Does Indonesia’s Telaga Ranu Geothermal Win Reshape The Bull Case For Ormat Technologies (ORA)?

Ormat Technologies, Inc. ORA | 112.00 | +0.99% |

- Earlier this week, Ormat Technologies, Inc. announced it had been awarded the Telaga Ranu Geothermal Working Area in Halmahera, North Maluku, securing long-term rights to explore and potentially develop up to 40MW of baseload geothermal capacity in Indonesia’s feed-in tariff zone.

- This concession deepens Ormat’s presence in Indonesia’s energy transition program, adding a regulated-tariff project that could enhance the company’s long-term international development pipeline and revenue visibility.

- Next, we will examine how securing the Telaga Ranu concession within Indonesia’s favorable feed-in tariff framework influences Ormat’s existing investment narrative.

Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

Ormat Technologies Investment Narrative Recap

To own Ormat, you need to believe in its ability to grow recurring revenues from long-lived geothermal, solar and storage assets while managing high capital intensity and operational complexity. The Telaga Ranu award modestly reinforces the long-term development pipeline, but it does not change that the most important near term focus remains execution and margins in the existing electricity segment, while balance sheet strain and funding costs are still the biggest current risk.

Among the recent announcements, the Arrowleaf solar plus storage project in California is particularly relevant. It shows Ormat already executing on hybrid renewable projects with long term contracts, similar to how Telaga Ranu would need to be commercialized. Together, Arrowleaf and Telaga Ranu illustrate how the growing project pipeline can support earnings over time, even as investors weigh funding needs and potential pressure from regulatory changes.

Yet investors should be aware that rising capital needs and a net debt load near 4.4x EBITDA could...

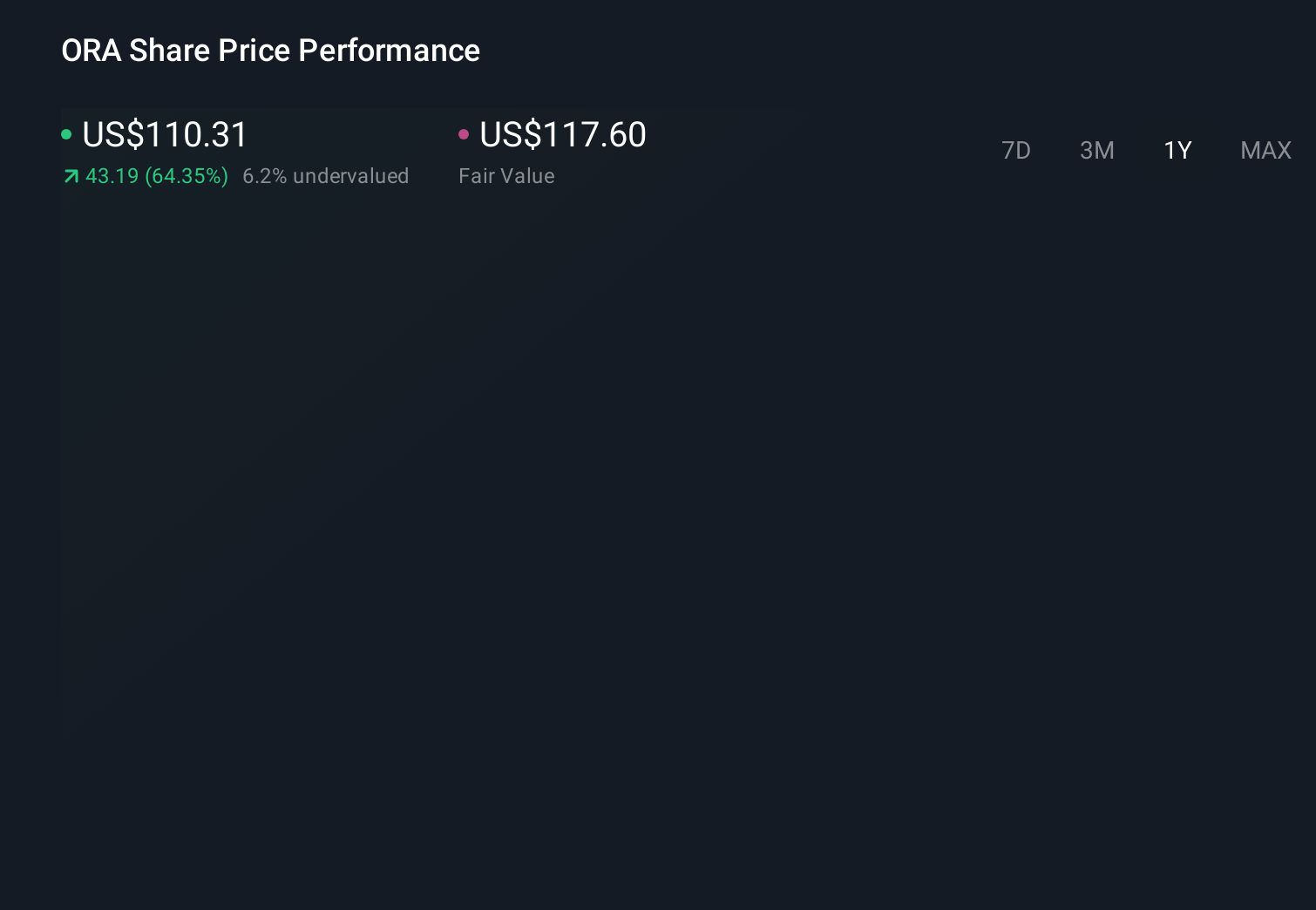

Ormat Technologies' narrative projects $1.2 billion revenue and $171.7 million earnings by 2028.

Uncover how Ormat Technologies' forecasts yield a $121.40 fair value, a 5% upside to its current price.

Exploring Other Perspectives

Four fair value estimates from the Simply Wall St Community span roughly US$24 to US$121 per share, underscoring how far opinions can diverge. You should weigh these against the concentrated risk around Ormat’s high capital expenditure and leverage, and consider how different funding conditions could affect future project economics and overall performance.

Explore 4 other fair value estimates on Ormat Technologies - why the stock might be worth as much as $121.40!

Build Your Own Ormat Technologies Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Ormat Technologies research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Ormat Technologies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ormat Technologies' overall financial health at a glance.

Interested In Other Possibilities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 38 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.