Does Stryker’s Valuation Reflect Its Latest Medical Device Acquisitions and Stock Performance in 2025?

Stryker Corporation SYK | 0.00 |

- If you have ever wondered whether Stryker is a hidden value play or just priced for perfection, you are not alone. Let's cut through the noise together.

- While Stryker's shares are down 6.7% over the last week and slipped 2.2% over the past month, the stock is basically flat for the year and still up an impressive 73.9% over the past three years.

- Recent news has highlighted Stryker’s ongoing developments in the medical device space, including strategic acquisitions and partnerships that could expand its growth pipeline. These headlines may help explain the stock’s latest swings and keep the company on investors’ radar despite short-term volatility.

- Stryker clocks in with a valuation score of 2 out of 6, meaning there is room for debate on whether it is a bargain or not. Let’s break down the numbers with some familiar valuation methods. Make sure you stick around, because there is an even better way to make sense of it all at the end of this article.

Stryker scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Stryker Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and discounting them back to their present value. This approach captures the value of a business by focusing directly on how much real money it can generate for shareholders.

For Stryker, the DCF model uses the 2 Stage Free Cash Flow to Equity method. The company's latest reported Free Cash Flow (FCF) stands at $4.09 billion. According to analyst estimates, Stryker’s FCF is set to grow steadily, reaching $6.37 billion by 2028 and projected by external sources to push past $10 billion by 2035. Estimates beyond 2028 reflect Simply Wall St’s extrapolated growth trends and are not direct analyst forecasts.

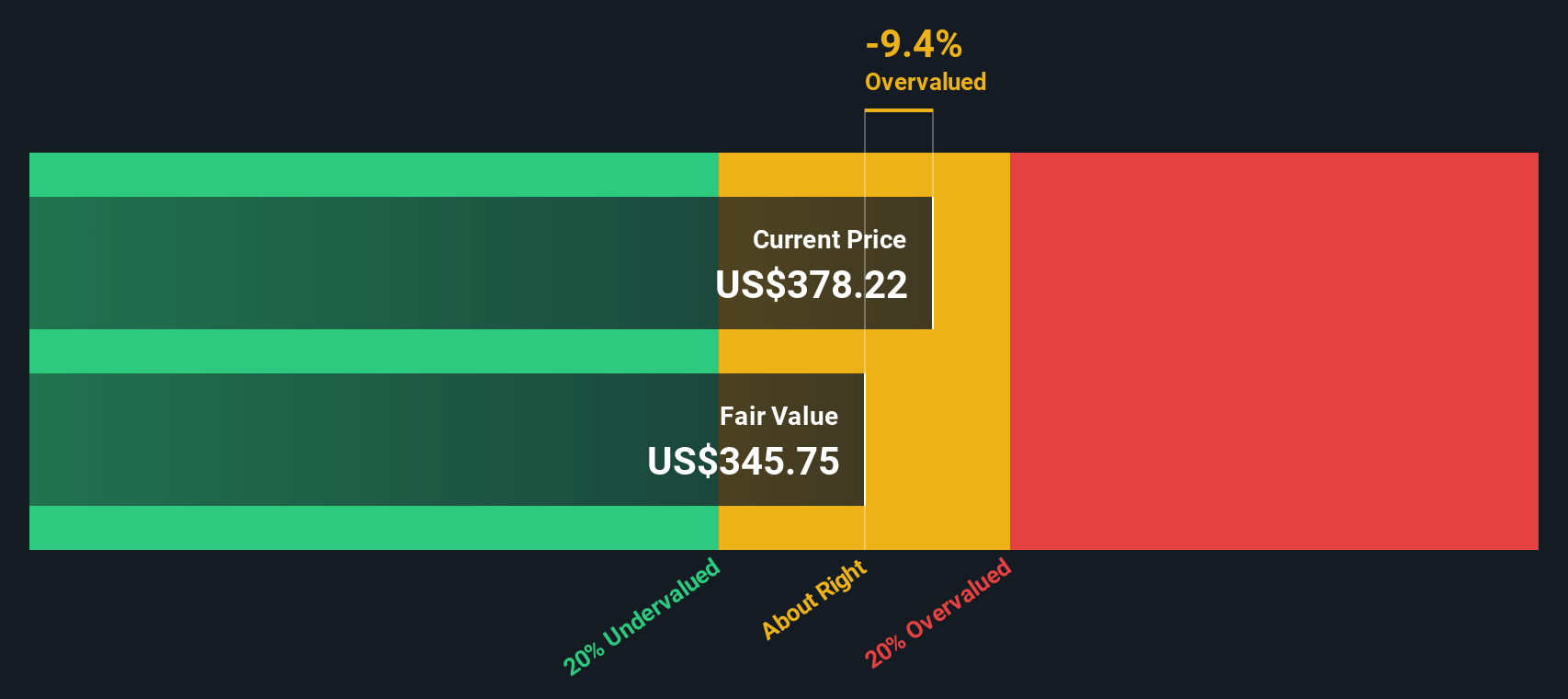

Based on these projections and discounting all future flows back to present value, the DCF model assigns Stryker an intrinsic value of $421.29 per share. Compared to its current trading price, this suggests the stock is about 15.4% undervalued.

The bottom line is that, by DCF standards, Stryker may be trading at an attractive entry point for long-term investors seeking value in the medical device sector.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Stryker is undervalued by 15.4%. Track this in your watchlist or portfolio, or discover 834 more undervalued stocks based on cash flows.

Approach 2: Stryker Price vs Earnings (PE Ratio)

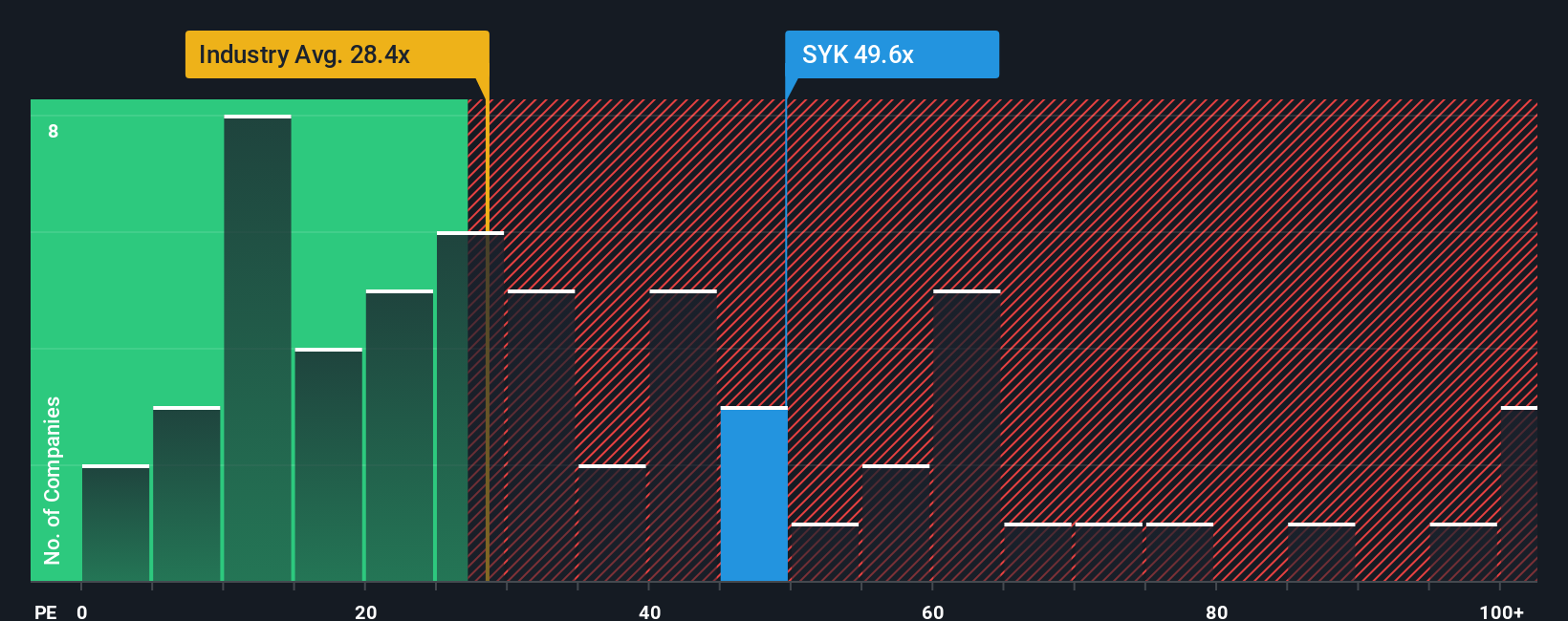

For profitable companies like Stryker, the Price-to-Earnings (PE) ratio is a widely used valuation metric. The PE ratio tells investors how much they are paying for each dollar of a company's earnings, which is especially useful when those earnings are stable and growing as they are for Stryker.

It is important to note that higher growth expectations usually justify a higher PE ratio, as investors are willing to pay more for companies expected to grow faster. Conversely, higher perceived risks or slower growth would push a fair PE lower, signaling a discount to reflect those concerns.

Stryker currently trades at a PE ratio of 46.28x. This sits well above the Medical Equipment industry average of 27.74x and also higher than the average of its listed peers at 40.71x. However, Simply Wall St calculates a proprietary Fair Ratio for Stryker at 34.00x, which considers the company's own earnings growth potential, risks, profit margin, industry factors, and its sizeable market cap.

Unlike simple peer or industry comparisons, the Fair Ratio aims to answer what a reasonable valuation looks like for Stryker specifically. This method accounts for nuances in the company’s growth rate, risk, and profit outlook that generic benchmarks might miss.

With Stryker’s current PE of 46.28x notably higher than the Fair Ratio of 34.00x, the stock appears to be trading at a premium, suggesting a potential overvaluation based on earnings.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1410 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Stryker Narrative

Earlier, we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is a simple yet powerful tool that enables you to connect the story you believe about a company—such as its future growth, risks, and opportunities—to your financial assumptions like future revenue, margins, and fair value. Narratives help turn your personal perspective on Stryker into a customized forecast, so your belief about the company’s direction is grounded in numbers, not just headlines or hype.

Available to millions in the Simply Wall St Community, Narratives make it easy to see how your fair value estimate stacks up against others, and compare your conclusions with the current market price. As news and quarterly results come in, Narratives are automatically updated, so your investment case always reflects the latest facts.

For example, with Stryker, one investor’s Narrative might price the shares at $465, supporting expectations for strong innovation and global expansion, while another, more cautious view sees fair value down at $316, emphasizing regulatory and cost pressures. Narratives empower you to decide for yourself when the numbers change and stories shift.

Do you think there's more to the story for Stryker? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.