Does GE's (GE) Revenue Jump and Buybacks Offset Softer Guidance in Its Aerospace Story?

GE Aerospace GE | 0.00 |

- In the first quarter of 2026, GE Aerospace reported revenue of US$12,392 million versus US$9,935 million a year earlier, with net income easing to US$1,904 million while basic EPS from continuing operations edged up to US$1.85.

- Alongside this, GE Aerospace continued sizeable share repurchases under its 2024 authorization and faced a US$36 million ITAR-related civil penalty, highlighting both active capital returns and ongoing compliance remediation.

- We’ll now examine how strong revenue growth paired with cautious full-year guidance and trimmed flight-departure forecasts affects GE Aerospace’s investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 19 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

General Electric Investment Narrative Recap

To own GE Aerospace here, you need to believe its large engine installed base and long-cycle services can support earnings even if air traffic growth slows. The latest Q1 results back that thesis on revenue, but management’s unchanged full-year outlook and lower flight-departure forecast keep the biggest near-term risk front and center: a more prolonged air travel slowdown that could soften high-margin aftermarket demand. The ITAR settlement and civil penalty do not appear to change that core risk in a material way.

Among recent announcements, the ongoing buyback under the March 2024 authorization stands out: GE Aerospace has repurchased 65.6 million shares for about US$14.5 billion so far. For investors focused on catalysts, that capital return sits alongside strong order growth as a key support for earnings per share, even as guidance stays conservative and the stock reacts to concerns about margins and flight activity.

Yet behind the strong backlog and capital returns, investors should still pay attention to how rising compliance and regulatory scrutiny could affect...

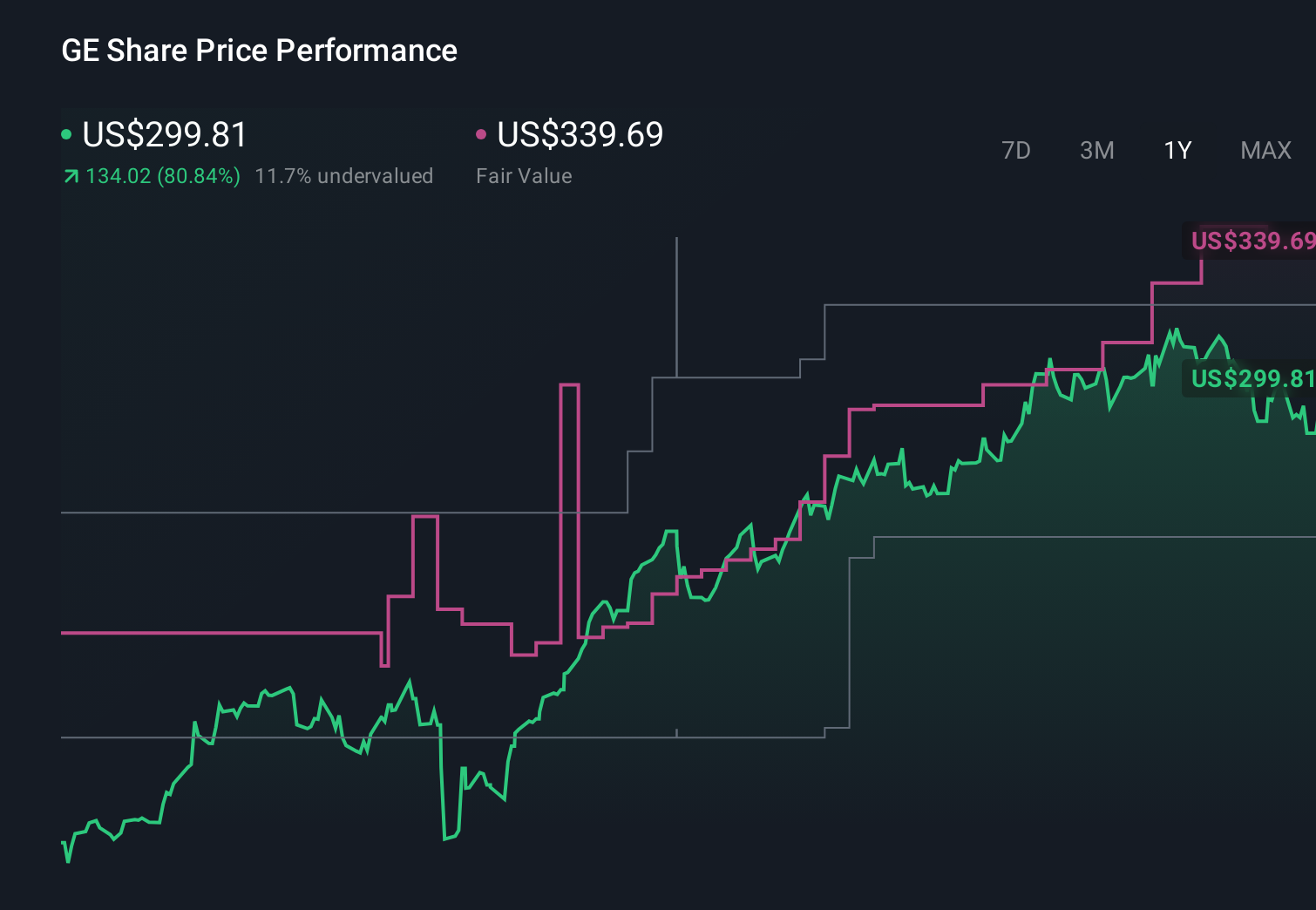

General Electric's narrative projects $50.8 billion revenue and $9.5 billion earnings by 2028. This requires 6.9% yearly revenue growth and about a $1.9 billion earnings increase from $7.6 billion today.

Uncover how General Electric's forecasts yield a $357.24 fair value, a 26% upside to its current price.

Exploring Other Perspectives

While the baseline view stresses air travel and margin risks, the most optimistic analysts were penciling in about US$62 billion of 2029 revenue and US$12.1 billion of earnings, reminding you that expectations can diverge sharply and that both this upbeat scenario and today’s cautious guidance may be revised as the Q1 news is fully digested.

Explore 9 other fair value estimates on General Electric - why the stock might be worth 10% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your General Electric research is our analysis highlighting 5 key rewards and 2 important warning signs that could impact your investment decision.

- Our free General Electric research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate General Electric's overall financial health at a glance.

Looking For Alternative Opportunities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 31 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.