Does Salesforce’s F1 AI Fan Agent Showcase a Durable Agentforce Advantage for CRM?

Salesforce.com, inc. CRM | 187.18 | +0.50% |

- In early March 2026, Salesforce and Formula 1 launched an Agentforce-powered fan companion agent on F1.com to provide F1’s 827 million fans with 24/7, AI-driven explanations of the complex 2026 regulations and personalized insights based on trusted F1 data sources.

- This launch showcases Salesforce’s Agentforce 360 platform as a real-world example of AI agents augmenting human support at global scale, highlighting how digital labor can deepen engagement while freeing staff to focus on higher-value tasks.

- We’ll now examine how this expanded use of Agentforce to power F1’s global fan companion agent could reshape Salesforce’s long-term investment narrative.

Outshine the giants: these 22 early-stage AI stocks could fund your retirement.

Salesforce Investment Narrative Recap

To own Salesforce, you need to believe its pivot to AI agents and data-driven automation can offset concerns about slower organic growth and potential SaaS commoditization. The F1 fan companion launch reinforces Agentforce as a real, at-scale AI platform, but it does not materially change the near term catalyst, which is whether AI bookings and Data Cloud adoption can keep growing fast enough to ease worries about guidance and competition from AI-native tools.

Alongside the F1 news, Salesforce’s new US$50,000 million share repurchase program is highly relevant, as it amplifies the impact of any eventual re-acceleration in growth and AI adoption on per share metrics. For shareholders, this capital return sits directly against the key risk that AI agents and low-code rivals compress pricing and margins faster than Agentforce and Data Cloud can expand contracts, making execution on AI monetization even more central to the story.

Yet investors should also weigh how quickly new AI competitors could pressure Salesforce’s pricing power before Agentforce fully scales...

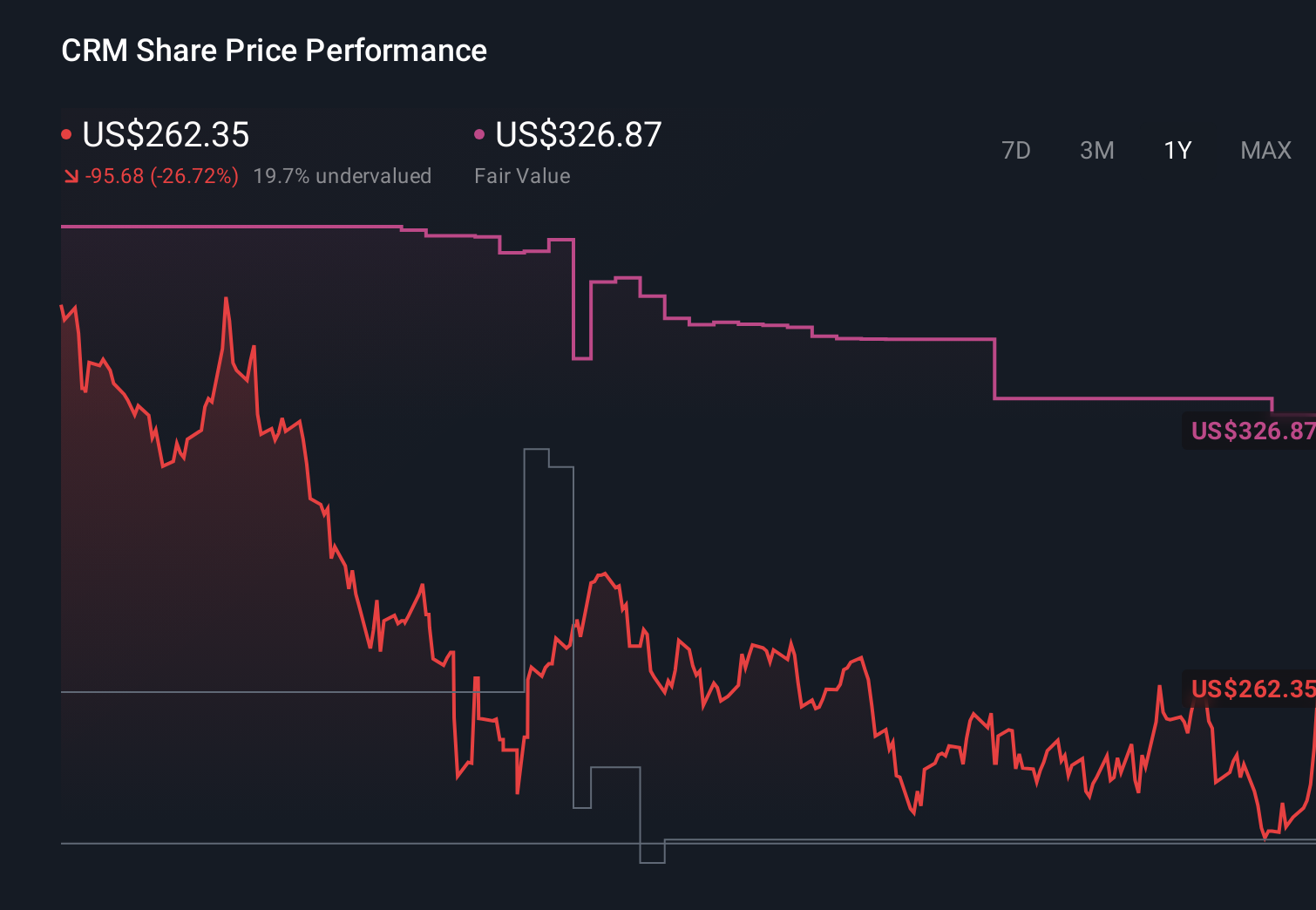

Salesforce's narrative projects $51.9 billion revenue and $10.3 billion earnings by 2028. This requires 9.6% yearly revenue growth and a $3.6 billion earnings increase from $6.7 billion today.

Uncover how Salesforce's forecasts yield a $317.21 fair value, a 64% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were assuming Salesforce revenue would grow only about 7.4% annually to around US$48.9 billion by 2028, which is a much more cautious view than the baseline and could shift further as deployments like the F1 agent test whether concerns about rising AI competition and thinner pricing power are justified.

Explore 41 other fair value estimates on Salesforce - why the stock might be worth as much as 81% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Salesforce research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Salesforce research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Salesforce's overall financial health at a glance.

Curious About Other Options?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 29 best rare earth metal stocks of the very few that mine this essential strategic resource.

- AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with 30 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.