Does Southern Copper’s (SCCO) Insider Sale Reframe How Investors Weigh Peru–Mexico Risk Against Copper Prices?

Southern Copper Corporation SCCO | 0.00 |

- In recent weeks, Southern Copper has attracted attention as higher copper prices tied to stronger factory activity and green energy demand coincided with a small open‑market sale of 100 shares by director Luis Miguel Palomino Bonilla at US$200.00 each, leaving him with 1,707 shares.

- Investor focus now centers on how rising copper prices intersect with ongoing political, social, and regulatory risks in Peru and Mexico that could affect Southern Copper’s operations and project timelines.

- We’ll now explore how stronger copper prices, amid persistent Peru and Mexico risk, reshape Southern Copper’s existing investment narrative and risk-reward profile.

Explore 30 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Southern Copper Investment Narrative Recap

To own Southern Copper today, you need to believe that elevated copper prices tied to factory activity and green energy can outweigh mounting cost, community, and regulatory pressures in Peru and Mexico. The recent 100 share sale by director Luis Miguel Palomino Bonilla looks immaterial to this bigger picture, while the key short term swing factor remains copper pricing versus regional political and permitting risk that could slow or disrupt projects.

The most relevant recent development is the share price strength alongside higher copper prices, which has already drawn mixed reactions from analysts. UBS and Scotiabank both raised their price targets while keeping negative ratings, highlighting how some see current copper driven optimism as running ahead of operational and country risk. This tension between price momentum and lingering Peru and Mexico uncertainty is central to how the near term risk reward now looks for Southern Copper.

Yet behind the strong copper story, investors also need to be aware of ongoing community and permitting pressures around projects like Tia Maria and Los Chancas...

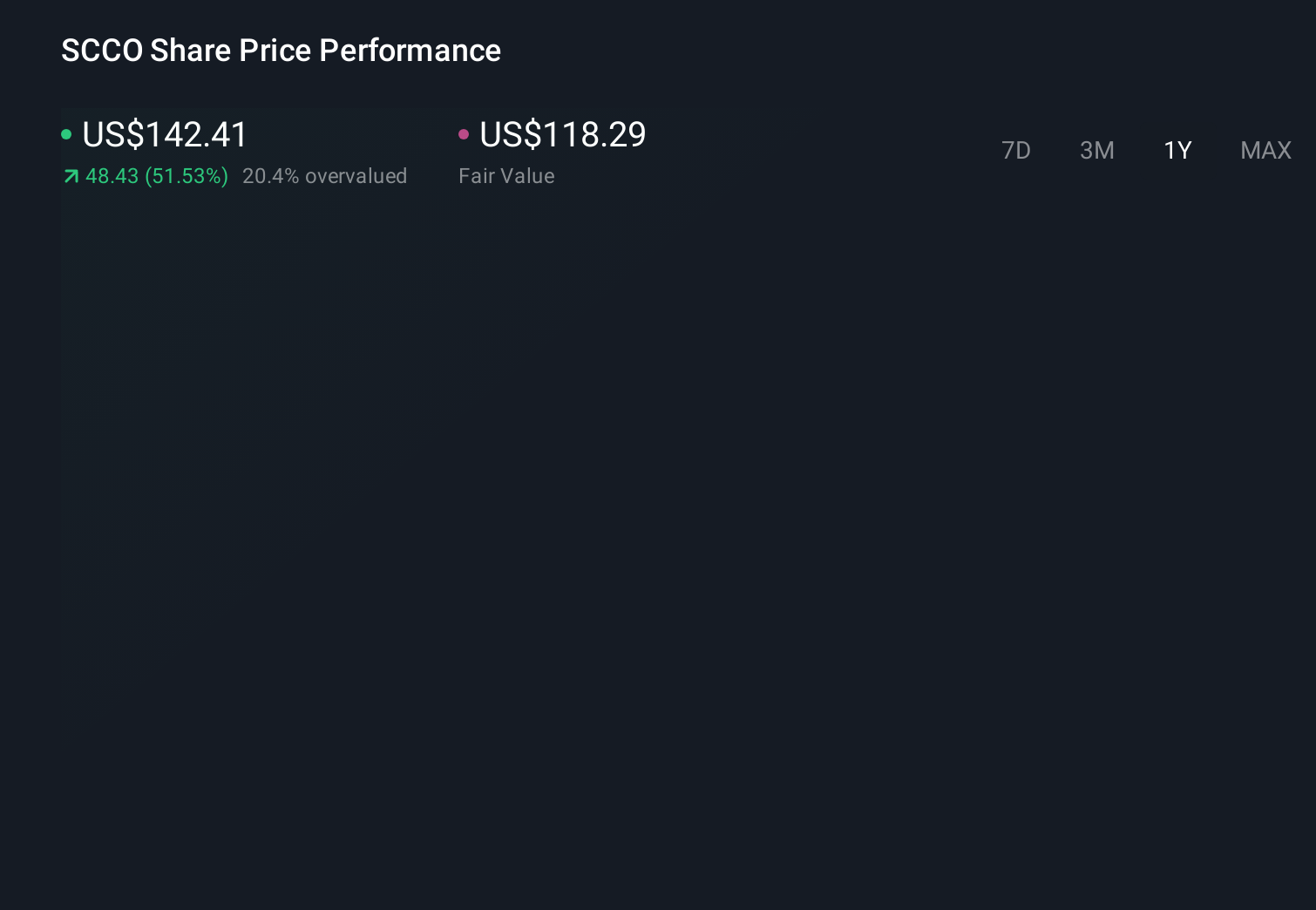

Southern Copper's narrative projects $16.8 billion revenue and $6.2 billion earnings by 2029. This requires 4.8% yearly revenue growth and a $1.2 billion earnings increase from $5.0 billion today.

Uncover how Southern Copper's forecasts yield a $162.54 fair value, a 6% downside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts were already assuming revenue could slip to about US$13.9 billion with only US$4.9 billion in earnings, which shows how differently you and other investors might weigh project delay risks and the latest copper price strength, and why these pre news forecasts may now need a fresh look.

Explore 4 other fair value estimates on Southern Copper - why the stock might be worth 28% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Southern Copper research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Southern Copper research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Southern Copper's overall financial health at a glance.

Want Some Alternatives?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Find 49 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.