Does Leadership Change And Margin Pressure Shift The Bull Case For Hershey’s (HSY) Profit Story?

Hershey Company HSY | 0.00 |

- The Hershey Company recently announced that its US President, Andrew Archambault, will leave the business on May 1, 2026, while the firm also refreshes its sustainability approach to reflect a growing salty snacks portfolio and tighter regulatory expectations.

- At the same time, analysts are increasingly focused on Hershey’s declining unit sales and margin pressure, raising questions about how effectively the company can translate revenue growth into profitable performance.

- We’ll now examine how concerns around higher input costs and margin pressure affect Hershey’s previously outlined investment narrative and earnings outlook.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Hershey Investment Narrative Recap

To own Hershey today, you need to believe its brands, innovation pipeline, and diversification into snacks can offset weak unit trends, margin pressure, and high input costs. The most important near term catalyst is how effectively new products and pricing can stabilize volumes and margins, while the biggest current risk is sustained cost inflation in cocoa and other commodities. The announced departure of the US President and sustainability refresh do not appear to materially change that near term setup.

The sustainability update, which now explicitly covers Hershey’s growing salty snacks portfolio and tighter regulatory expectations, is the most relevant recent announcement. It directly intersects with concerns about higher input costs and potential future compliance spending, while also tying into longer term catalysts around brand resilience and the expansion of snacks beyond chocolate, where pricing, packaging, and innovation may offer more levers to protect profitability.

Yet beneath the brand strength, there is a cost and margin story here that investors should be aware of, especially around...

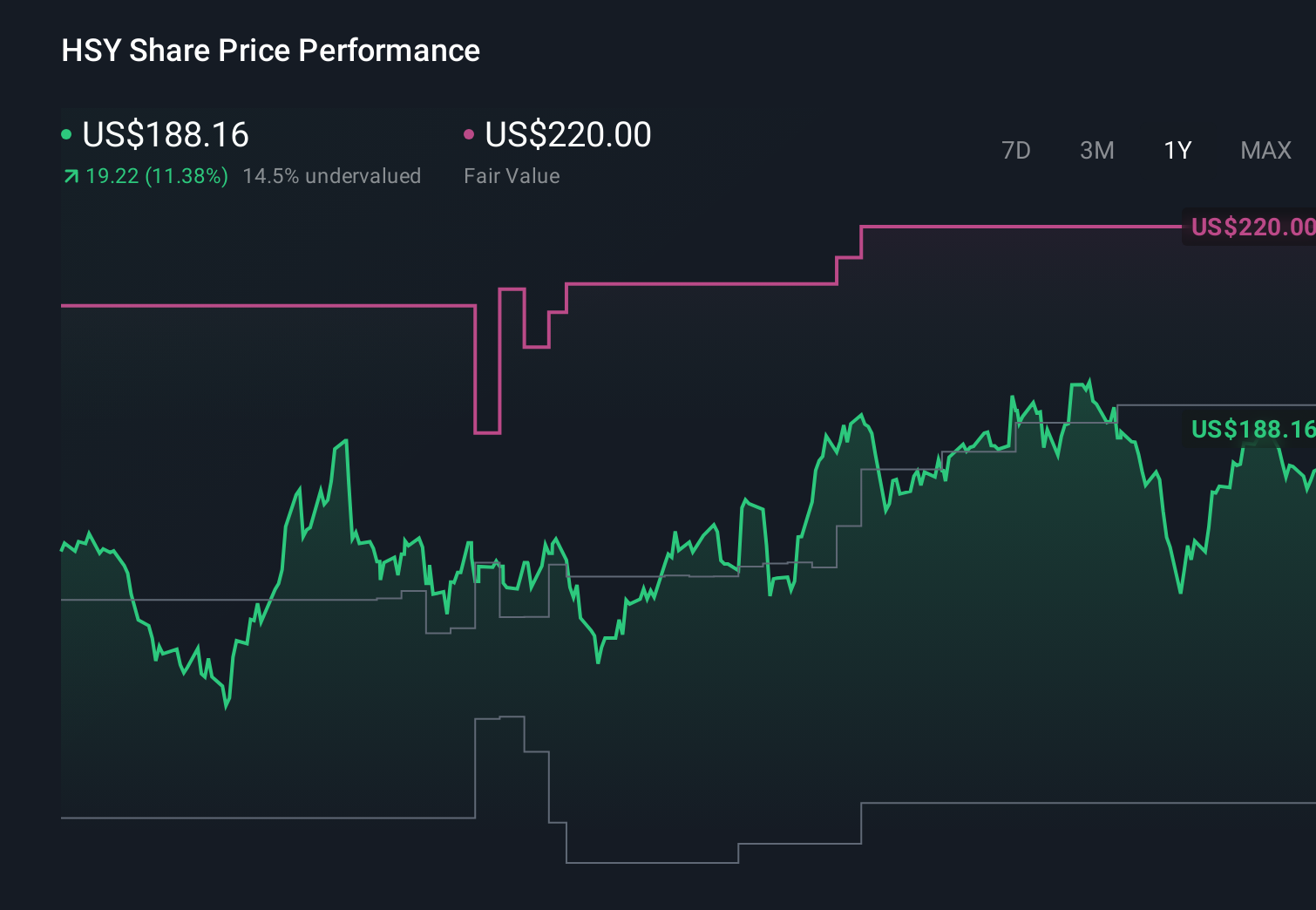

Hershey's narrative projects $12.9 billion revenue and $2.1 billion earnings by 2029. This requires 3.4% yearly revenue growth and roughly a $1.2 billion earnings increase from $883.3 million today.

Uncover how Hershey's forecasts yield a $227.78 fair value, a 19% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts paint a much harsher picture than consensus, with scenarios like earnings falling to about US$1.4 billion even as tariffs ease, reminding you that views on Hershey’s future can differ widely and that both the new leadership changes and input cost pressure could still reshape those expectations.

Explore 4 other fair value estimates on Hershey - why the stock might be worth 16% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Hershey research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Hershey research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Hershey's overall financial health at a glance.

Curious About Other Options?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Find 56 companies with promising cash flow potential yet trading below their fair value.

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- Capitalize on the AI infrastructure supercycle with our selection of the 38 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.