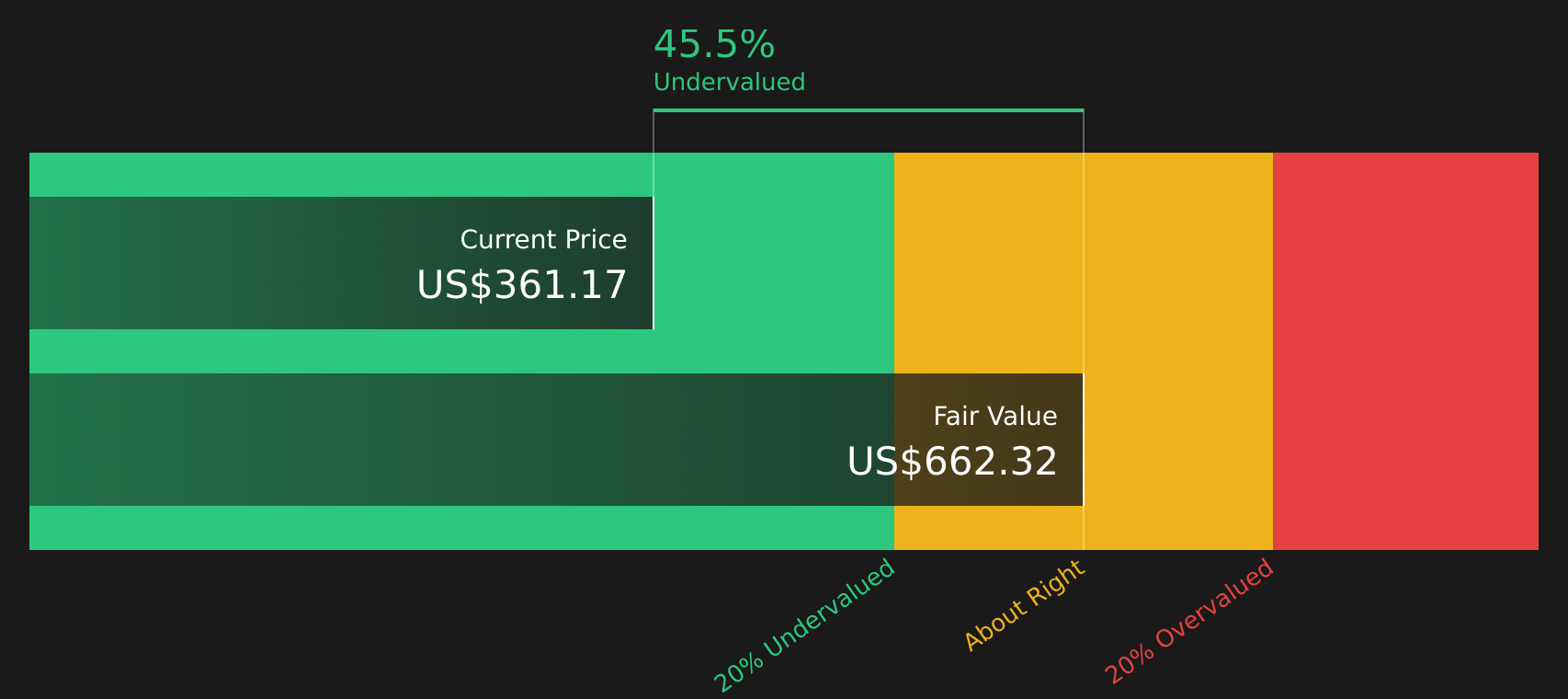

With a cost of equity of $15.74 per share and an excess return of $14.72 per share, the model assumes Chubb can earn more on its equity than it costs to fund, supported by an average return on equity of 13.40%. That stream of excess returns translates into an intrinsic value estimate of $662.32 per share, which puts the current market price 45.5% below this estimate. Because the new $7.5b share buyback program reduces the equity base over time, it fits neatly with a thesis that hinges on sustained returns on equity and supports this excess returns framework.

On this Excess Returns view, Chubb stock screens as undervalued, with the market price sitting well below the model’s $662.32 per share estimate.

Our Excess Returns analysis suggests Chubb is undervalued by 45.5%. Track this in your watchlist or portfolio, or discover 43 more high quality undervalued stocks.

Does Chubb Look Fairly Valued on Earnings?

P/E is a useful yardstick for Chubb because earnings remain a central focus for insurance investors. Chubb currently trades on a P/E of 12.4x, which is close to the Insurance industry average of 12.1x and sits above the peer group average of about 9.0x.

The Fair P/E Ratio, which looks at Chubb’s earnings profile, size, and risk to infer a more tailored multiple, is 11.4x. That is only slightly below where the stock trades today, so while Chubb carries a premium to many peers, it is not extreme and lines up with what this framework suggests is reasonable for the company.

Overall, Chubb appears priced roughly in line with what its earnings profile would justify on a P/E basis.

The Chubb Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where the valuation puzzle for Chubb leaves off by spelling out which combinations of future growth, margins and earnings would need to play out for the stock to be worth significantly more or less than today’s price. Each Narrative links a specific fair value to a clear story about Chubb’s potential catalysts and risks, so you can track over time which version of events appears to be unfolding on the Community page.

Be one of the early voices in the Simply Wall St community to present a number-driven narrative on Chubb, including a clear view on whether the new $400m marine war risk facility and Chubb's capital return plans truly support the current pricing.

Set out your assumptions, publish your narrative, and track how it holds up as Chubb's results, capital moves and war risk exposure develop over time.

Do you think there's more to the story for Chubb? Head over to our Community to see what others are saying!

The Bottom Line

For Chubb, the Excess Returns intrinsic value estimate points to the stock screening as undervalued, while the P/E view suggests pricing is about right relative to its earnings profile. That gap comes down to what you think matters more from here: the value of its equity and cash generation, or how the market currently prices insurers on earnings and sentiment. With broader valuation checks still weak, the key question is whether Chubb can keep earning enough above its cost of equity for that intrinsic value case to hold, or whether the current market multiple is already capturing the realistic upside given its risks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.