Does Strong Q1 Results And A New Buyback Program Change The Bull Case For ZTO (ZTO)?

ZTO Express (Cayman) Inc. Sponsored ADR Class A ZTO | 0.00 |

- Earlier in 2026, ZTO Express (Cayman) reported first-quarter results showing higher earnings per share and revenue year over year, reaffirmed its 2026 parcel volume guidance, and authorized a two-year US$1.50 billion share repurchase program.

- This combination of improving fundamentals and a sizeable buyback plan highlights management’s confidence in the business while potentially altering the company’s capital allocation profile.

- We’ll now examine how the new US$1.50 billion share repurchase program may reshape ZTO Express (Cayman)’s broader investment narrative.

AI is about to change healthcare. These 38 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

ZTO Express (Cayman) Investment Narrative Recap

To own ZTO Express (Cayman), you need to believe that parcel volumes and cost efficiency can offset pricing pressure and capital spending needs. The reaffirmed 2026 parcel growth guidance keeps volume as the key near term catalyst, while intense competition and shifting parcel mix remain the biggest risks to margins. The new US$1.50 billion buyback and stronger first quarter figures support the story but do not fundamentally change those core drivers.

The new two year US$1.50 billion repurchase program is the headline development here, especially alongside ongoing automation and technology investment. With ZTO reporting higher year over year revenue and earnings per share, this capital return plan sits squarely in the debate over whether cost savings and parcel growth can offset industry pricing pressure and heavy capex, and how much of that shows up in per share results.

Yet, even with parcel growth guidance intact, investors should still be aware of how persistent pricing pressure and a shift toward smaller, lower value parcels could...

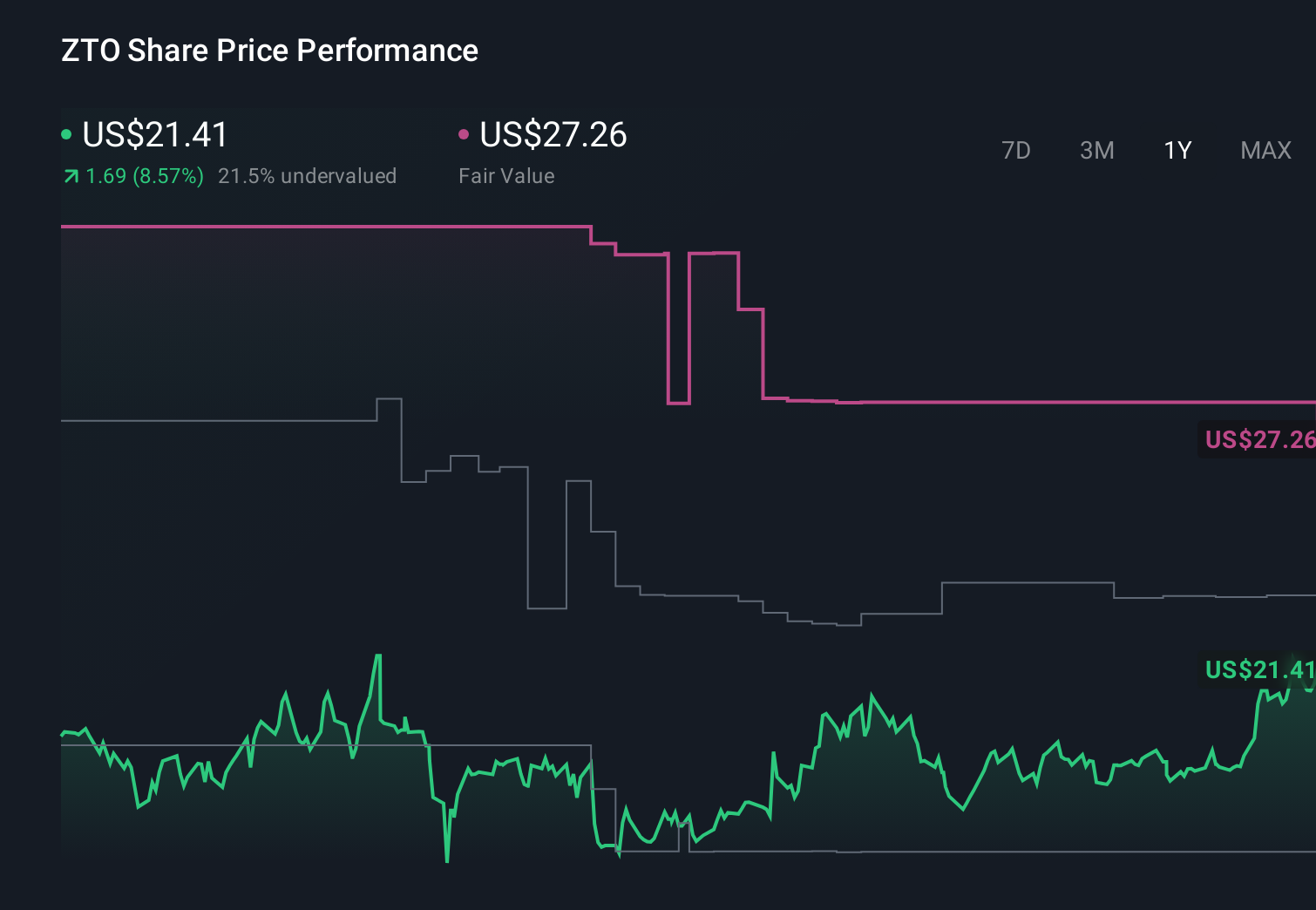

ZTO Express (Cayman)'s narrative projects CN¥60.4 billion revenue and CN¥11.6 billion earnings by 2028.

Uncover how ZTO Express (Cayman)'s forecasts yield a $23.87 fair value, a 7% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts already expected revenue near CN¥77.1 billion and earnings around CN¥15.4 billion by 2029, so this buyback news could either reinforce their view or prompt revisions, especially if rising labor costs and higher performance based wages start to bite into the margin story they are counting on.

Explore 6 other fair value estimates on ZTO Express (Cayman) - why the stock might be worth 6% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your ZTO Express (Cayman) research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free ZTO Express (Cayman) research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ZTO Express (Cayman)'s overall financial health at a glance.

Curious About Other Options?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.