Does the Recent 11.2% Drop Make Pfizer a Value Play in 2025?

Pfizer Inc. PFE | 28.32 | -0.81% |

- Curious if Pfizer's current stock price is a bargain or just a mirage? You're not alone; plenty of investors are wondering whether now is the right time to dive in or stay on the sidelines.

- Despite robust debate around its potential, Pfizer’s share price dipped 0.8% over the past week, finished last month down 11.2%, and has lost 7.1% over the last year. This signals a shift in how the market perceives its growth prospects and risks.

- Recent headlines spotlight Pfizer’s strategic moves in drug development and acquisitions, alongside ongoing industry innovation. These have kept the company at the center of both challenges and big-picture opportunities, adding extra color to the recent price swings.

- On our value checklist, Pfizer scores a solid 5 out of 6, indicating it passes most key affordability screens based on our usual metrics. Next, we will break down how each valuation method stacks up, and we have another perspective you will want to see before you make your decision.

Approach 1: Pfizer Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its expected future cash flows and discounting them back to today's dollars. For Pfizer, this involves analyzing future Free Cash Flow (FCF), which is essentially the cash the company can return to shareholders after maintaining and growing its business.

Currently, Pfizer generates $9.95 billion in Free Cash Flow. According to analyst projections, annual FCF is expected to steadily grow over the next decade, reaching approximately $18.02 billion by 2035. While analysts provide estimates for the next five years, additional years are extrapolated by Simply Wall St for a more comprehensive view.

The DCF model calculates Pfizer's intrinsic value at $67.65 per share. This represents a 64.1% discount compared to where the stock currently trades. These numbers suggest Pfizer is trading well below its calculated fair value using conservative cash flow estimates.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Pfizer is undervalued by 64.1%. Track this in your watchlist or portfolio, or discover 840 more undervalued stocks based on cash flows.

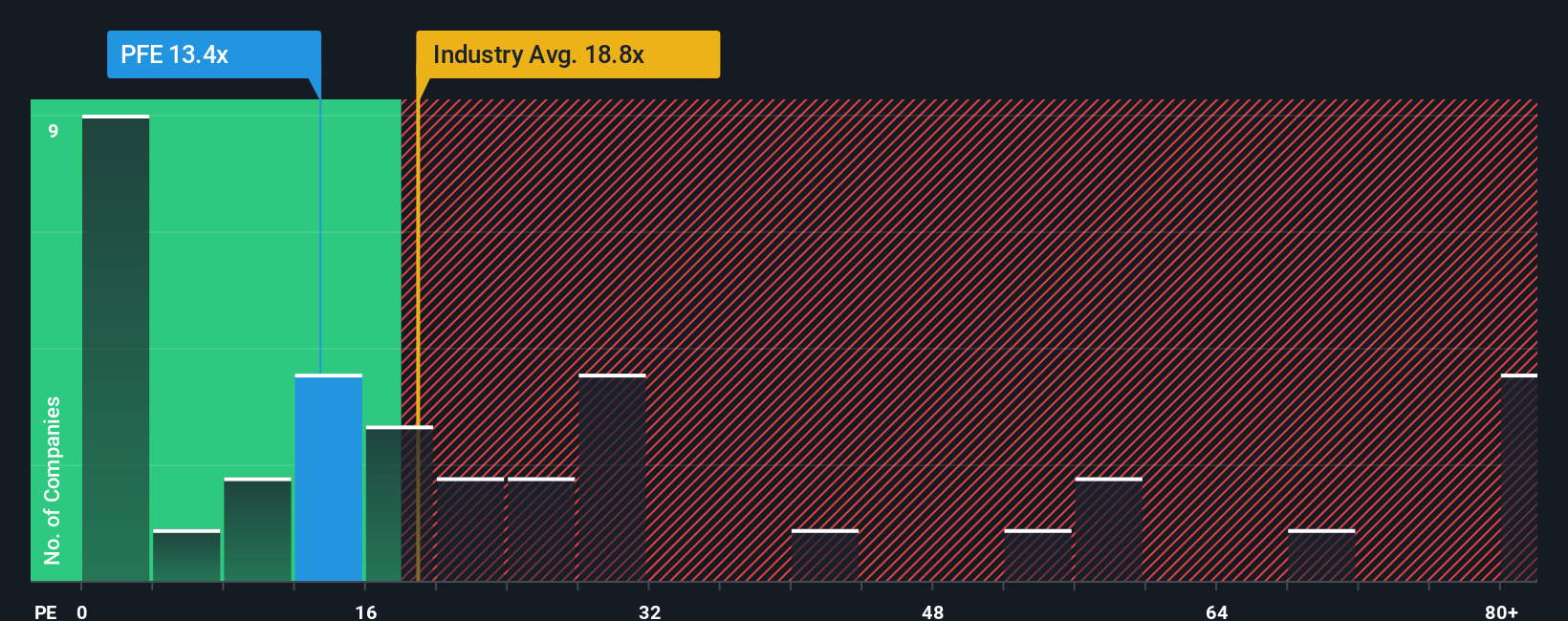

Approach 2: Pfizer Price vs Earnings

The Price-to-Earnings (PE) ratio is a widely used valuation metric for profitable companies because it relates a company's share price to its earnings per share. For investors, the PE ratio offers a quick measure of how much they are paying for each dollar of company earnings, and can help identify if a stock is undervalued or overvalued relative to other options.

What qualifies as a "normal" or "fair" PE ratio can vary quite a bit depending on growth expectations and risk. Fast-growing companies typically command higher ratios while mature or riskier companies see lower numbers. Industry trends and market sentiment can also shift the bar for what is seen as reasonable.

Currently, Pfizer trades at a PE ratio of 14.1x. This is lower than the Pharmaceuticals industry average of 17.7x and also below the peer group’s average of 16.3x. At first glance, this could suggest Pfizer is trading at a discount compared to its sector and competitors.

Simply Wall St's proprietary “Fair Ratio” is a more nuanced benchmark, reflecting factors like Pfizer’s profit margins, long-term growth forecast, size, and the risk profile of its business. Rather than just comparing to industry or peers, the Fair Ratio sets a more customized bar to judge whether the current valuation aligns with the company’s true prospects.

For Pfizer, the Fair Ratio is 24.2x, substantially higher than its current PE. This indicates the market is pricing the stock well below what its fundamentals might justify, signaling potential undervaluation.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1410 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Pfizer Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is a story investors create about a company’s future, connecting their perspective on where Pfizer is headed with the numbers: their forecast for future revenue, earnings, and fair value.

Instead of only relying on static ratios or consensus estimates, Narratives let you tie the company’s story, such as breakthrough drugs launching, operational risks, or industry shifts, to a personalized financial outlook. This approach links your perspective to a specific price target and prediction for the years ahead.

Narratives are easy to use and fully accessible right on the Simply Wall St Community page, where millions of investors share their own forecasts and stories, helping you see not only analyst estimates but the logic behind them.

This tool helps you decide when to buy or sell by letting you compare each Narrative’s Fair Value to the current stock price. It highlights who believes in a turnaround, ongoing risks, or outperformance, and explains why. Additionally, Narratives update dynamically as news and earnings are released, keeping your view as current as possible.

For Pfizer, some investors see enormous upside with targets above $35 if oncology growth and cost efficiencies pan out, while others warn of downside close to $24 amid regulatory and patent headwinds.

For Pfizer however, we'll make it really easy for you with previews of two leading Pfizer Narratives: 🐂 Pfizer Bull CaseFair Value: $28.86

Undervalued by: 15.74%

Revenue Growth Rate: -2.2%

- Pfizer is positioned for long-term growth through expansion in innovative therapies, especially oncology and biologics, with further support from strategic acquisitions and business development.

- Focused efforts in digitalization and emerging markets are driving operational efficiencies, improved margins, and uncovering new revenue sources, particularly in developing regions.

- The main risks include regulatory changes, patent expirations, and growing competition, but consensus analysts expect earnings growth and a price target above the current share price if these headwinds are managed well.

Fair Value: $24.00

Overvalued by: 1.25%

Revenue Growth Rate: -4.2%

- Increasing global pressure to reduce drug prices, regulatory reforms, and impending patent expirations are expected to undercut Pfizer's revenue growth and constrain profit margins.

- Heavier reliance on new R&D assets to fill gaps left by aging, at-risk drugs poses a significant risk to Pfizer’s future revenue and earnings stability.

- While innovation and acquisitions may provide some support, bearish analysts believe these opportunities will not fully offset the projected declines and consider the current price higher than warranted by their fair value estimates.

Do you think there's more to the story for Pfizer? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.