Does HPE’s Recent Cloud and AI Push Signal More Upside After a 25% Stock Surge?

Hewlett Packard Enterprise Co. HPE | 24.09 | +1.20% |

- Wondering if Hewlett Packard Enterprise is undervalued or ready for a surge? You are not alone, and today we are diving straight into what investors need to know about its potential worth.

- The stock has climbed an impressive 25.0% over the past year, with gains of 13.7% year-to-date and a strong 86.7% return over three years. This hints at optimism and renewed attention from the market.

- Recently, Hewlett Packard Enterprise has been making headlines for its focus on expanding GreenLake cloud services and forming partnerships in AI and data infrastructure. Both of these are key drivers that have sparked investor interest and contributed to shifting its risk and growth profile.

- When it comes to value, Hewlett Packard Enterprise scores a solid 3 out of 6 on our checks for being undervalued. How do these methods compare, and could there be an even more insightful way to evaluate its worth? Let’s break it all down, and stick around for a smarter approach to valuation at the end.

Approach 1: Hewlett Packard Enterprise Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future free cash flows and discounting them back to today's value. This method provides a way to look past short-term earnings swings by focusing on how much cash the business can generate over the long run.

For Hewlett Packard Enterprise, the latest reported Free Cash Flow stands at negative $344 Million. However, analysts expect a strong recovery, projecting Free Cash Flow to reach about $3.6 Billion by 2029 as the company grows its cloud and AI segments. These future numbers are based on a mix of analyst consensus for the next few years, with Simply Wall St extrapolating out to a decade. Over ten years, cash flows are forecasted to grow steadily, supporting the long-term value case.

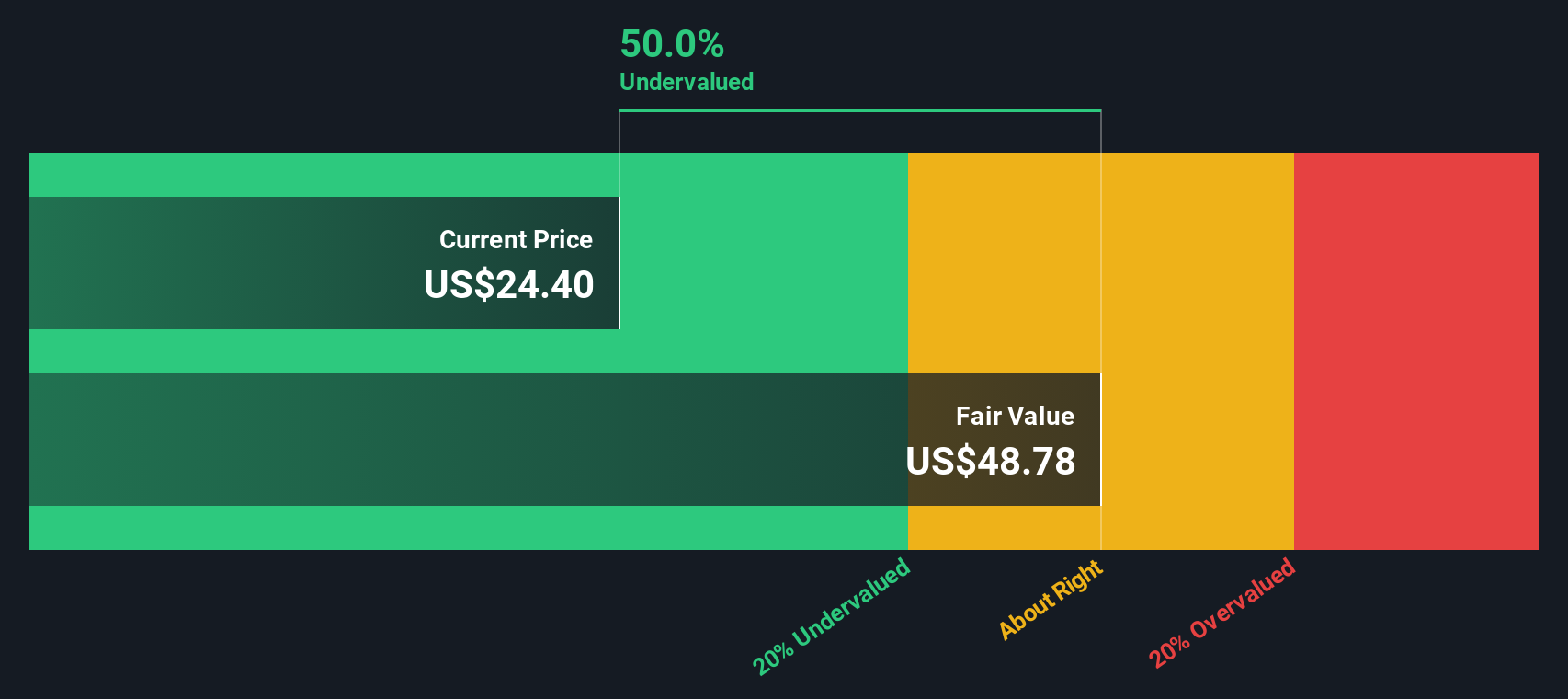

According to this DCF model, Hewlett Packard Enterprise's estimated fair value is $35.66 per share. Based on the current share price, this suggests the stock is trading at a 31.5% discount, indicating significant undervaluation.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Hewlett Packard Enterprise is undervalued by 31.5%. Track this in your watchlist or portfolio, or discover 840 more undervalued stocks based on cash flows.

Approach 2: Hewlett Packard Enterprise Price vs Earnings (P/E)

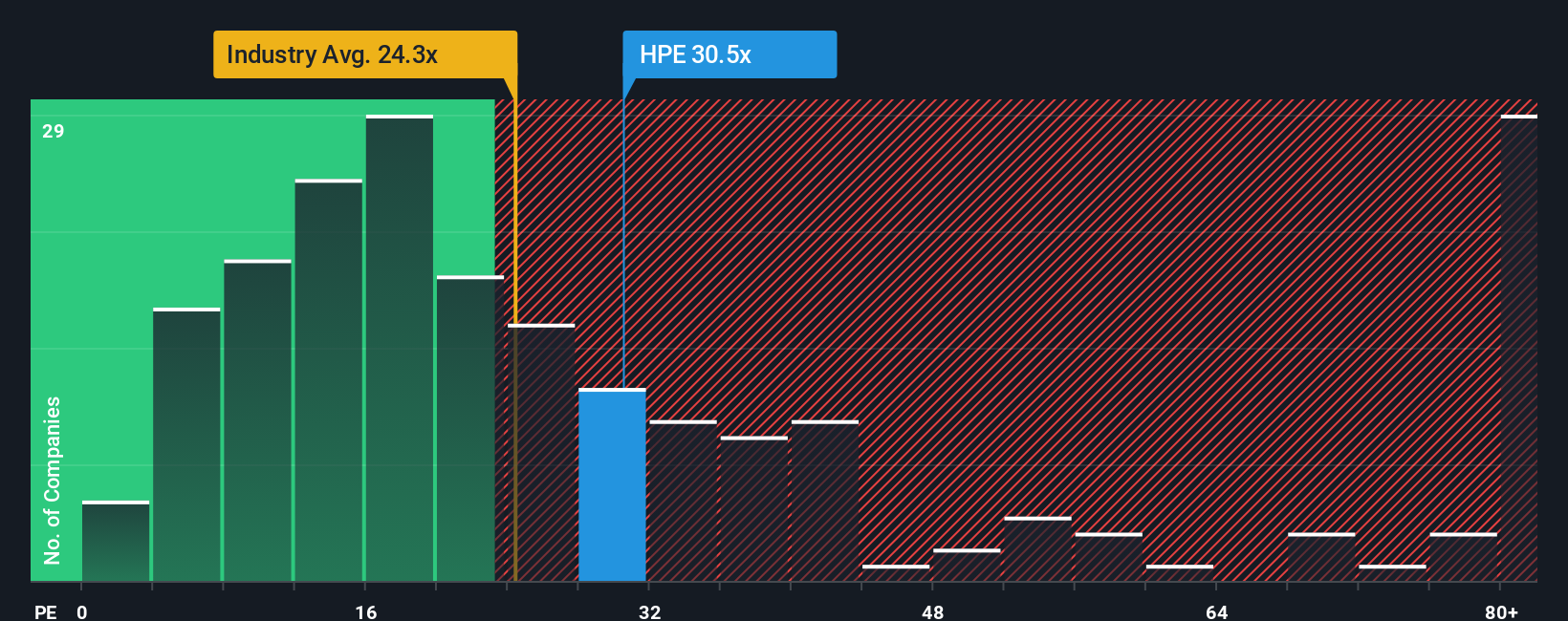

When it comes to valuing established, profitable companies like Hewlett Packard Enterprise, the Price-to-Earnings (P/E) ratio is often the go-to metric. The P/E ratio simply measures how much investors are willing to pay today for a dollar of the company’s earnings. It is particularly useful because it captures market expectations about the company’s future earnings growth and perceived risks.

A company with strong growth prospects or lower risk typically commands a higher "normal" P/E ratio. On the other hand, companies facing uncertainty or slow growth usually trade at lower multiples. For context, Hewlett Packard Enterprise currently trades at a P/E of 28.4x, above the Tech industry average of 23.1x and the average of its peers at 20.4x. This indicates investors are optimistic about HPE's future earnings growth or see it as less risky compared to rivals.

Simply Wall St introduces the proprietary "Fair Ratio," which for Hewlett Packard Enterprise is 44.6x. The Fair Ratio is considered a better benchmark than peer or industry averages, as it adjusts for key company-specific factors like earnings growth, profit margins, risk profile, industry group, and market capitalization. This holistic approach gives a more tailored and realistic view of what a fair multiple should look like for HPE.

Comparing HPE’s current P/E of 28.4x to its Fair Ratio of 44.6x, the stock appears to be trading well below what would be considered fair given its growth and risk profile. This suggests the shares may still have more upside potential.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1414 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Hewlett Packard Enterprise Narrative

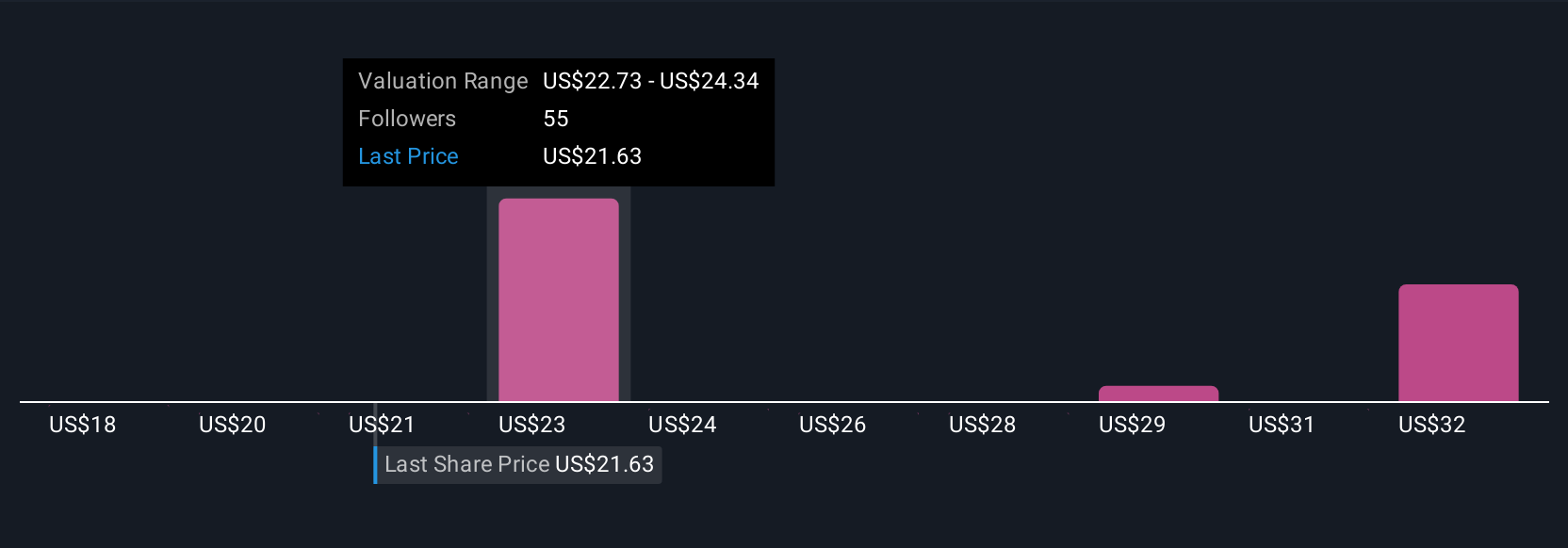

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives. A Narrative is your personal story about a company, connecting the business’s future potential (like projected revenue, earnings, or margins) to a fair value and, ultimately, to your own investing decisions. On Simply Wall St’s Community page, Narratives allow anyone to share their forecast, beliefs, and valuation assumptions in a simple, interactive format used by millions of investors. Narratives bridge the gap between numbers and conviction, helping you weigh whether to buy or sell by letting you compare Fair Value estimates (from your own or others’ Narratives) to the current price. These are automatically kept up to date whenever new information emerges, such as news or earnings releases.

For example, some investors see Hewlett Packard Enterprise’s recent AI and cloud advances as catalysts for strong revenue growth and higher profit margins, supporting optimistic fair value targets as high as $30 per share. Others are more cautious, highlighting risks from legacy hardware or debt, and set lower values down to $19 per share. With Narratives, you can compare the logic, data, and conviction behind either perspective and confidently choose your own path.

Do you think there's more to the story for Hewlett Packard Enterprise? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.