Does Paychex Insider Buying Amid Cautious Analyst Sentiment Reshape the Bull Case for PAYX?

Paychex, Inc. PAYX | 91.70 | +0.87% |

- In recent days, Wells Fargo analyst Jason Kupferberg maintained a Sell rating on Paychex, while corporate insider Joseph Doody, a company director, bought 1,000 shares amid muted 8.7% annual revenue growth and rising expenses that reduced operating margins.

- This combination of cautious analyst coverage and increased insider buying highlights a tension between external skepticism and internal confidence in Paychex’s prospects.

- We’ll now examine how this mix of cautious analyst sentiment and increased insider buying could influence Paychex’s investment narrative.

Find 53 companies with promising cash flow potential yet trading below their fair value.

Paychex Investment Narrative Recap

To own Paychex, you need to believe its human capital management platform can stay relevant for small and mid-sized businesses even as growth moderates and costs rise. The recent mix of a reiterated Sell rating and insider buying does not materially change the near term picture, where the key catalyst remains execution on efficiency and product innovation, and the main risk is pressure on margins from rising expenses and softer client activity.

Among recent announcements, the new US$1,000,000,000 share repurchase authorization stands out, especially alongside insider purchases. For investors watching catalysts, this combination of buybacks and insider buying may reinforce attention on how Paychex balances capital returns with the need to invest in technology and integration to support long term profitability.

Yet behind the insider confidence and buybacks, there is a risk investors should be aware of around rising expenses and margin pressure...

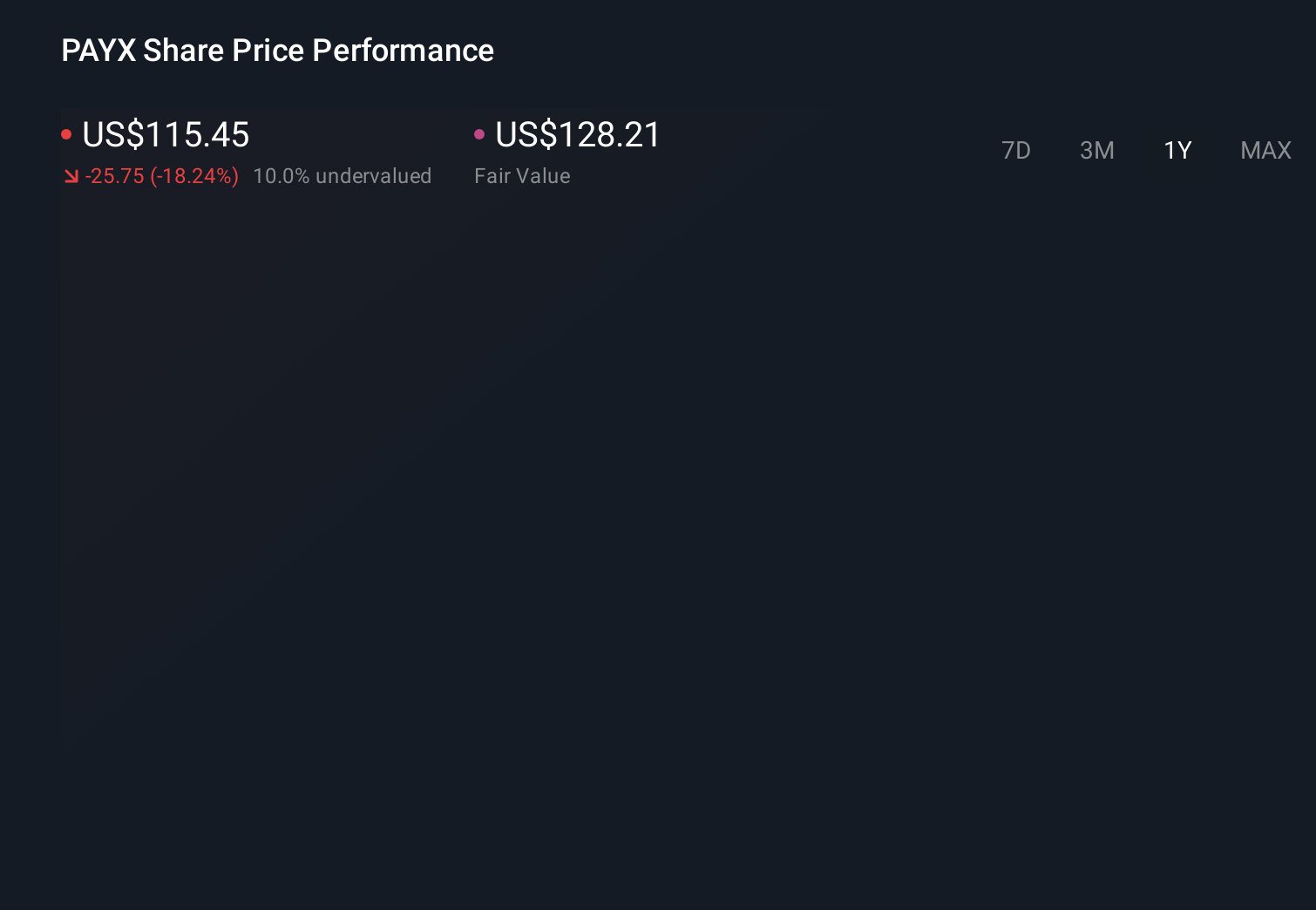

Paychex's narrative projects $7.5 billion revenue and $2.3 billion earnings by 2028. This requires 10.2% yearly revenue growth and about a $0.6 billion earnings increase from $1.7 billion today.

Uncover how Paychex's forecasts yield a $119.07 fair value, a 31% upside to its current price.

Exploring Other Perspectives

Six members of the Simply Wall St Community value Paychex between US$119.07 and US$188.55 per share, showing a wide spread in expectations. You can weigh these views alongside the recent margin compression and cost pressures that are shaping how the business might perform from here.

Explore 6 other fair value estimates on Paychex - why the stock might be worth over 2x more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Paychex research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Paychex research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Paychex's overall financial health at a glance.

Looking For Alternative Opportunities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Invest in the nuclear renaissance through our list of 84 elite nuclear energy infrastructure plays powering the global AI revolution.

- Uncover the next big thing with 30 elite penny stocks that balance risk and reward.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.