Does New MUOS Deal And EU Truce Change The Bull Case For Boeing (BA)?

Boeing Company BA | 0.00 |

- Boeing recently secured a US$2.00 billion fixed-price incentive contract from Space Systems Command to build and support two MUOS satellites through 2035, while EU authorities extended a truce in the Boeing–Airbus dispute that keeps retaliatory tariffs on U.S. industrial goods suspended until at least 2029.

- Together, the long-dated defense space award and continued tariff reprieve reinforce Boeing’s mix of government-backed revenue and reduced trade friction across its transatlantic operations.

- We’ll now examine how the MUOS satellite contract and extended EU tariff truce could reshape Boeing’s investment narrative and risk balance.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Boeing Investment Narrative Recap

To own Boeing today, you need to believe the company can turn a large backlog and improving operations into sustained profitability while working down its heavy debt load. The MUOS satellite win and extended EU tariff truce both support backlog quality and trade conditions, but they do not change the fact that 737 production stability remains the key short term catalyst and high leverage remains the central financial risk.

Among recent announcements, the US$2.00 billion MUOS contract is most relevant here, because it further tilts Boeing’s earnings mix toward long term, government-backed defense and space work. That can help offset volatility in commercial programs while management focuses on fixing 737 execution issues and restoring margins in Boeing Commercial Airplanes, but it does not remove the need for consistent, safe deliveries to restore confidence in the core jetliner franchise.

But even with these positives, investors still need to be aware of the unresolved risk around Boeing’s high debt and its impact on...

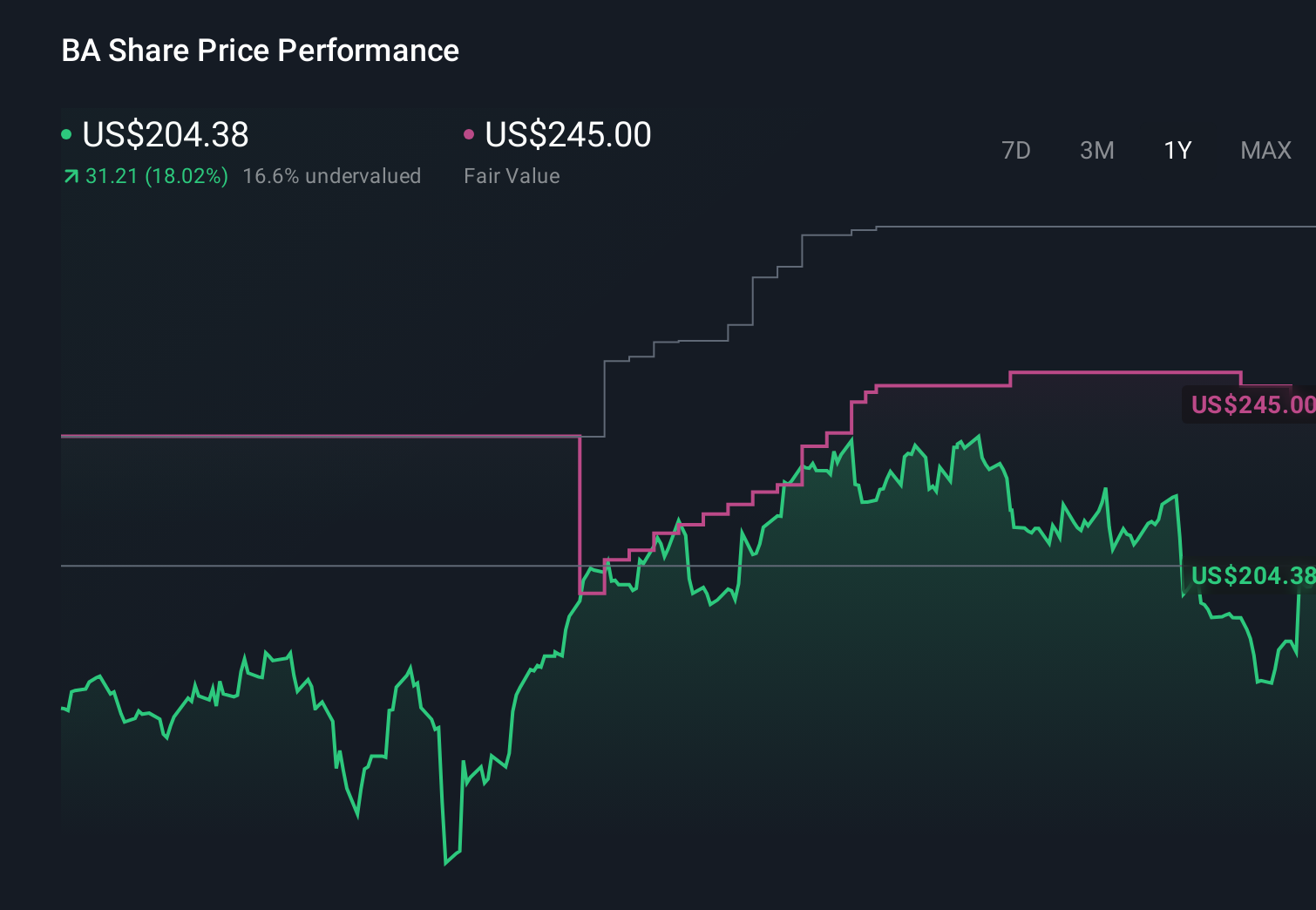

Boeing's narrative projects $125.6 billion revenue and $7.9 billion earnings by 2029. This requires 10.9% yearly revenue growth and a roughly $6.0 billion earnings increase from $1.9 billion today.

Uncover how Boeing's forecasts yield a $270.00 fair value, a 24% upside to its current price.

Exploring Other Perspectives

The most optimistic analysts were already assuming revenue could reach about US$132.7 billion and earnings US$11.7 billion by 2028, so compared with consensus they are effectively betting that satellite wins and wider defense exposure greatly accelerate margin recovery and cash generation, while you weigh that more upbeat story against ongoing concerns about tariffs and export access.

Explore 7 other fair value estimates on Boeing - why the stock might be worth just $270.00!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Boeing research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Boeing research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Boeing's overall financial health at a glance.

Curious About Other Options?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- This technology could replace computers: discover 29 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.