Does StoneCo’s Russell Index Additions and Upbeat Forecasts Change The Bull Case For STNE?

StoneCo Ltd. STNE | 0.00 |

- In late June 2026, StoneCo Ltd. (NasdaqGS: STNE) was added to multiple Russell value indexes, including the Russell 2000, 2500, 3000, 3000E and Small Cap Comp Value benchmarks.

- This wave of index inclusions coincides with upbeat analyst expectations ahead of StoneCo’s upcoming earnings release, including a favorable Zacks Rank of #2 (Buy) and projected earnings and revenue growth.

- We’ll now examine how this combination of index additions and upbeat analyst sentiment may influence StoneCo’s existing investment narrative.

Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

StoneCo Investment Narrative Recap

To own StoneCo, you need to believe in the long-term shift to digital payments and financial services for small businesses in Brazil, and in StoneCo’s ability to deepen relationships across banking, credit and payments. The recent wave of Russell value index inclusions may support near term liquidity and visibility, but it does not materially change the key near term catalyst, which remains execution around earnings quality, or the main risk from slower TPV growth and credit quality pressures.

Among recent developments, the extraordinary cash dividend of US$2.53 per share announced in April 2026 stands out as most relevant when thinking about today’s index additions. Together with ongoing buybacks, it underlines management’s willingness to return capital even as analysts forecast earnings and revenue trends that are more muted ahead. How sustainable that capital return posture is will likely depend on how StoneCo balances funding growth, absorbing credit costs and preserving balance sheet strength.

Yet beneath the improving headline story, investors should be aware that rising credit provisions and slower TPV growth could still...

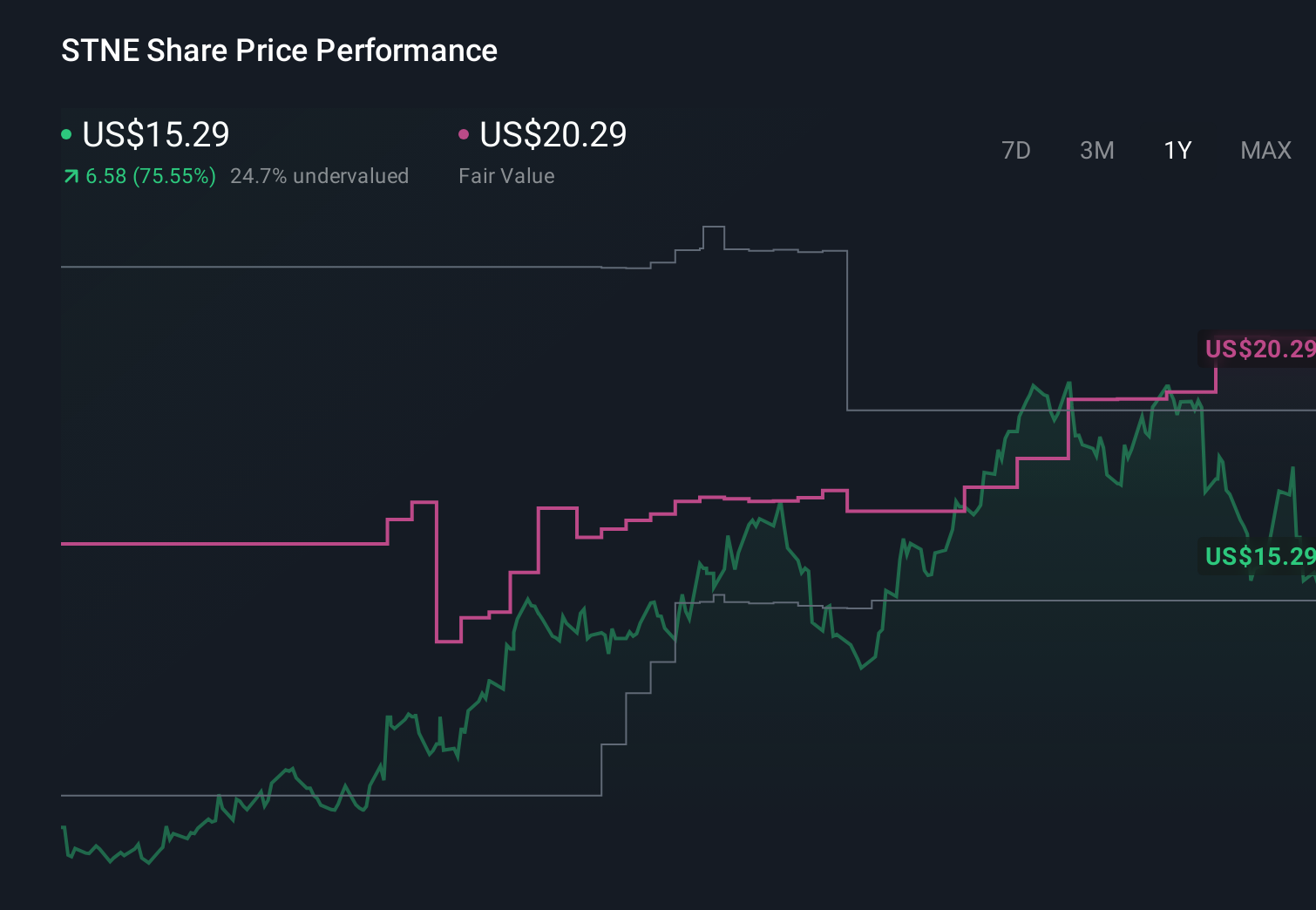

StoneCo's narrative projects R$17.4 billion revenue and R$5.0 billion earnings by 2028. This requires 8.2% yearly revenue growth and about a R$6.3 billion earnings increase from R$-1.3 billion today.

Uncover how StoneCo's forecasts yield a $20.29 fair value, a 82% upside to its current price.

Exploring Other Perspectives

By contrast, the most bearish analysts were assuming revenue growth of only 2.3% a year and earnings falling toward about R$2.0 billion, which shows how differently you and other investors might view risks like regulatory pressure and digital disruption in light of StoneCo’s new index status and why it is worth weighing several viewpoints before deciding what this latest news might mean.

Explore 5 other fair value estimates on StoneCo - why the stock might be worth over 4x more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your StoneCo research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free StoneCo research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate StoneCo's overall financial health at a glance.

No Opportunity In StoneCo?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Find 43 companies with promising cash flow potential yet trading below their fair value.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 31 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.