Does P&G’s Share Price Drop Signal a New Opportunity for Investors in 2025?

Procter & Gamble Company PG | 143.12 | -0.67% |

- Wondering if Procter & Gamble is a smart buy right now? You are not alone. With so many voices out there, getting straight to the real value is more important than ever.

- The stock has dipped slightly over the last week, down 1.7%, and is off 9.9% since the start of the year. It is still up 19.1% over five years, presenting a mixed bag that sparks debate about both risk and growth.

- Lately, headlines have focused on Procter & Gamble's strategic initiatives in sustainable packaging and expansion into emerging markets. These moves are reshaping investor sentiment and may help explain the pressures as well as the optimism impacting the share price this year.

- When it comes to classic valuation measures, Procter & Gamble scores a 3 out of 6 for undervaluation checks, suggesting there is room for debate on its true worth. Before diving into the usual valuation approaches, let’s hint at a smarter, more insightful way to judge value. Stay tuned for that at the end.

Approach 1: Procter & Gamble Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's true value by projecting its future cash flows and discounting them back to today's dollars. This helps investors judge whether a stock is overvalued or undervalued compared to its current trading price.

For Procter & Gamble, current Free Cash Flow stands at $15.4 Billion. Analysts expect this figure to gradually rise, reaching $16.98 Billion by 2028. Looking out over the next decade, further projections estimate free cash flow could approach $21.2 Billion by 2035, with forecasts beyond 2028 extrapolated based on recent trends and industry expectations.

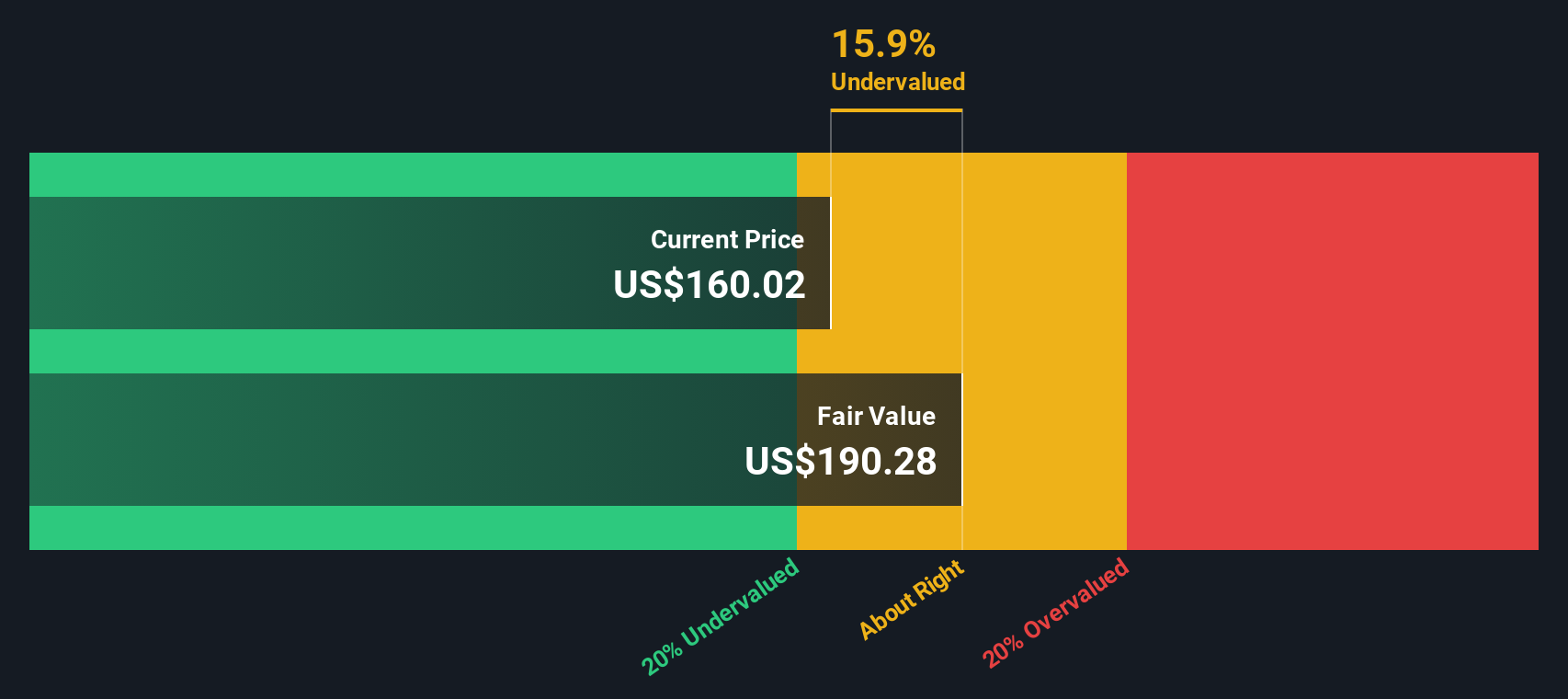

Using this model, the estimated fair value of Procter & Gamble comes to $185.83 per share. This reflects a 19.5% discount relative to the present market price. In simple terms, this suggests the stock is trading about one-fifth below what its future cash generation would justify.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Procter & Gamble is undervalued by 19.5%. Track this in your watchlist or portfolio, or discover 848 more undervalued stocks based on cash flows.

Approach 2: Procter & Gamble Price vs Earnings

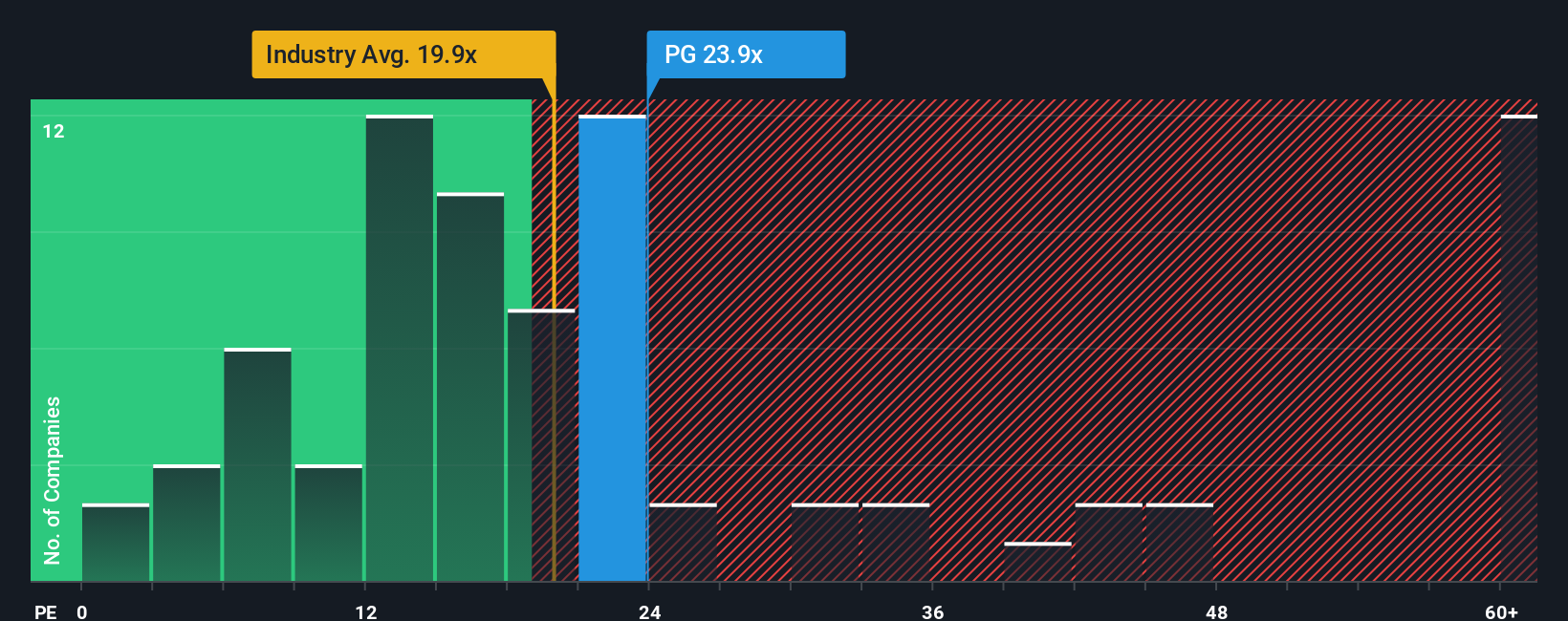

For solidly profitable companies like Procter & Gamble, the Price-to-Earnings (PE) ratio is a widely-used and practical valuation tool. It helps investors compare what they are paying for each dollar of earnings, making it easier to gauge if a stock seems reasonably priced relative to its profit potential.

Growth prospects and perceived risks play a big role in setting what is considered a “fair” PE ratio. More growth and less risk often justify a higher multiple, while companies with slower growth or more uncertainty usually trade at lower PE ratios. Procter & Gamble’s current PE ratio is 21.25x. That sits between the broader Household Products industry average of 18.75x and the peer average of 23.12x. This suggests it is priced slightly higher than the industry, but a bit lower than the typical peer group.

Simply Wall St’s proprietary Fair Ratio for Procter & Gamble is 27.34x. Unlike a simple comparison against peers or the industry, this Fair Ratio accounts for the company’s specific earnings growth outlook, risks, profit margins, industry context, and market cap. This makes it a more holistic measure of value than the classic “apples to apples” approach. It provides a truer sense of what the stock should be worth.

Comparing Procter & Gamble’s current PE of 21.25x to its Fair Ratio of 27.34x, the shares are appearing undervalued by this analysis, which signals potential upside if the company delivers on its expected performance.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1405 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Procter & Gamble Narrative

Earlier we mentioned that there's an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is a unique, investor-driven story about a company’s future, backed not just by personal perspective, but by numbers like fair value estimates, expected revenue, earnings, and profit margins. By linking a company’s story to a financial forecast and then to a fair value, Narratives make it easy to see how different viewpoints translate into concrete actions.

Anyone can create a Narrative using Simply Wall St’s platform, right within the Community page. This approach is accessible to millions of investors. With Narratives, you can compare your fair value estimate and view how it stacks up against the current market price, giving you clarity on when to buy, hold, or sell. Narratives are updated in real time when news or earnings are announced, so your perspective always stays relevant and informed.

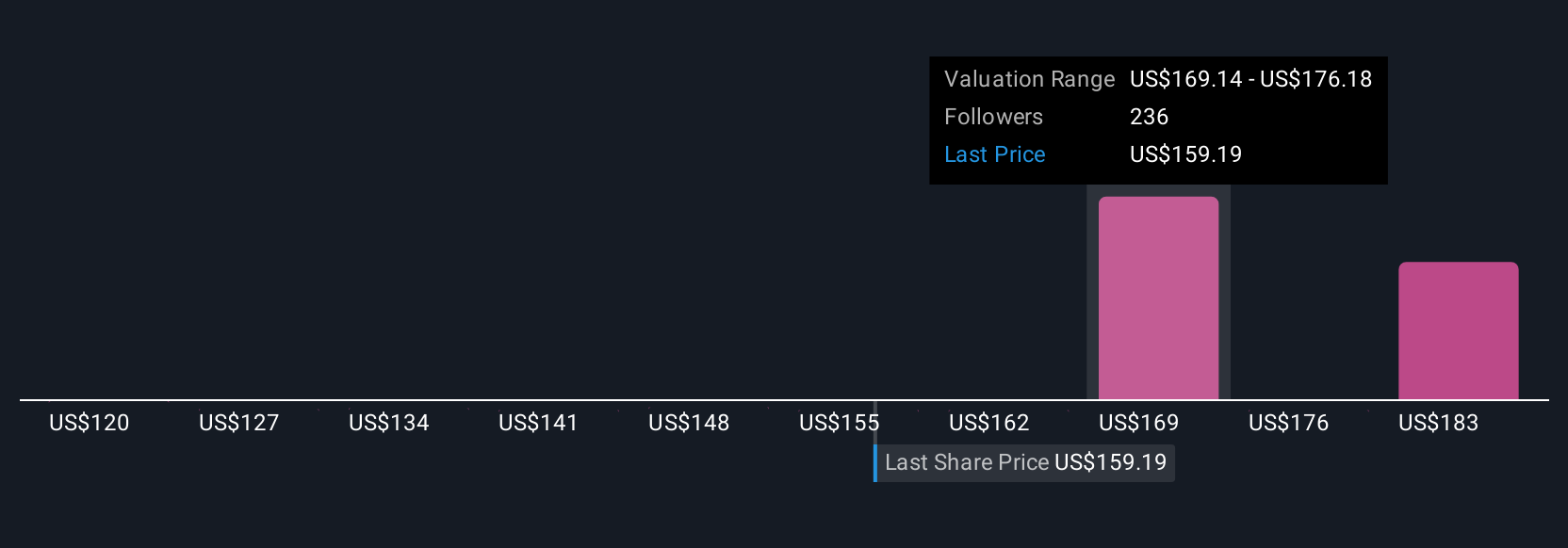

For example, when it comes to Procter & Gamble, one investor might use conservative growth assumptions and see a fair value around $119.81 per share, viewing the stock as overvalued. A more optimistic investor, factoring in strong product innovation or rising consumer confidence, could estimate fair value as high as $186 per share. Narratives let you anchor your investment decisions to your own convictions, empowered by data and shared alongside a community of investors.

For Procter & Gamble, we will make it easy for you with previews of two leading Procter & Gamble Narratives:

Fair Value: $168.64

Undervalued by 11.3%

Expected Revenue Growth: 3.17%

- Investments in product innovation and productivity are expected to increase market share, revenues, and profit margins. Analysts project stable growth as consumer confidence returns.

- This narrative assumes profit margins will expand and share count will decline. These factors may lead to earnings per share growth and support a slightly higher future price-to-earnings ratio.

- Main risks include consumer and retailer volatility, geopolitical tensions, tariffs and cost headwinds, and modest consensus about upside. Analysts’ fair value is only slightly above the current market price.

Fair Value: $119.81

Overvalued by 24.8%

Expected Revenue Growth: 4.68%

- P&G remains a reliable dividend giant but faces slowing growth as it matures. Long-term revenue and free cash flow are expected to track close to the risk-free rate.

- Weighted valuation methods (DCF, DDM, historic yield, and PE) suggest the stock is trading above its fair value, with limited upside from current levels unless earnings or margins improve unexpectedly.

- The stock is considered high quality and stable for income. However, current pricing reflects a premium that could limit future returns unless business momentum improves substantially.

Do you think there's more to the story for Procter & Gamble? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.