Does Strong Q1 Results And Reaffirmed EPS Guidance Shift The Bull Case For Otter Tail (OTTR)?

Otter Tail Corporation OTTR | 0.00 |

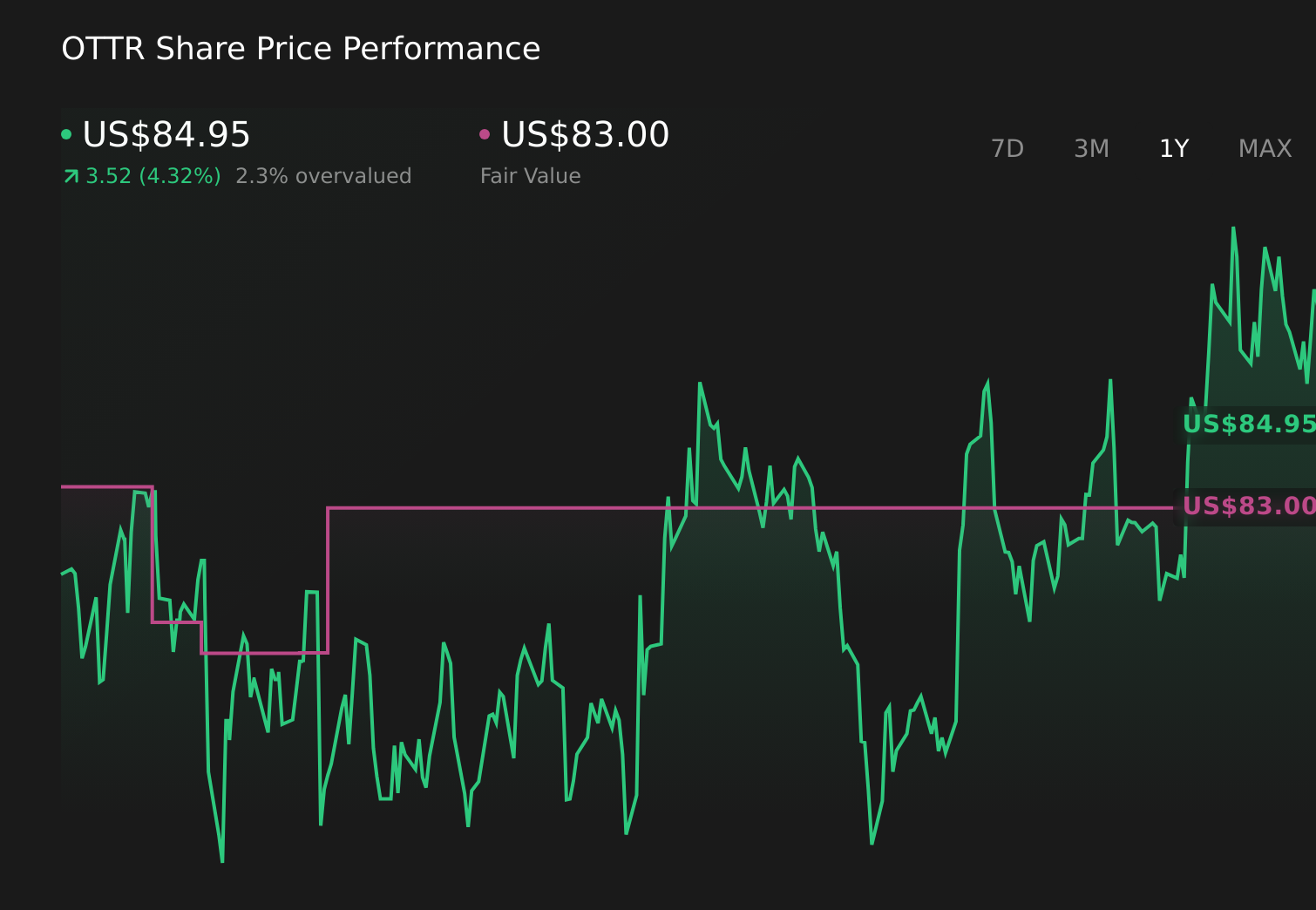

- In early May 2026, Otter Tail Corporation reported higher first-quarter revenue of US$347.03 million and net income of US$72.61 million year over year, reaffirmed its 2026 diluted EPS guidance of US$5.22 to US$5.62, and declared a quarterly dividend of US$0.5775 per share payable in June.

- The combination of earnings growth, maintained full‑year guidance, and a continued dividend payout highlights Otter Tail’s emphasis on earnings visibility and returning cash to shareholders.

- We’ll now assess how reaffirmed 2026 earnings guidance shapes Otter Tail’s existing investment narrative around regulated growth and execution risks.

The latest GPUs need a type of rare earth metal called Dysprosium and there are only 31 companies in the world exploring or producing it. Find the list for free.

Otter Tail Investment Narrative Recap

To own Otter Tail, you need to be comfortable with a regulated utility that is funding a large capital program while relying on a mix of utility, manufacturing, and plastics earnings. The latest quarter’s higher revenue and net income, along with reaffirmed 2026 EPS guidance, supports near term earnings visibility, but does not materially change the key short term debate around execution risk on the US$1.4 billion capital plan and exposure to higher funding costs.

The reaffirmed 2026 diluted EPS guidance of US$5.22 to US$5.62 is the most relevant piece of news here, because it anchors expectations around how reliably Otter Tail can earn through its rate base investments while managing headwinds such as potential environmental compliance costs and any earnings normalization in non utility segments.

Yet investors should also be aware that tighter monetary conditions could raise Otter Tail’s cost of capital and...

Otter Tail's narrative projects $1.4 billion revenue and $205.5 million earnings by 2029. This requires 2.9% yearly revenue growth and an earnings decrease of $74.9 million from $280.4 million today.

Uncover how Otter Tail's forecasts yield a $90.50 fair value, a 3% upside to its current price.

Exploring Other Perspectives

Three fair value estimates from the Simply Wall St Community span roughly US$65 to US$91 per share, underlining how far apart individual views can be. Against that backdrop, Otter Tail’s reaffirmed 2026 EPS guidance and sizable capital plan keep the focus squarely on how funding costs and regulatory outcomes could influence future profitability, so it is worth comparing several independent viewpoints before forming your own.

Explore 3 other fair value estimates on Otter Tail - why the stock might be worth 26% less than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Otter Tail research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Otter Tail research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Otter Tail's overall financial health at a glance.

Searching For A Fresh Perspective?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Invest in the nuclear renaissance through our list of 87 elite nuclear energy infrastructure plays powering the global AI revolution.

- Find 49 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.