Does lululemon (LULU) Guidance and Board Shift Hint at a Strategic Reset or Steady Course?

lululemon athletica inc. LULU | 155.72 | -1.95% |

- Earlier this month, lululemon athletica inc. reported fourth-quarter and full-year 2025 results showing slightly higher sales but lower net income and earnings per share, issued 2026 guidance for modest revenue and EPS growth, completed a multi-year share repurchase program, and added former Levi Strauss CEO Chip Bergh to its board.

- An interesting angle is how this mix of softer profitability, cautious guidance, leadership transition, and ongoing board refresh could influence investor confidence in lululemon’s product reset and international expansion plans.

- With guidance pointing to relatively modest revenue growth and EPS expectations, we’ll now examine how this earnings update reframes lululemon’s investment narrative.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

lululemon athletica Investment Narrative Recap

To own lululemon today, you need to believe its product reset and international growth can offset softer U.S. demand, tariff pressure, and recent margin compression. The latest quarter’s flat sales and lower EPS, paired with modest 2026 guidance and an unsettled CEO search, put more weight on execution around new products and trend re-acceleration. The biggest near term catalyst is a successful refresh of core casual and lifestyle lines, while the key risk is that U.S. demand and pricing power keep slipping.

Among the recent updates, the appointment of former Levi Strauss CEO Chip Bergh to the board stands out. His arrival adds apparel and global brand experience just as lululemon leans harder on international expansion and a higher mix of new styles. For investors, this governance change sits alongside cautious guidance and a completed share buyback, and will likely be viewed through the lens of how quickly leadership can restore confidence in earnings quality and growth.

But beneath the surface, the pressure on U.S. demand and margins is something investors should be aware of as they consider whether...

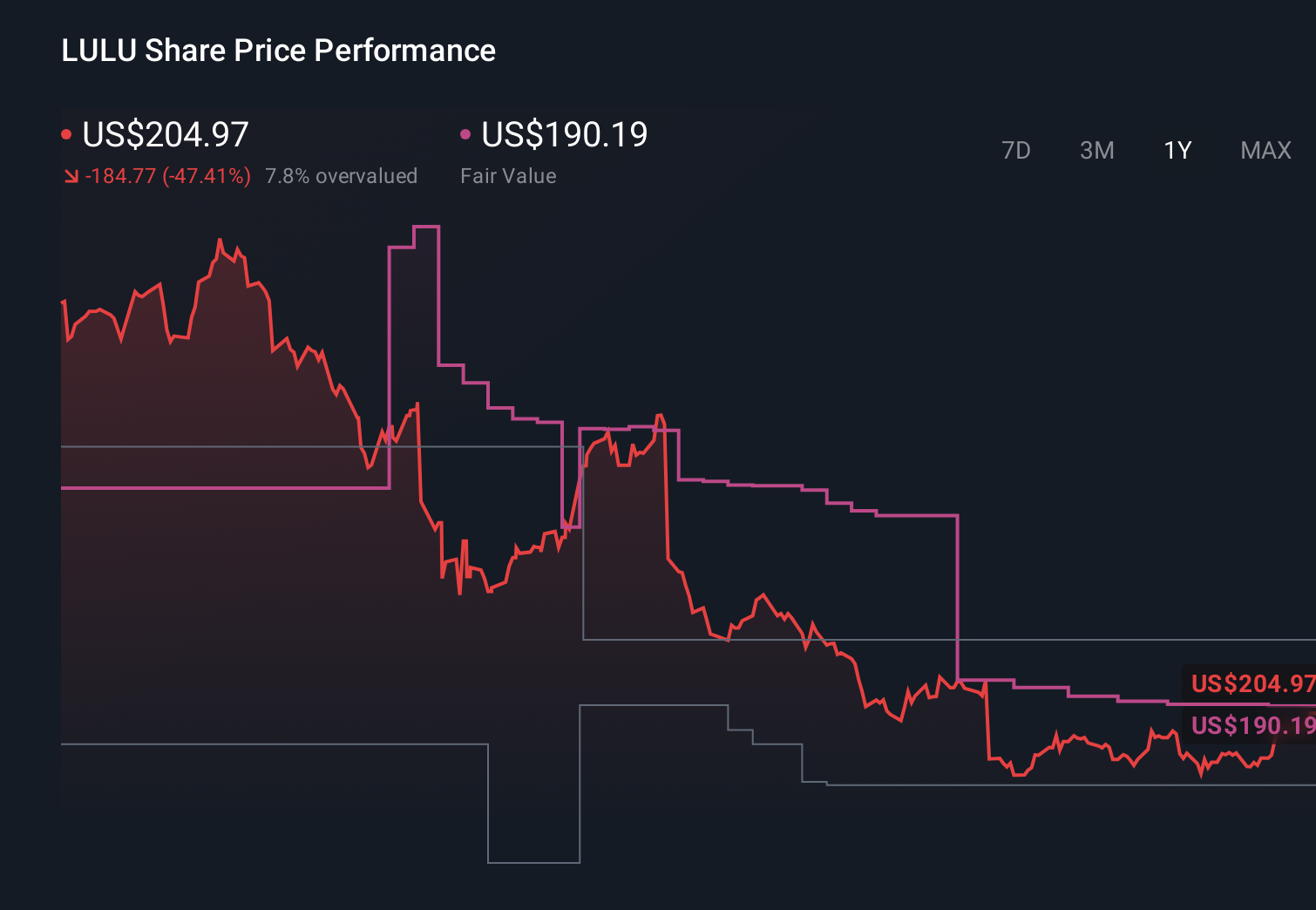

lululemon athletica's narrative projects $12.8 billion revenue and $1.9 billion earnings by 2028. This requires 5.4% yearly revenue growth and a modest $0.1 billion earnings increase from $1.8 billion today.

Uncover how lululemon athletica's forecasts yield a $208.35 fair value, a 43% upside to its current price.

Exploring Other Perspectives

Before this earnings miss, the most optimistic analysts were assuming revenue near US$13.8 billion and earnings around US$2.2 billion, yet softer U.S. demand and margin risks now raise fair questions about how realistic those targets are and what you believe about lululemon’s next chapter.

Explore 41 other fair value estimates on lululemon athletica - why the stock might be worth 7% less than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your lululemon athletica research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free lululemon athletica research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate lululemon athletica's overall financial health at a glance.

Seeking Other Investments?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Find 62 companies with promising cash flow potential yet trading below their fair value.

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.