Does Lucid’s CarPlay and Android Auto Rollout Signal a Deeper Software Strategy Shift for LCID?

Lucid LCID | 9.96 | +4.18% |

- Lucid Group has begun rolling out Apple CarPlay and Android Auto via a complimentary over-the-air Lucid UX 3.5 update to Gravity SUVs in North America, with Middle East and Europe deployments scheduled for later in March, while all new Gravity models now include this smartphone integration as standard alongside Air sedans.

- This enhanced connectivity, combined with Lucid’s broader technology focus and upcoming Investor Day, underscores how software updates and partnerships are central to its EV value proposition.

- With Apple CarPlay and Android Auto now standard on Lucid Gravity, we’ll examine how this connectivity push reshapes Lucid’s investment narrative.

Explore 22 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Lucid Group Investment Narrative Recap

To own Lucid today, you generally have to believe its technology focused EV strategy, anchored by Gravity and Air plus software centric features, can eventually support a path toward better margins and a stronger balance sheet. The CarPlay and Android Auto rollout fits that software story, but it does not materially change the near term picture where Investor Day remains the key catalyst and cash burn and dilution risk still loom largest.

The most relevant recent development alongside this connectivity update is Lucid’s upcoming Investor Day, which is expected to outline how management sees the transition from an early stage EV builder to a scaled automaker. In that context, CarPlay and Android Auto help reinforce Lucid’s pitch as a tech forward brand just as the company prepares to talk through production plans, robotaxi partnerships and financial targets that many shareholders are watching closely.

Yet behind the promise of Gravity’s software upgrades, investors should still be aware of Lucid’s heavy dependence on external capital and...

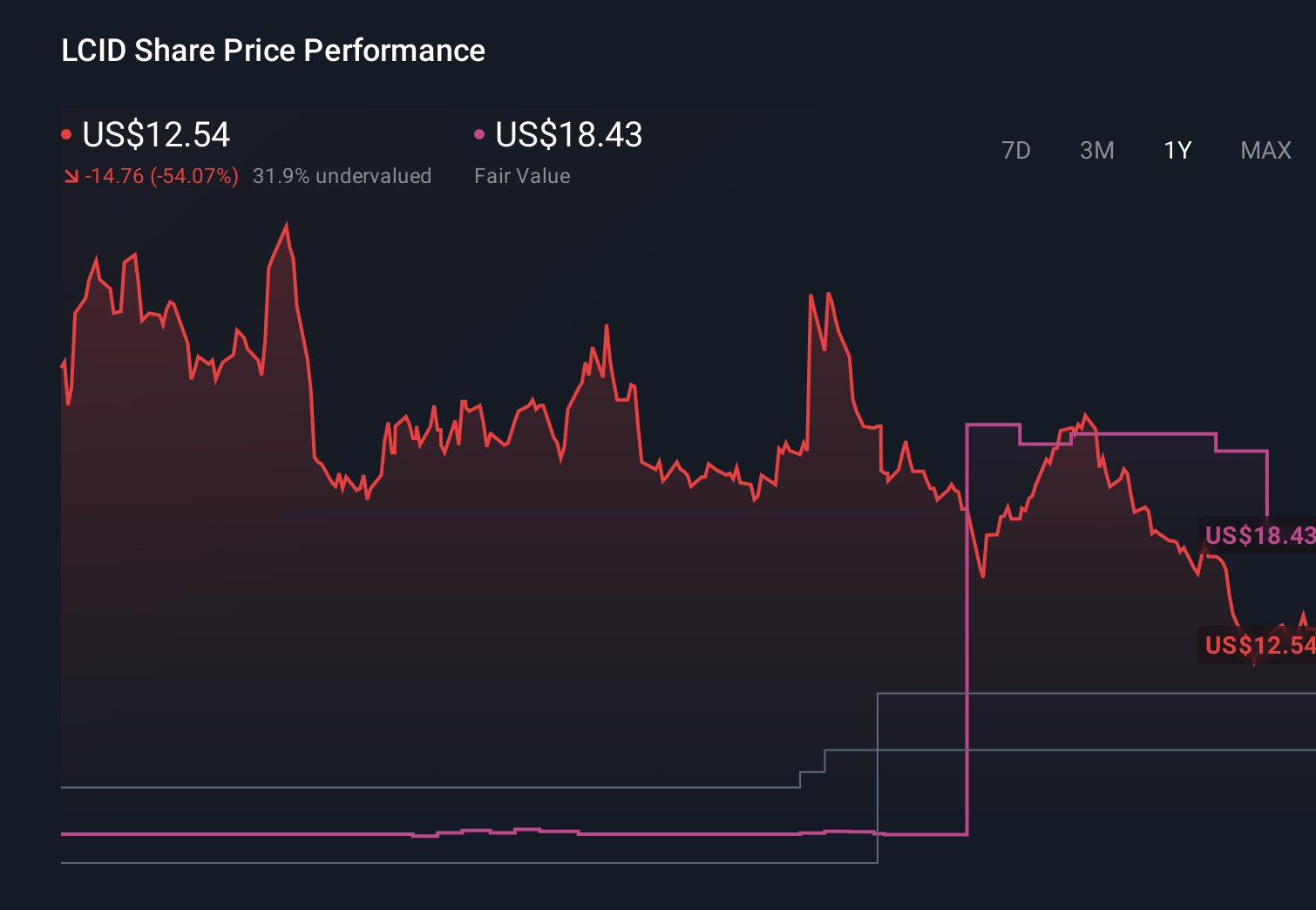

Lucid Group’s narrative projects $5.6 billion revenue and $285.8 million earnings by 2028. This implies 82.4% yearly revenue growth and an earnings increase of roughly $3.4 billion from -$3.1 billion today.

Uncover how Lucid Group's forecasts yield a $16.67 fair value, a 56% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenue could climb toward US$9.2 billion by 2028, and this new software push may eventually feed into that higher growth and technology licensing story, but it also contrasts sharply with ongoing concerns about chronic cash burn that could still reshape how you think about Lucid’s risk and reward.

Explore 6 other fair value estimates on Lucid Group - why the stock might be worth 30% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Lucid Group research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Lucid Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Lucid Group's overall financial health at a glance.

Want Some Alternatives?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 50 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.