Does Massive Wrongful Termination Verdict Reshape The Bull Case For Ameris Bancorp (ABCB)?

Ameris Bancorp ABCB | 0.00 |

- Recently, a jury found Ameris Bancorp liable in a wrongful termination case with a total verdict of about US$79.95 million, including roughly US$16.53 million in economic and non-economic damages plus statutory penalties and about US$62.90 million in punitive damages.

- The bank plans to appeal the decision and is assessing how such a large punitive award could affect its financial results, overall condition, and liquidity.

- We’ll now examine how this sizable wrongful termination verdict and Ameris Bancorp’s planned appeal may influence the company’s broader investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Ameris Bancorp Investment Narrative Recap

To own Ameris Bancorp, you need to believe in its ability to keep growing a regional banking franchise while managing credit quality, funding costs, and tighter competition for deposits. The wrongful termination verdict is large relative to a single quarter’s earnings, so the key short term question is how any ultimate payout, legal costs, or regulatory response might affect capital, liquidity, and management focus. If the appeal meaningfully reduces the award, the core earnings story may remain largely unchanged.

The most relevant recent development here is Ameris’s Q1 2026 earnings report, which showed higher net interest income and net income year on year. Those results, together with ongoing share repurchases, had been reinforcing a thesis centered on earnings growth and active capital return. The new legal overhang now sits alongside these financial trends and could influence how investors weigh the appeal outcome against the company’s recent profitability and capital management.

Yet beneath the earnings strength, investors should be aware of how a large legal judgment might interact with Ameris’s concentrated exposure to cyclical lending and...

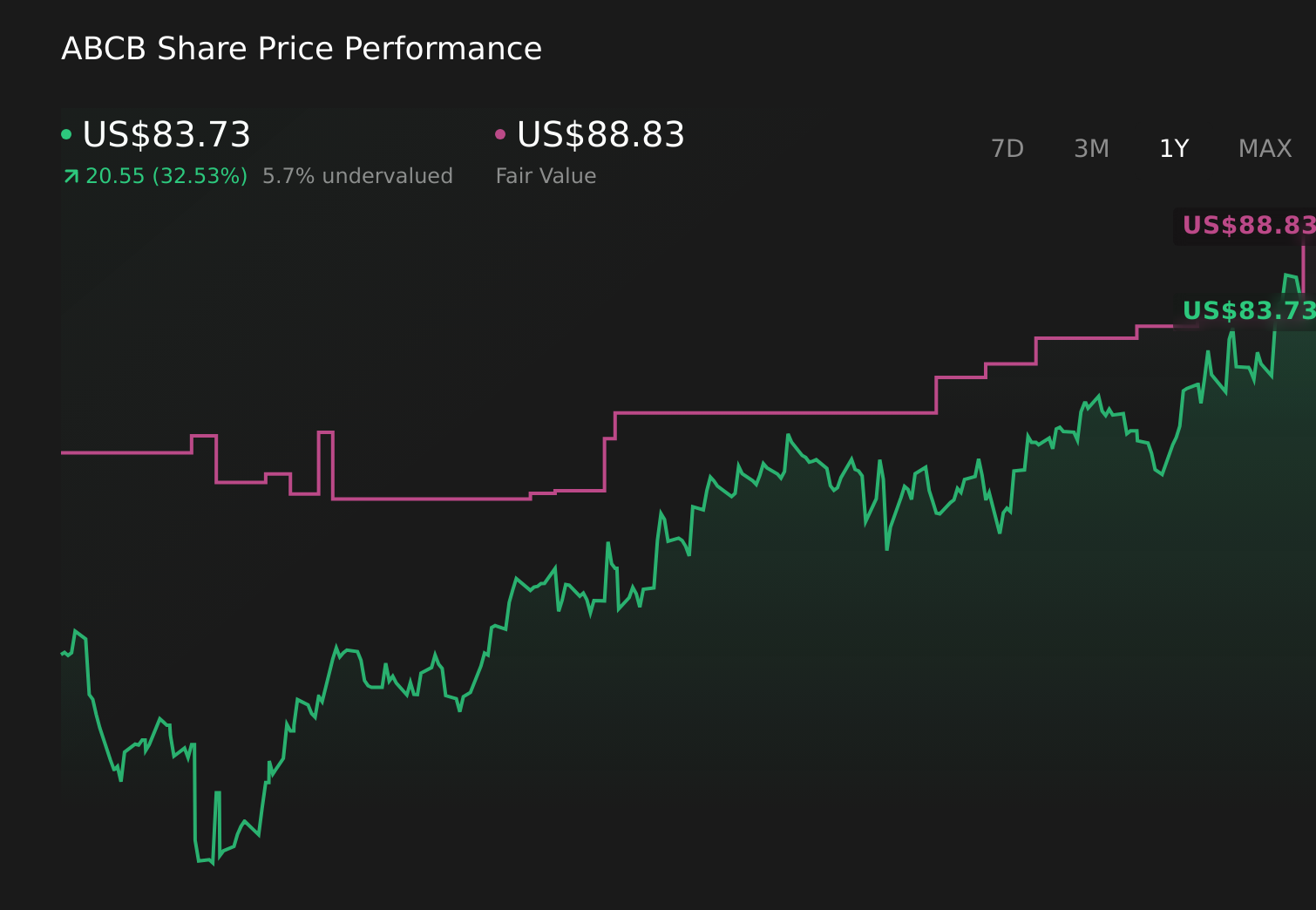

Ameris Bancorp's narrative projects $1.6 billion revenue and $502.9 million earnings by 2029. This requires 9.9% yearly revenue growth and an earnings increase of about $68.2 million from $434.7 million today.

Uncover how Ameris Bancorp's forecasts yield a $93.86 fair value, a 6% upside to its current price.

Exploring Other Perspectives

One Simply Wall St Community member currently pegs Ameris Bancorp’s fair value at US$93.86, underscoring how individual assessments can differ from market pricing. Against that single view, the new wrongful termination verdict adds a fresh layer of legal and capital risk that readers may want to weigh alongside existing concerns about loan and deposit competition.

Explore another fair value estimate on Ameris Bancorp - why the stock might be worth as much as 6% more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Ameris Bancorp research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Ameris Bancorp research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ameris Bancorp's overall financial health at a glance.

Want Some Alternatives?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.