Does GE’s New GE426 Air Force Contract (GE) Deepen Its Defense Engine Investment Narrative?

GE Aerospace GE | 0.00 |

- In May 2026, GE Aerospace announced it had been awarded a U.S. Air Force contract to complete the preliminary design review of its new GE426 engine for the service’s medium-thrust-class Autonomous Collaborative Platform program, advancing a prototype focused on producibility, capability, cost, and alignment with ACP fleet requirements.

- This contract underscores GE Aerospace’s push into scalable, affordable propulsion for autonomous combat platforms, adding another defense-focused program alongside its GEK800 and GEK1500 engines and expanding its role in uncrewed, collaborative military aviation.

- We’ll now examine how this new GE426 Air Force contract could influence GE Aerospace’s investment narrative built around advanced engine programs and defense growth.

Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

General Electric Investment Narrative Recap

To own GE Aerospace, you need to believe in its core engine franchises and the durability of its high-margin services, while accepting greater concentration in aviation and a relatively high valuation. The new GE426 Air Force design contract modestly reinforces the defense narrative and helps diversify a bit away from commercial exposure, but it does not change that the near term swing factor is execution on major engine ramps and supply chain stability, with inflation and input bottlenecks still the key risk.

The most relevant recent development alongside GE426 is Seaport Research Partners’ new coverage, which highlights how defense wins could become a more important counterweight if investors grow more cautious on the commercial aftermarket cycle. Seaport’s focus on defense as an additional earnings driver fits this contract’s tilt toward autonomous combat platforms, and it gives helpful context for how new programs like GE426 might influence sentiment around GE’s mix of commercial and defense cash flows over time.

Yet beneath the excitement around new defense engines, investors should be aware that GE’s higher debt load and execution risk on complex programs could...

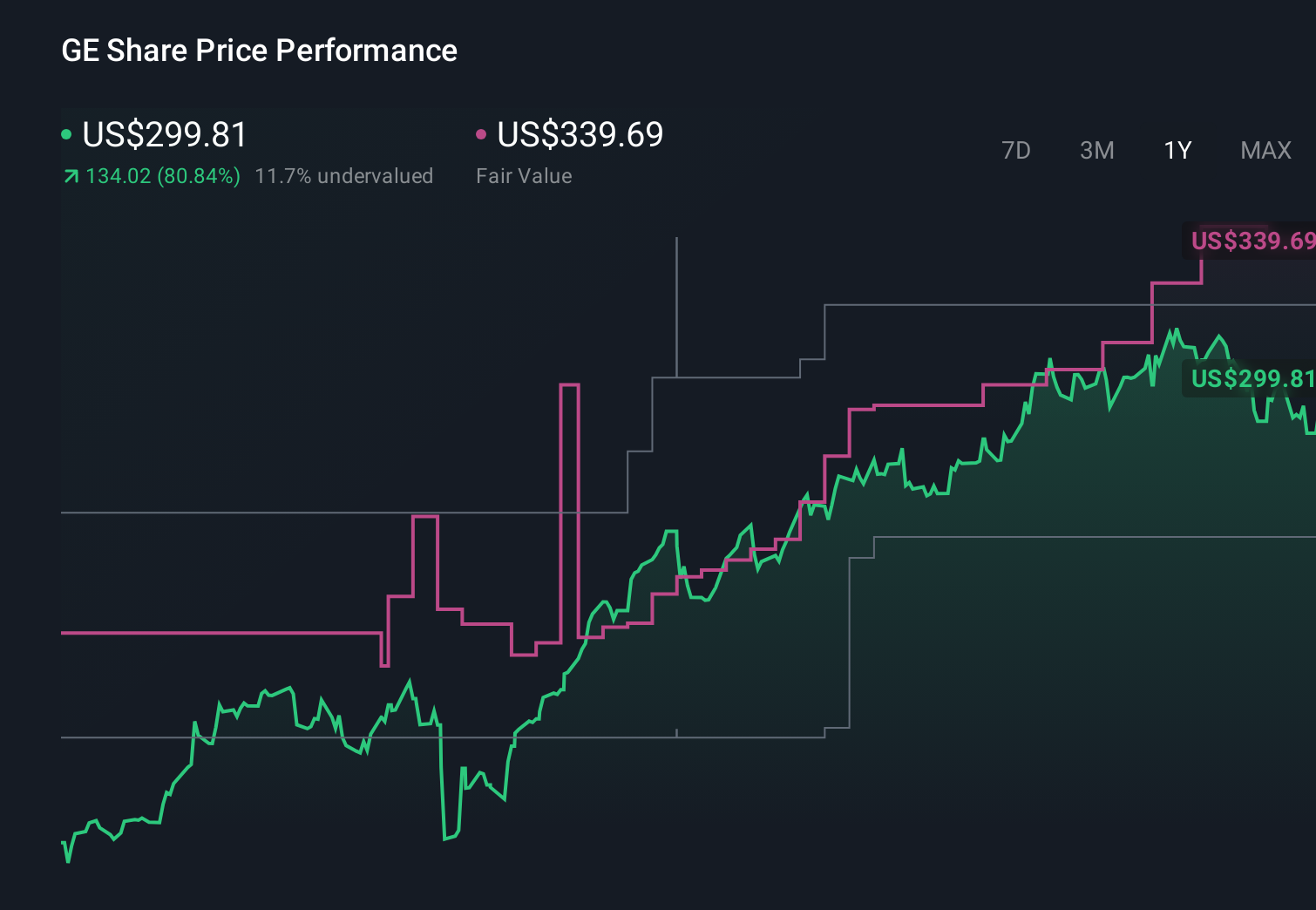

General Electric's narrative projects $59.2 billion revenue and $10.8 billion earnings by 2029.

Uncover how General Electric's forecasts yield a $350.45 fair value, a 10% upside to its current price.

Exploring Other Perspectives

Some of the lowest-rated analysts were already cautious, assuming only 7 percent annual revenue growth and earnings of about US$10.4 billion by 2029, and the GE426 news could either soften or reinforce those concerns around alternative propulsion and climate policy pressure, so as a shareholder you should weigh how your own expectations compare with these more pessimistic views.

Explore 8 other fair value estimates on General Electric - why the stock might be worth 22% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your General Electric research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free General Electric research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate General Electric's overall financial health at a glance.

Seeking Other Investments?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Capitalize on the AI infrastructure supercycle with our selection of the 47 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.