Does Pediatrix (MD) Joining Russell Defensive Indexes Recast Its Profile as a Value-Safe Haven?

Pediatrix Medical Group, Inc. MD | 0.00 |

- Pediatrix Medical Group, Inc. (NYSE: MD) was added in June 2026 to both the Russell 2000 Value-Defensive Index and the Russell 2000 Defensive Index, placing the company within key benchmarks tracked by many institutional investors.

- This dual inclusion highlights how the market increasingly views Pediatrix as a defensive healthcare name with characteristics that align with value-oriented, risk-aware investment mandates.

- We’ll now consider how Pediatrix’s addition to the Russell 2000 Defensive indices might influence its existing investment narrative and investor focus.

Find 41 companies with promising cash flow potential yet trading below their fair value.

Pediatrix Medical Group Investment Narrative Recap

To own Pediatrix Medical Group, you need to believe in steady demand for high-acuity neonatal and maternal care while the company manages reimbursement, labor, and portfolio restructuring pressures. Its inclusion in the Russell 2000 Value-Defensive and Defensive indices may broaden the shareholder base and support trading liquidity, but it does not materially change the near term revenue risk from portfolio dispositions or the ongoing challenge of containing salary and physician compensation costs.

The most relevant recent update is the Q1 2026 earnings release, which showed higher sales and net income year over year. That improvement supports the view that revenue cycle efficiencies and operating discipline can partly offset pressures from practice divestitures and tight hospital fee negotiations. However, these financial gains sit alongside rising compensation and restructuring activity, keeping execution risk front and center as investors reassess Pediatrix’s “defensive” label after the index additions.

Yet behind the new defensive index label, there is still meaningful risk around future reimbursement changes that investors should be aware of...

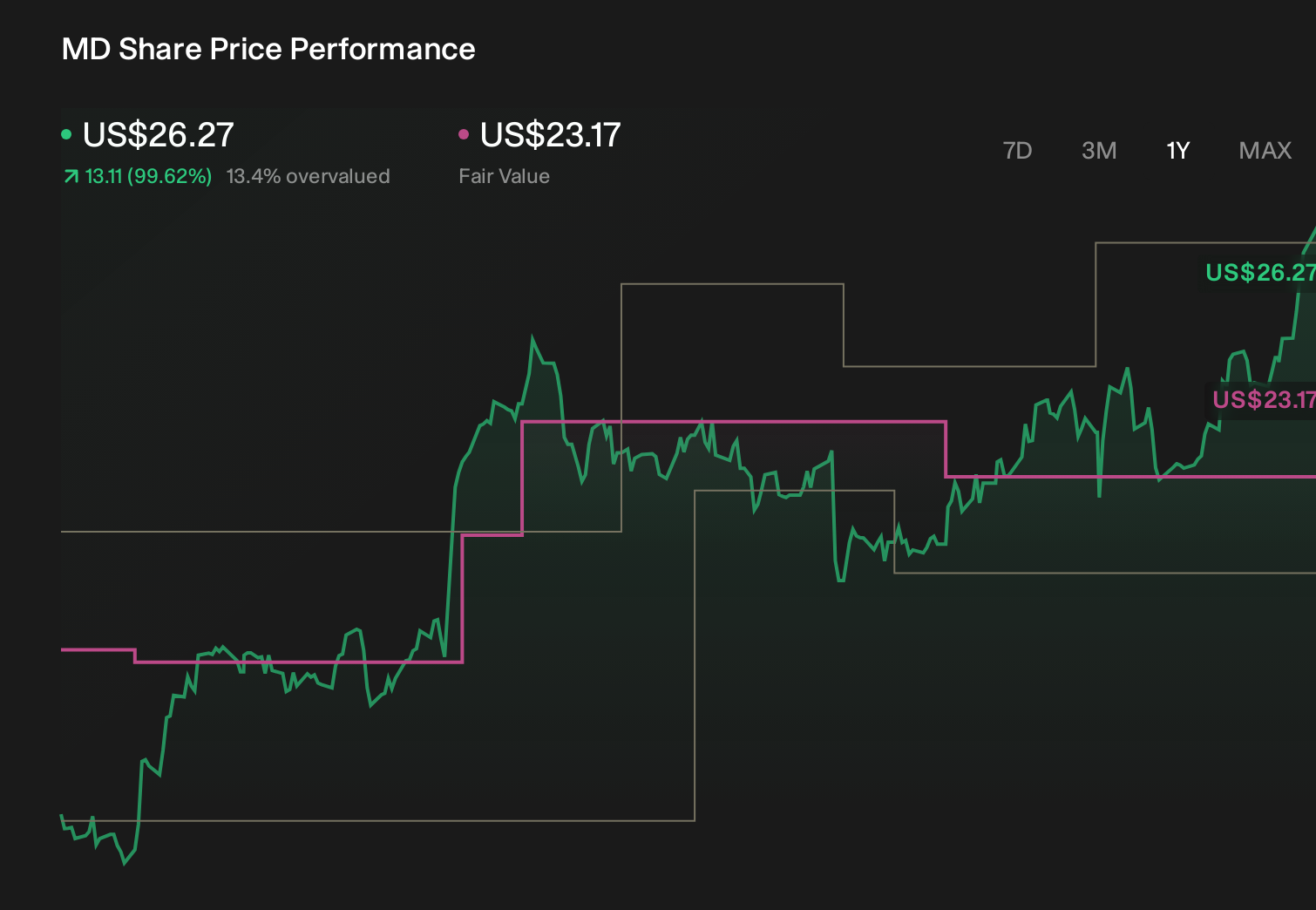

Pediatrix Medical Group's narrative projects $2.1 billion revenue and $171.4 million earnings by 2029. This requires 2.6% yearly revenue growth and about a $6 million earnings increase from $165.4 million today.

Uncover how Pediatrix Medical Group's forecasts yield a $21.33 fair value, a 20% downside to its current price.

Exploring Other Perspectives

While consensus focuses on modest growth and operational fixes, the most optimistic analysts were modeling about US$2.1 billion of revenue and US$184.4 million of earnings by 2029, suggesting that if Russell 2000 defensive inclusion enhances Pediatrix’s profile, the already bullish view of its NICU leverage and cash generation could shift again in light of concentrated neonatal exposure and evolving payment models.

Explore 6 other fair value estimates on Pediatrix Medical Group - why the stock might be worth less than half the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Pediatrix Medical Group research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Pediatrix Medical Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Pediatrix Medical Group's overall financial health at a glance.

Curious About Other Options?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 31 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.