Does Perceived Undervaluation at Baxter (BAX) Recast Its Margin Recovery and Portfolio Optimization Story?

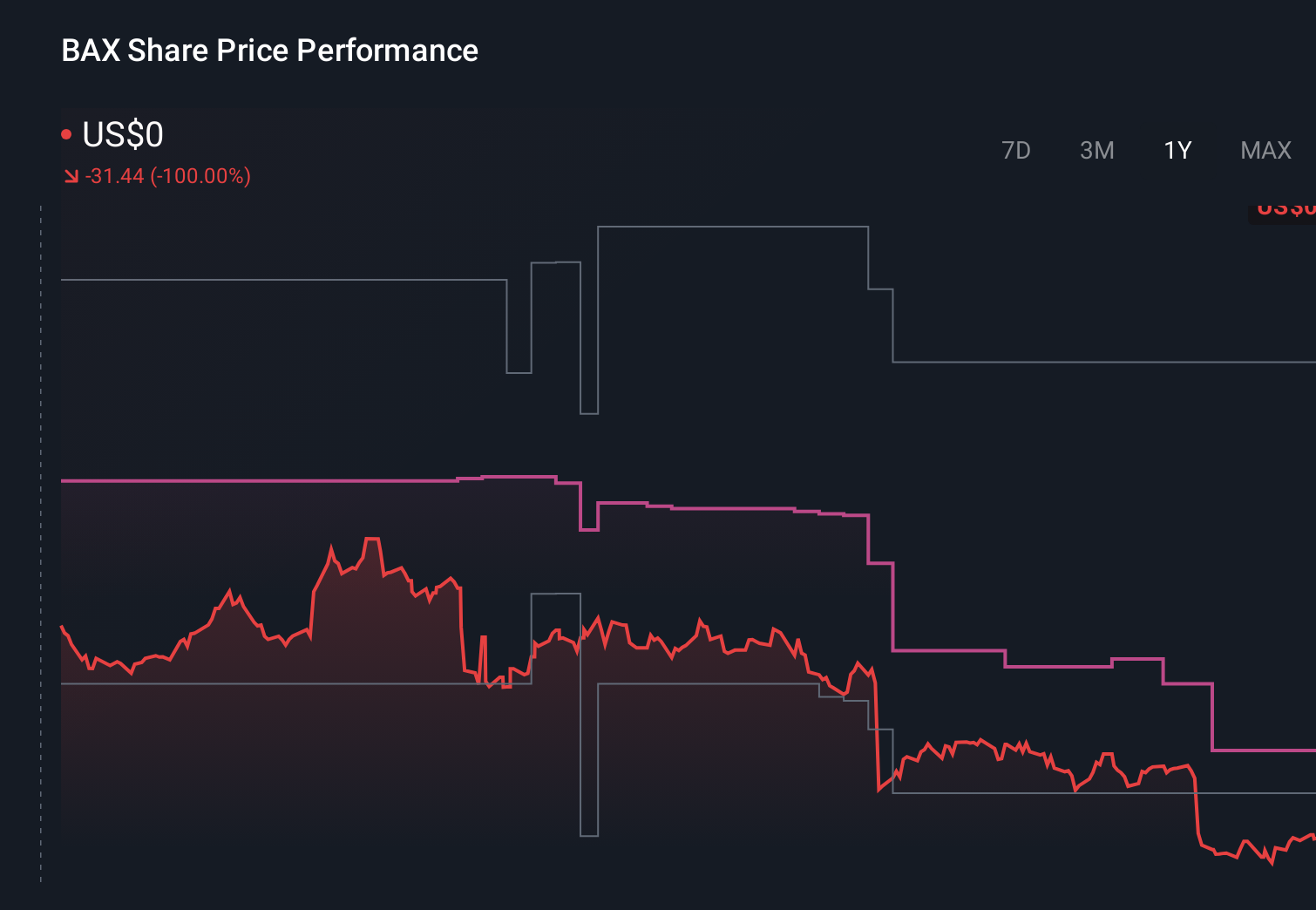

Baxter International Inc. BAX | 0.00 |

- Recent analysis has highlighted that Baxter International is trading well below various estimates of its intrinsic value and its own historical valuation multiples, prompting fresh investor attention in early June 2026.

- The combination of a comparatively low price-to-earnings ratio and an absence of recent insider transactions is feeding a perception that the shares may offer value without obvious internal red flags.

- Next, we will examine how this perceived undervaluation interacts with Baxter International's existing investment narrative around margin recovery and portfolio optimization.

This technology could replace computers: discover 30 stocks that are working to make quantum computing a reality.

Baxter International Investment Narrative Recap

To own Baxter International today, you need to believe the company can restore margins and return to consistent profitability while managing product quality and post‑divestiture cost challenges. The recent indication that the shares trade below several intrinsic value estimates does not materially change the near term focus on margin execution and the key risk around ongoing losses, especially after recent quarters of negative net income.

Against this backdrop, the first quarter 2026 results are particularly relevant. Baxter reported US$2,701 million in sales but a net loss of US$15 million, underlining that margin pressure and cost absorption remain central issues. The apparent valuation discount highlighted in early June 2026 only matters if Baxter can translate modest revenue growth into sustainable earnings improvement and progress on reducing stranded costs after the Kidney Care divestiture.

Yet beneath the perceived discount, investors should be aware that ongoing hospital IV fluid conservation and slower than expected usage recovery could...

Baxter International's narrative projects $12.1 billion revenue and $629.2 million earnings by 2029. This requires 2.2% yearly revenue growth and a $1,610.2 million earnings increase from -$981.0 million today.

Uncover how Baxter International's forecasts yield a $21.54 fair value, a 11% upside to its current price.

Exploring Other Perspectives

While consensus still centers on gradual repair, the most optimistic analysts saw Baxter reaching about US$12.1 billion in revenue and US$766 million in earnings, assuming IV utilization rebounds faster, which shows just how far opinions can differ and how this new valuation signal could prompt a rethink of both bullish and cautious views.

Explore 6 other fair value estimates on Baxter International - why the stock might be worth as much as 72% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Baxter International research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Baxter International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Baxter International's overall financial health at a glance.

Searching For A Fresh Perspective?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.