Does Sonos' (SONO) Profit Jump and Buyback Hint at a New Capital Allocation Play?

SONOS INC SONO | 13.86 | +1.46% |

- In early February 2026, Sonos, Inc. reported first-quarter results showing sales of US$545.66 million, slightly lower than a year earlier, while net income rose to US$93.8 million and diluted earnings per share from continuing operations increased to US$0.75.

- Over the same period, Sonos also completed a previously announced share repurchase program totaling 3,010,242 shares for US$45.36 million, underscoring management’s focus on returning capital to shareholders alongside improving profitability.

- We’ll now explore how this stronger quarterly profitability, despite softer sales, may influence Sonos’s existing investment narrative and future expectations.

Find 54 companies with promising cash flow potential yet trading below their fair value.

Sonos Investment Narrative Recap

To own Sonos, you need to believe its premium audio ecosystem and software-led platform can compound value even through product lulls and a soft home-electronics cycle. The latest quarter showed higher profitability on slightly lower sales and a completed buyback, but this does not materially change the near term focus on margin resilience as the key catalyst, or the risk that slower hardware innovation and category weakness could weigh on revenue.

The freshly completed repurchase of 3,010,242 shares for US$45.36 million stands out against this backdrop. It ties directly into the existing catalyst around a leaner cost base and stronger earnings power, because per-share metrics benefit when profits improve while the share count shrinks. That said, with tariffs still pressuring costs and the next major hardware cycle some distance away, the buyback sits alongside, rather than replaces, the core operational questions investors are watching.

Yet against this improving margin story, investors still need to consider the risk that higher tariffs in Vietnam and Malaysia could eventually force price hikes that...

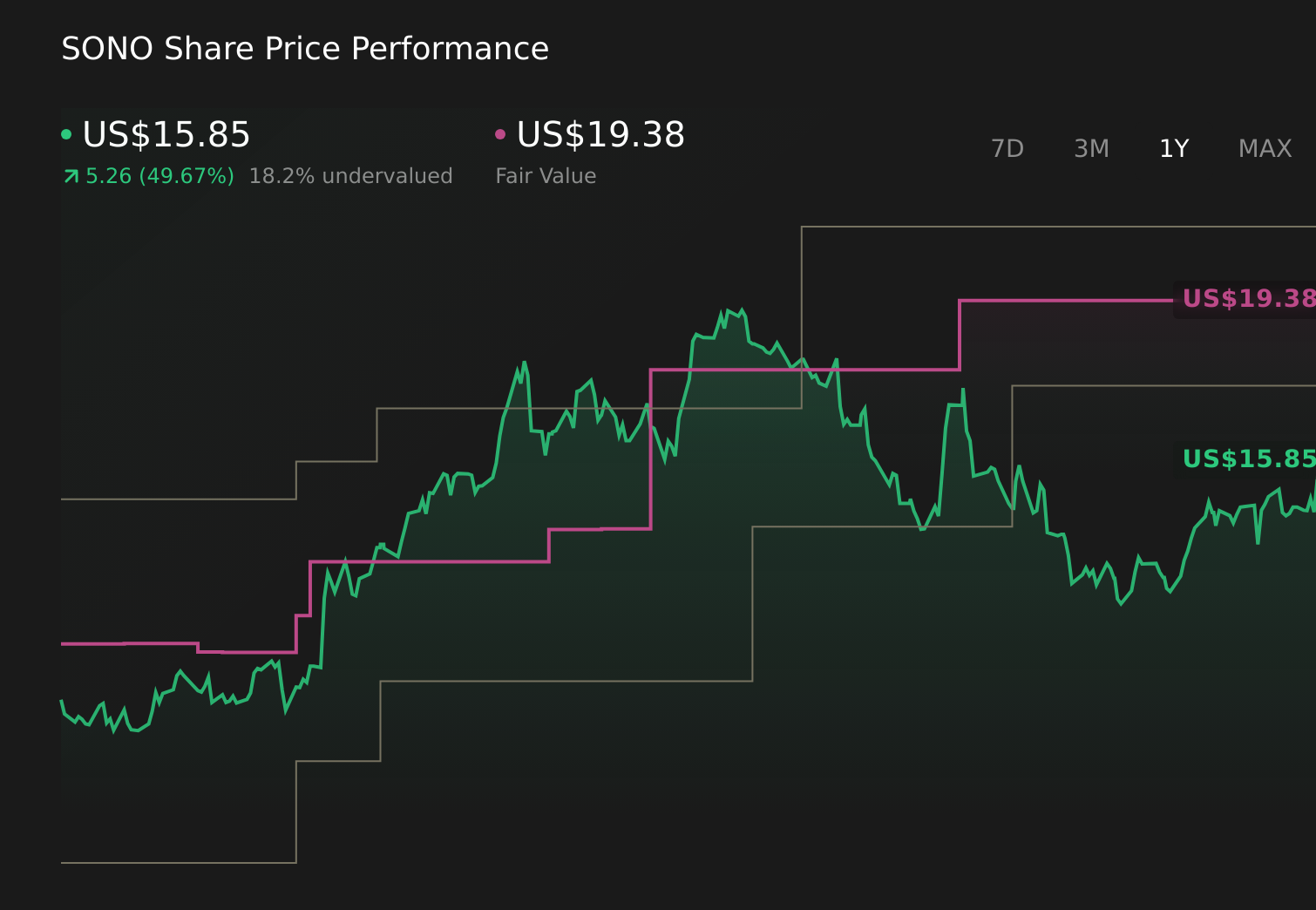

Sonos’ narrative projects $1.6 billion revenue and $120.2 million earnings by 2028.

Uncover how Sonos' forecasts yield a $19.38 fair value, a 24% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming Sonos could lift revenue to about US$1.7 billion and return to modest profitability, but this strong EPS beat and tariff exposure might push those views either further apart or closer together, depending on how you weigh short term cost pressures against long term platform and AI upside.

Explore 4 other fair value estimates on Sonos - why the stock might be worth 26% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Sonos research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Sonos research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Sonos' overall financial health at a glance.

Want Some Alternatives?

Our top stock finds are flying under the radar-for now. Get in early:

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Invest in the nuclear renaissance through our list of 85 elite nuclear energy infrastructure plays powering the global AI revolution.

- Uncover the next big thing with 29 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.