Does Deeper Merck and eGain Adoption Confirm Salesforce’s AI Operating Layer Ambitions for CRM?

Salesforce.com, inc. CRM | 0.00 |

- In early May 2026, Merck Animal Health and eGain announced deeper use of Salesforce platforms, with Merck adopting Agentforce Life Sciences for unified, data-rich customer engagement and eGain embedding its AI Agent directly into Salesforce Service Cloud to streamline case handling across channels.

- These moves highlight how enterprises are increasingly treating Salesforce as a central, AI-ready operating layer that unifies data, workflows, and agent-based automation across complex ecosystems.

- We’ll now examine how this growing use of Salesforce as an AI-enabled operating layer for customer engagement influences the company’s investment narrative.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 33 best rare earth metal stocks of the very few that mine this essential strategic resource.

Salesforce Investment Narrative Recap

The core Salesforce thesis is that it can be the AI-enabled operating layer for customer and employee engagement, with Agentforce and Data 360 deepening customer lock-in. The key near term catalyst is evidence that AI and Data Cloud adoption can offset macro and software-spending worries, against the major risk of intensifying competition and potential commoditization of CRM and workflow tools. The Merck and eGain news is positive validation but not a transformative catalyst on its own.

Among recent developments, the launch of Agentforce Operations in late April 2026 looks especially relevant. As more enterprises embed AI agents into Salesforce, Operations’ audit trails and compliance controls directly address one of the biggest adoption hurdles. If customers view Salesforce not just as an AI front end, but as a governed execution layer for agentic work, that could reinforce the company’s efforts to sustain pricing power and protect margins despite rising competition.

Yet beneath this AI momentum, investors should also be aware that growing regulatory and competitive pressures could eventually force Salesforce to reconsider how aggressively it leans into...

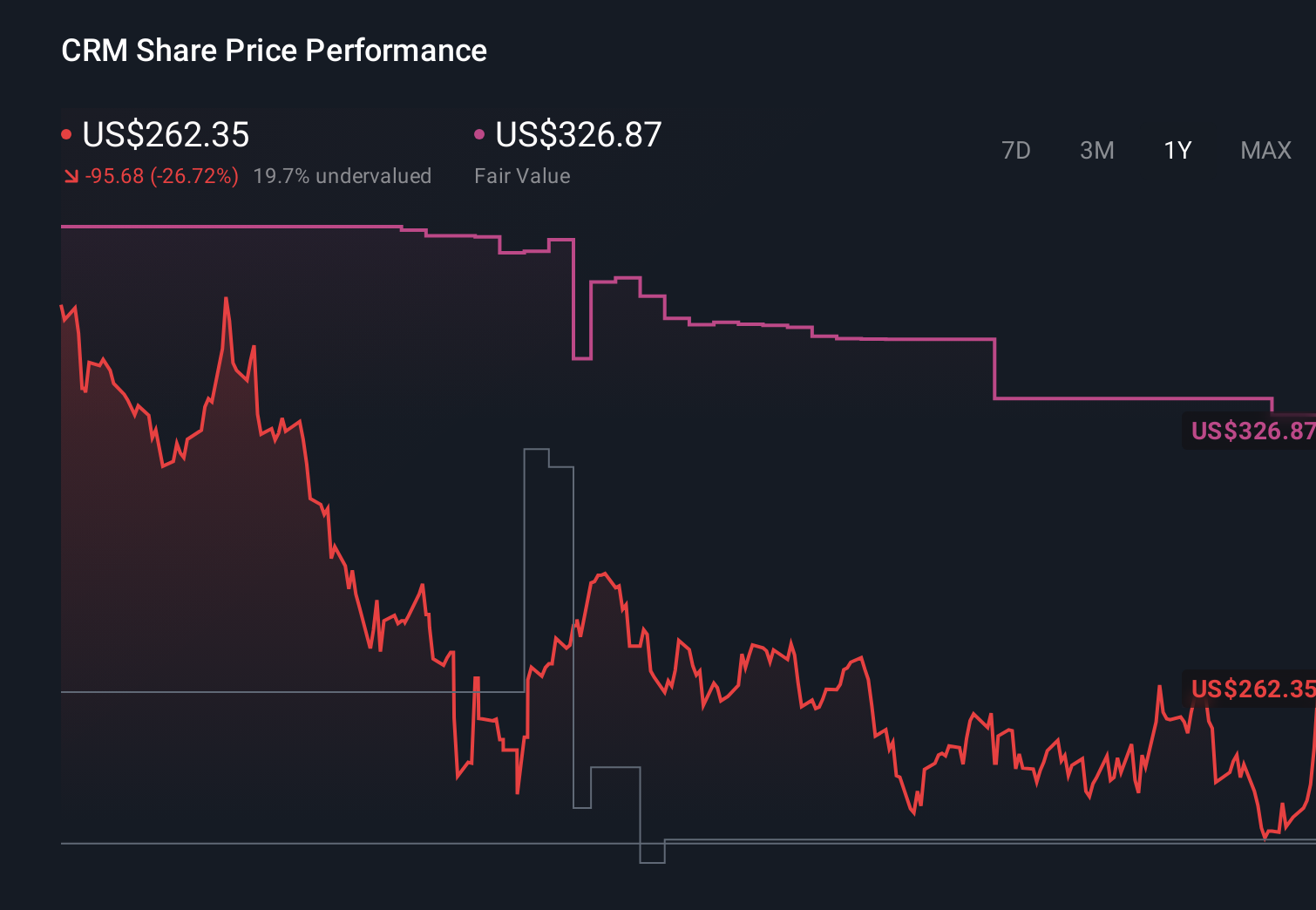

Salesforce's narrative projects $51.9 billion revenue and $10.3 billion earnings by 2028. This requires 9.6% yearly revenue growth and about a $3.6 billion earnings increase from $6.7 billion today.

Uncover how Salesforce's forecasts yield a $317.21 fair value, a 79% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts already projected Salesforce revenue of about US$58.9 billion and earnings of US$11.6 billion by 2029, and they see today’s AI agent momentum as reinforcing that bullish view, while the latest Agentforce deployments also highlight how quickly the risk of disruptive AI automation could reshape both Salesforce’s opportunities and its vulnerabilities.

Explore 38 other fair value estimates on Salesforce - why the stock might be worth just $200.00!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Salesforce research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Salesforce research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Salesforce's overall financial health at a glance.

Ready For A Different Approach?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- Find 47 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 26 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.