Does Reaffirmed 2026 Revenue Guidance And Cash Runway To 2028 Change The Bull Case For Iovance (IOVA)?

Iovance Biotherapeutics Inc IOVA | 0.00 |

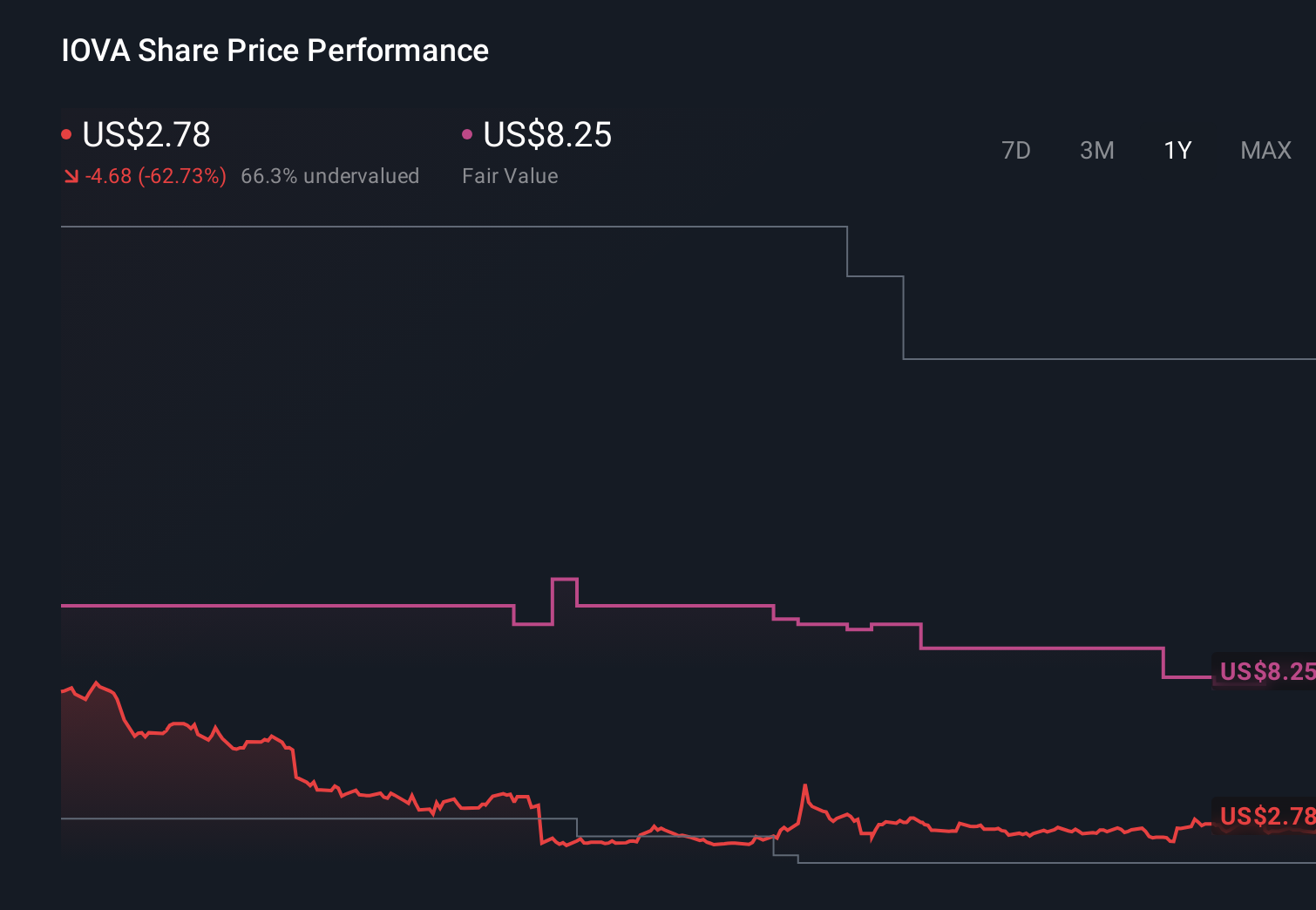

- Iovance Biotherapeutics recently updated its corporate presentation, reaffirming 2026 revenue guidance of US$350 million to US$370 million and highlighting a cash runway into 2028 alongside growing commercial adoption of Amtagvi in advanced melanoma.

- The company also underscored its expanding treatment footprint with more than 1,500 patients treated and over 90 authorized centers, while advancing clinical programs across lung, endometrial, and other solid tumors.

- We will now examine how reaffirmed revenue guidance and a cash runway into 2028 may influence Iovance’s existing investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Iovance Biotherapeutics Investment Narrative Recap

To own Iovance, you need to believe tumor infiltrating lymphocyte therapies can support a durable, scalable business anchored by Amtagvi in advanced melanoma. The reaffirmed 2026 revenue guidance and cash runway into 2028 support that story but do not meaningfully change the near term focus on commercial execution for Amtagvi or the key risk around dependence on a single high priced product in a politically sensitive pricing climate.

Among recent updates, the conditional approval of Amtagvi by Australia’s TGA is particularly relevant. It points to incremental international diversification at a time when Iovance is emphasizing a cash runway into 2028 and a growing treatment network. While this does not remove the underlying risks around pricing pressure or international regulatory uncertainty, it adds context to how additional markets could interact with the company’s current revenue and margin catalysts.

Yet, against this backdrop of reaffirmed guidance and extended cash runway, investors should also keep in mind the risk that pricing scrutiny on a US$562,000 therapy could...

Iovance Biotherapeutics' narrative projects $744.8 million revenue and $35.6 million earnings by 2028. This requires 45.6% yearly revenue growth and a $425.5 million earnings increase from -$389.9 million today.

Uncover how Iovance Biotherapeutics' forecasts yield a $8.35 fair value, a 94% upside to its current price.

Exploring Other Perspectives

Compared with the consensus view, the lowest analysts were assuming around 31 percent annual revenue growth to about US$598.4 million by 2029 but still no profitability, reflecting concern that complex commercialization and high costs could outweigh Iovance’s reaffirmed guidance and cash runway into 2028. This more cautious stance highlights how differently you might weigh the same data and why it can be useful to test your own expectations against several perspectives.

Explore 8 other fair value estimates on Iovance Biotherapeutics - why the stock might be worth over 6x more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Iovance Biotherapeutics research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Iovance Biotherapeutics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Iovance Biotherapeutics' overall financial health at a glance.

Searching For A Fresh Perspective?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- We've uncovered the 7 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.