Does Positive PANOVA-4 Data Alter the Bull Case For NovoCure’s TTFields Platform (NVCR)?

NovoCure Ltd. NVCR | 10.28 | -2.61% |

- Novocure recently reported that its Phase 2 PANOVA-4 trial of Tumor Treating Fields (TTFields) combined with atezolizumab and chemotherapy for first-line treatment of metastatic pancreatic ductal adenocarcinoma met its primary endpoint, delivering a statistically significant improvement in disease control versus historical controls.

- This outcome adds fresh clinical evidence for TTFields in a highly challenging cancer setting, potentially reinforcing Novocure’s broader effort to expand TTFields into combination regimens across multiple solid tumor indications.

- With TTFields showing improved disease control in metastatic pancreatic cancer, we’ll now examine how this development may influence Novocure’s investment narrative.

AI is about to change healthcare. These 36 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

NovoCure Investment Narrative Recap

To own NovoCure, you need to believe TTFields can become a meaningful treatment backbone across multiple solid tumors, not just a niche GBM therapy. The PANOVA-4 pancreatic data supports that broader-platform view, but it does not change the near term focus on execution in lung cancer and on improving reimbursement. The biggest risk, in my view, remains slow real world adoption and payer uptake, which keep the company unprofitable despite growing revenue.

The recent Japan reimbursement approval for Optune Lua in advanced NSCLC looks especially relevant beside PANOVA-4. Together, they highlight a consistent theme of TTFields being integrated with immunotherapies in difficult cancers, across both regulatory and clinical fronts. While PANOVA-4 is still early stage, investors may watch closely to see whether pancreatic and lung indications together can eventually shift NovoCure’s revenue mix beyond GBM and help address ongoing losses.

Yet beneath the positive trial headlines, investors should be aware that persistent reimbursement and adoption hurdles could still...

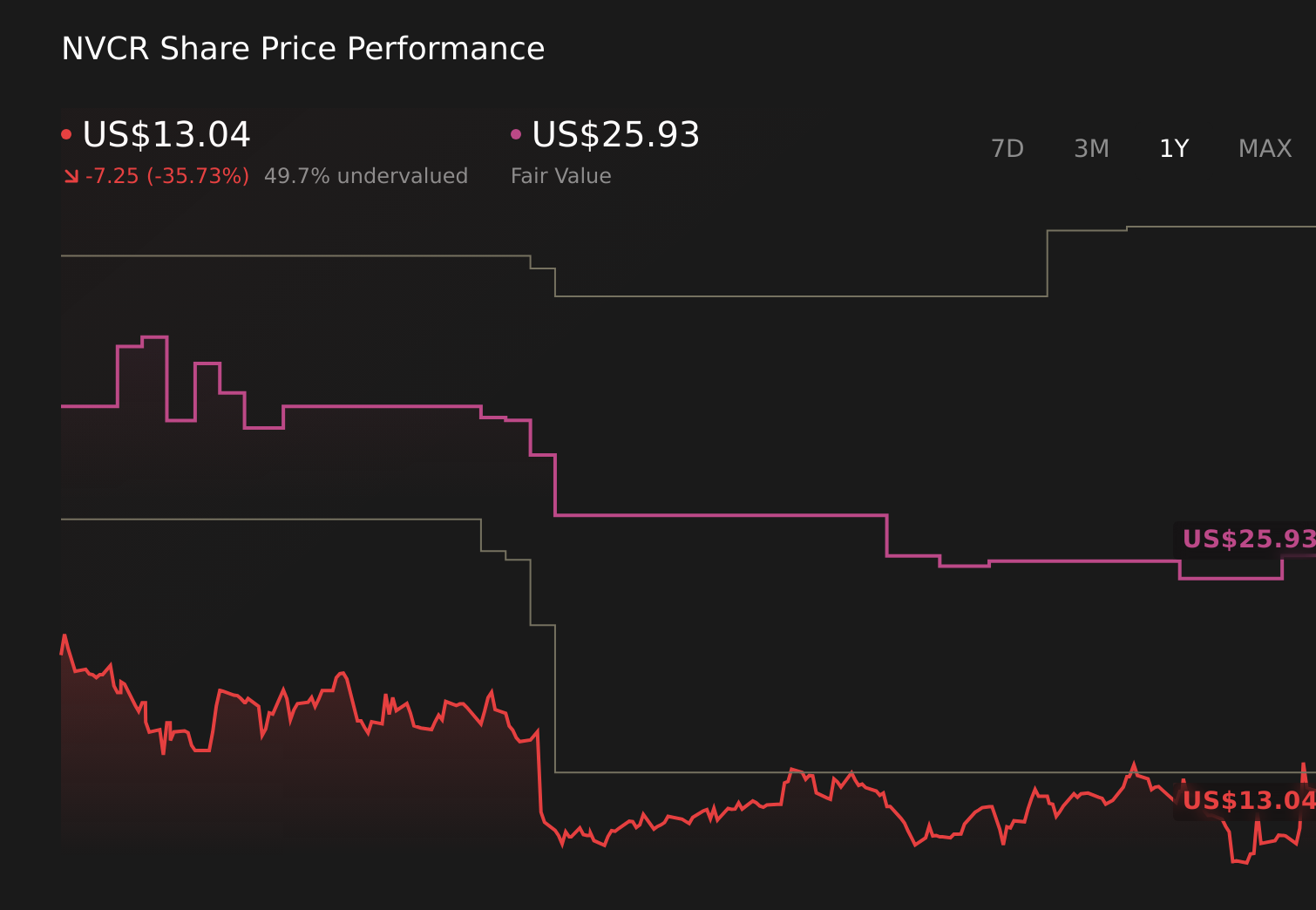

NovoCure's narrative projects $863.5 million revenue and $107.8 million earnings by 2028.

Uncover how NovoCure's forecasts yield a $25.93 fair value, a 123% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenue could reach about US$930.1 million with positive earnings by 2028, yet even that outlook accepted real risks around reimbursement and slower adoption that PANOVA-4 might not fully resolve.

Explore 4 other fair value estimates on NovoCure - why the stock might be worth just $25.93!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your NovoCure research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free NovoCure research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate NovoCure's overall financial health at a glance.

No Opportunity In NovoCure?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Find 55 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 29 elite penny stocks that balance risk and reward.

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.