Does Delta’s Dividend And Governance Stance Amid Fuel Pressure Reframe The Bull Case For DAL?

Delta Air Lines, Inc. DAL | 0.00 |

- In April 2026, Delta Air Lines filed its definitive proxy statement urging shareholders to reject proposals on written consent and cumulative voting, while also declaring a US$0.19 quarterly dividend payable on June 4, 2026.

- At the same time, Delta and other airlines have been cutting less-popular routes and raising fees in response to surging jet fuel costs tied to Middle East conflict and supply disruptions, highlighting how governance decisions are unfolding against a backdrop of significant industry cost pressure.

- With Delta adjusting routes and pricing amid elevated jet fuel costs, we’ll now examine how this developments affect its investment narrative.

Outshine the giants: these 18 early-stage AI stocks could fund your retirement.

Delta Air Lines Investment Narrative Recap

To own Delta today, you need to believe it can protect margins and cash flow despite fuel shocks, route cuts and a still-uncertain demand picture. The most important near term catalyst remains how effectively it reprices fares and reshapes its network around higher fuel costs, while the biggest immediate risk is that those cost pressures persist longer than expected. The latest proxy fight over governance rights looks important but does not materially change that near term risk reward balance.

The dividend declaration of US$0.1875 per share, payable on June 4, 2026, is the clearest recent signal for shareholders. It reinforces that, even as Delta trims less-popular routes and raises fees to cope with the jet fuel shock, management is still committing cash to regular shareholder payouts. For investors focused on catalysts, that ongoing capital return sits alongside fuel cost trends and pricing power as key short term signposts to watch.

Yet, even with this support, investors should be aware that concentrated cost risks from jet fuel and capacity adjustments could...

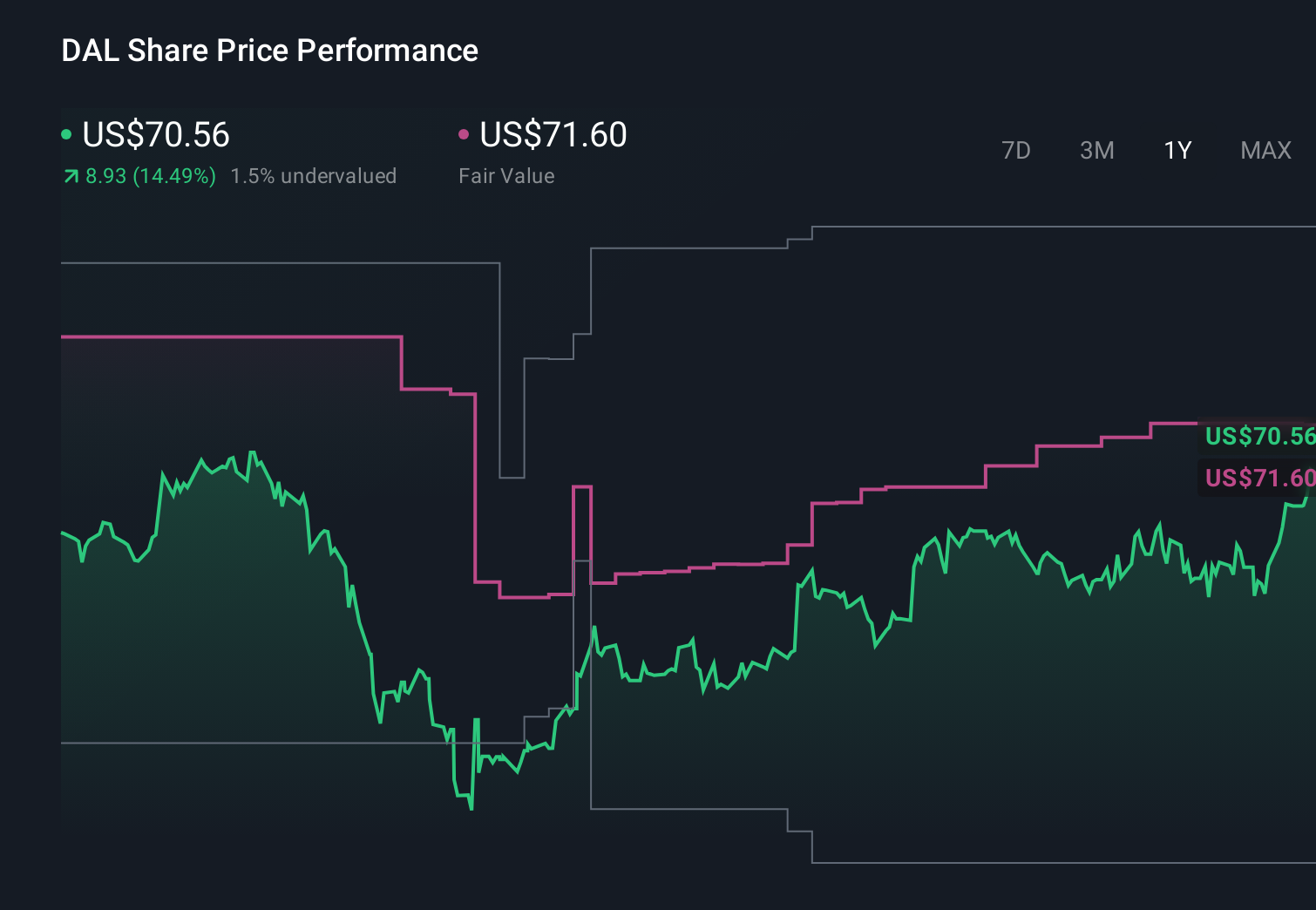

Delta Air Lines' narrative projects $72.9 billion revenue and $5.5 billion earnings by 2029. This requires 4.8% yearly revenue growth and about a $0.5 billion earnings increase from $5.0 billion today.

Uncover how Delta Air Lines' forecasts yield a $79.89 fair value, a 17% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts expected Delta’s earnings to reach about US$6.2 billion by 2028, yet the current jet fuel shock and route cuts could test those upbeat views and your own assumptions.

Explore 10 other fair value estimates on Delta Air Lines - why the stock might be worth as much as 74% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Delta Air Lines research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Delta Air Lines research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Delta Air Lines' overall financial health at a glance.

Looking For Alternative Opportunities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Rare earth metals are the new gold rush. Find out which 32 stocks are leading the charge.

- The future of work is here. Discover the 35 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.