Does New Gulf Drillship Backlog From LLOG Deals Change The Bull Case For Seadrill (SDRL)?

Seadrill Limited SDRL | 0.00 |

- Earlier this week, Harbour Energy subsidiary LLOG Exploration Company LLC announced two ultra-deepwater drilling contract awards with Seadrill in the U.S. Gulf, adding about US$260 million to Seadrill’s backlog through extensions for the West Neptune and a new 270-day program for the West Vela starting in 2026.

- This incremental backlog further secures future utilization for two high-spec drillships, underlining Seadrill’s exposure to longer-duration, higher-value offshore projects in the Gulf.

- We’ll now examine how this US$260 million backlog addition, centered on high-spec Gulf of Mexico drillships, reshapes Seadrill’s investment narrative.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

Seadrill Investment Narrative Recap

To own Seadrill, you have to be comfortable with a cyclical offshore driller that is still working through softer utilization, pricing pressure, and legal overhangs, while relying on a growing multi‑year contract backlog to improve earnings visibility. The new US$260 million LLOG awards modestly ease near term utilization risk for two key Gulf of Mexico drillships but do not remove the broader pressures from competition, idle assets, and unresolved disputes that remain front of mind in the next 12 to 18 months.

The recent 1,095 day extension for West Polaris with Petrobras in Brazil, adding about US$480 million to backlog from 2028, is particularly relevant here. Together with the LLOG awards, it highlights how Seadrill is increasingly anchored by long duration deepwater work in two core basins, which directly ties into the main catalyst of stronger backlog coverage into the back half of the decade, while still leaving investors exposed to contract timing gaps and regional approval delays.

Yet while the new contracts help, investors should be aware that prolonged softness in utilization and day rates could still...

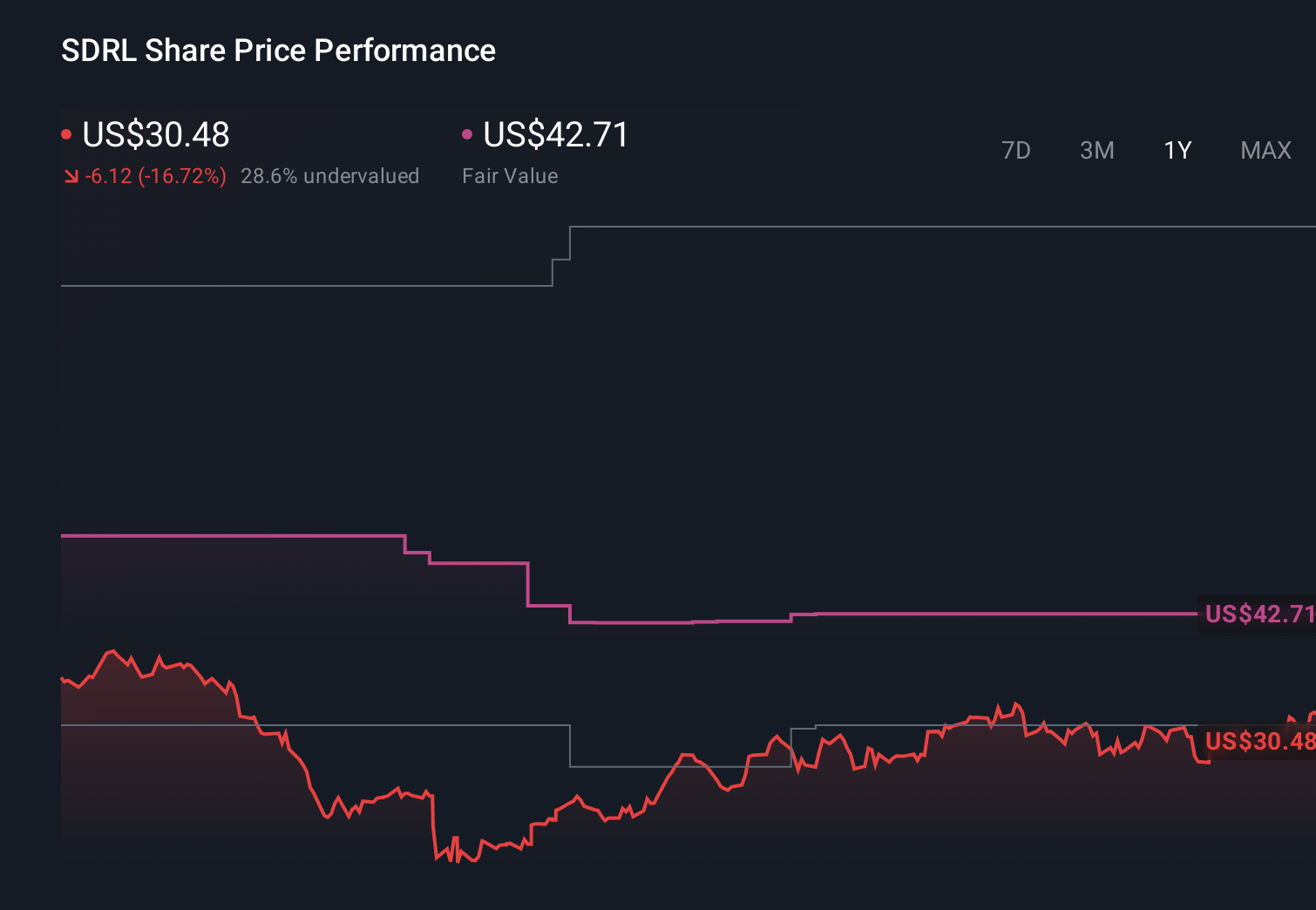

Seadrill's narrative projects $1.6 billion revenue and $231.6 million earnings by 2028. This requires 7.2% yearly revenue growth and about a $154.6 million earnings increase from $77.0 million today.

Uncover how Seadrill's forecasts yield a $43.50 fair value, a 10% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were assuming only about 3.6 percent annual revenue growth to roughly US$1.5 billion by 2029 and earnings of about US$219 million, showing how cautious views on rig demand and potential idle periods can be, especially when set against fresh contract wins like LLOG that may prompt you to revisit which outlook you find more realistic.

Explore 6 other fair value estimates on Seadrill - why the stock might be worth over 8x more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Seadrill research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Seadrill research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Seadrill's overall financial health at a glance.

Seeking Other Investments?

Our top stock finds are flying under the radar-for now. Get in early:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 32 companies in the world exploring or producing it. Find the list for free.

- Find 54 companies with promising cash flow potential yet trading below their fair value.

- The future of work is here. Discover the 35 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.