Does the Recent 69.8% Hertz Stock Surge Signal a Real Opportunity for 2025?

HERTZ GLOBAL HOLDINGS, INC. HTZ | 5.11 | -1.35% |

- Curious if Hertz Global Holdings is a bargain or a bounce trap? You're not alone, and we're diving deep to see just how much value might be hiding in the numbers.

- The stock has rocketed up 32.4% year to date and gained an impressive 69.8% over the past year, even though it has dipped 4.4% in the last week and 21.0% over the past month.

- Momentum has largely been sparked by renewed attention on the used car market and shifting consumer travel habits, both of which put Hertz in the spotlight. News of industry-wide vehicle shortages and changing car rental dynamics have played a major role in recent price swings.

- The company earns a strong 5 out of 6 valuation score, suggesting a lot to like for value-minded investors. We'll break down how that number is calculated and, more importantly, dig into what it might miss. There may be an even better way to see the full picture, which we'll get to before we wrap up.

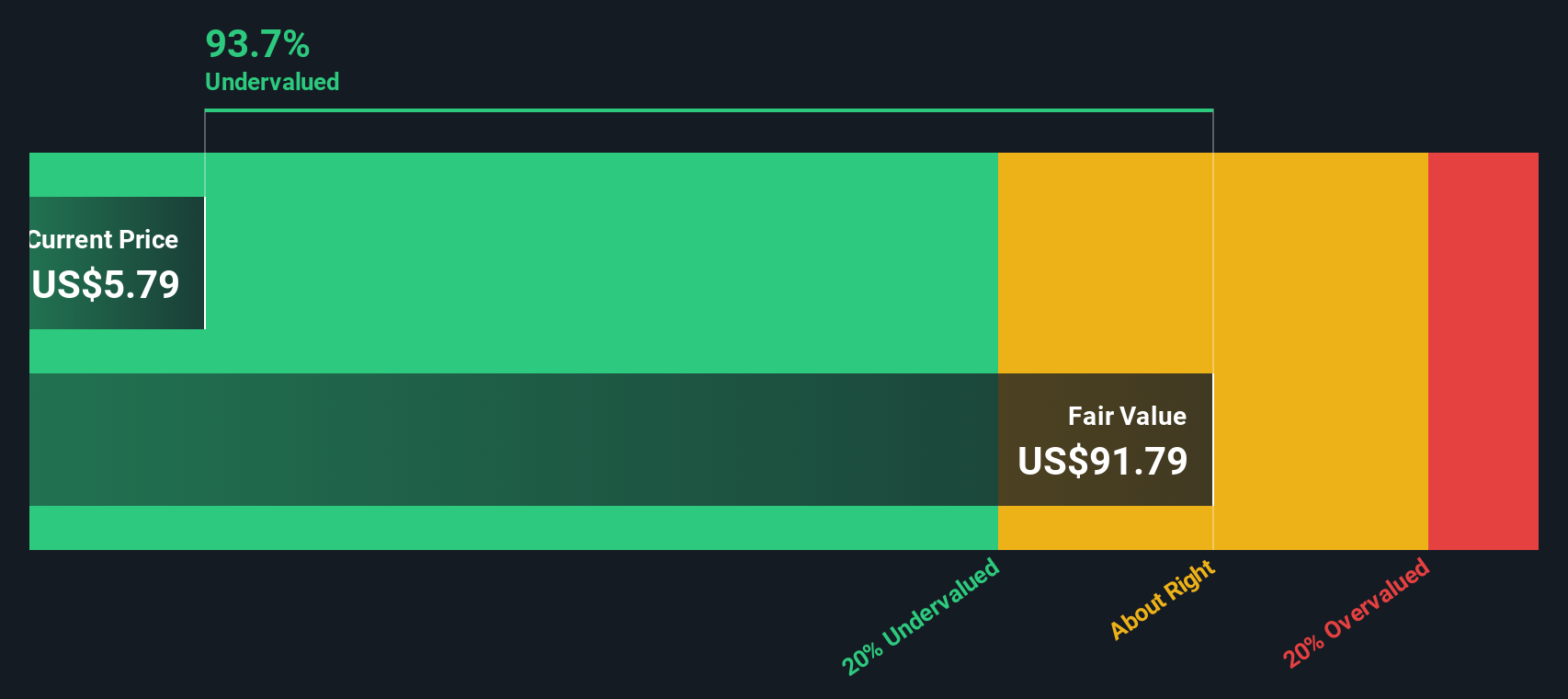

Approach 1: Hertz Global Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates the true value of a company by projecting its expected future cash flows and then discounting those figures back to today's value. This approach aims to answer the question: What is Hertz Global Holdings worth if we consider all the cash it could realistically generate for shareholders over time?

For Hertz Global Holdings, the DCF analysis starts with the company's latest twelve months Free Cash Flow, which stands at negative $1.24 billion, reflecting recent challenges. Looking ahead, analyst estimates suggest a turnaround, with Free Cash Flow projected to reach $595 million by 2026. The model then extrapolates growth even further and expects Free Cash Flow to climb to approximately $3.0 billion by 2035, all measured in US dollars.

This long-term projection is discounted based on the risks and time value of money, resulting in an estimated intrinsic value per share of $63.73. With the DCF model indicating Hertz is trading at a 92.2% discount compared to that value, this suggests the shares are substantially undervalued according to this measure.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Hertz Global Holdings is undervalued by 92.2%. Track this in your watchlist or portfolio, or discover 843 more undervalued stocks based on cash flows.

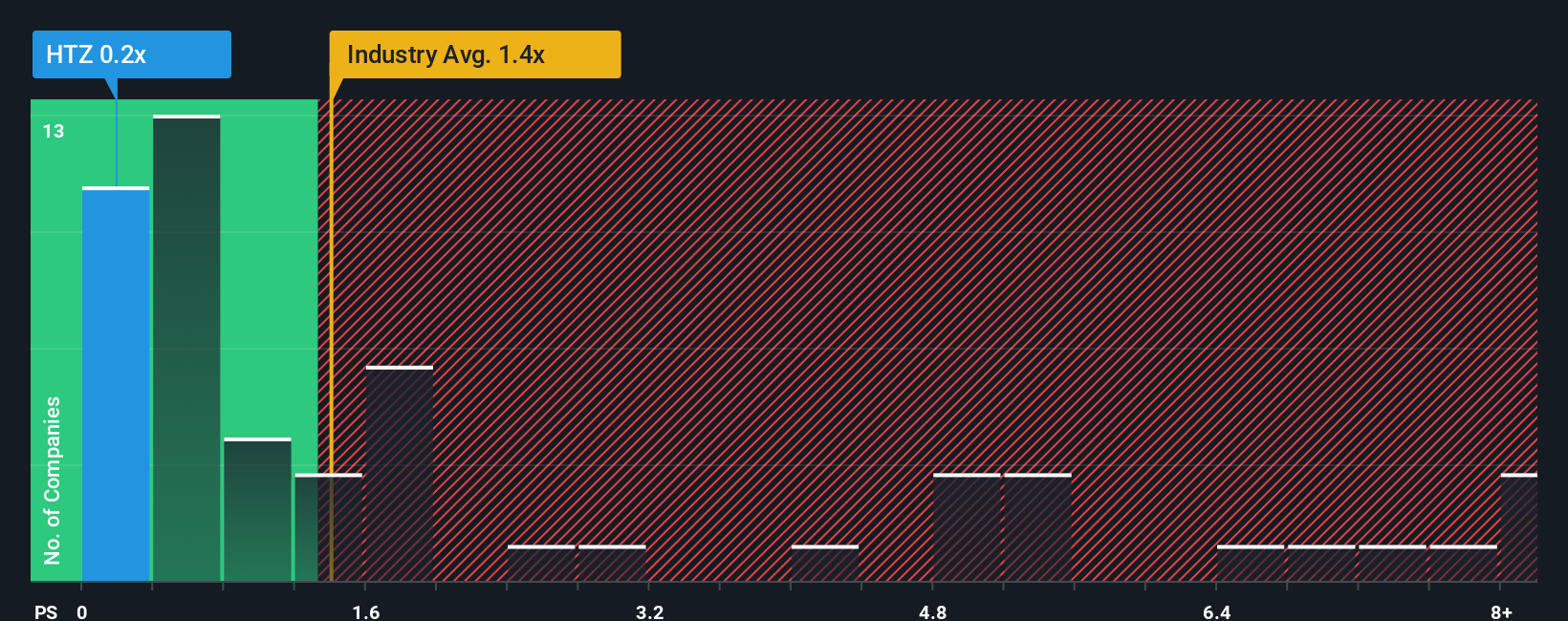

Approach 2: Hertz Global Holdings Price vs Sales

For companies like Hertz Global Holdings, which have experienced swings in profitability and negative earnings in recent periods, the Price-to-Sales (P/S) ratio is often a more reliable valuation tool than metrics like Price-to-Earnings. The P/S ratio focuses on the company’s total revenue, making it useful for assessing value when profits are volatile or temporarily negative because it gives a sense of how much investors are paying for each dollar of sales.

Growth expectations and risk directly impact what constitutes a “normal” or “fair” P/S multiple. Fast-growing, lower-risk companies can justify higher ratios, while slower-growth or more uncertain businesses tend to trade at lower levels. This context is crucial when comparing Hertz’s current P/S to key benchmarks.

As it stands, Hertz trades at a P/S ratio of 0.18x, which is dramatically lower than the Transportation industry average of 1.20x and the peer group’s average of 2.72x. While these numbers signal Hertz’s shares are trading at a significant discount, there is a more nuanced way to assess value: Simply Wall St's proprietary “Fair Ratio.” The Fair Ratio, calculated at 0.41x for Hertz, factors in growth prospects, industry dynamics, profit margins, market capitalization, and risk, giving a tailored expectation of what the P/S should be for this specific business rather than just a broad-brush comparison.

This approach is more insightful than using simple peer or industry benchmarks because it accounts for the big-picture influences that actually drive sustainable value. While Hertz’s P/S of 0.18x is still below its Fair Ratio of 0.41x, the gap is not enormous, suggesting the stock is undervalued by this measure but not to a dramatic degree.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1410 companies where insiders are betting big on explosive growth.

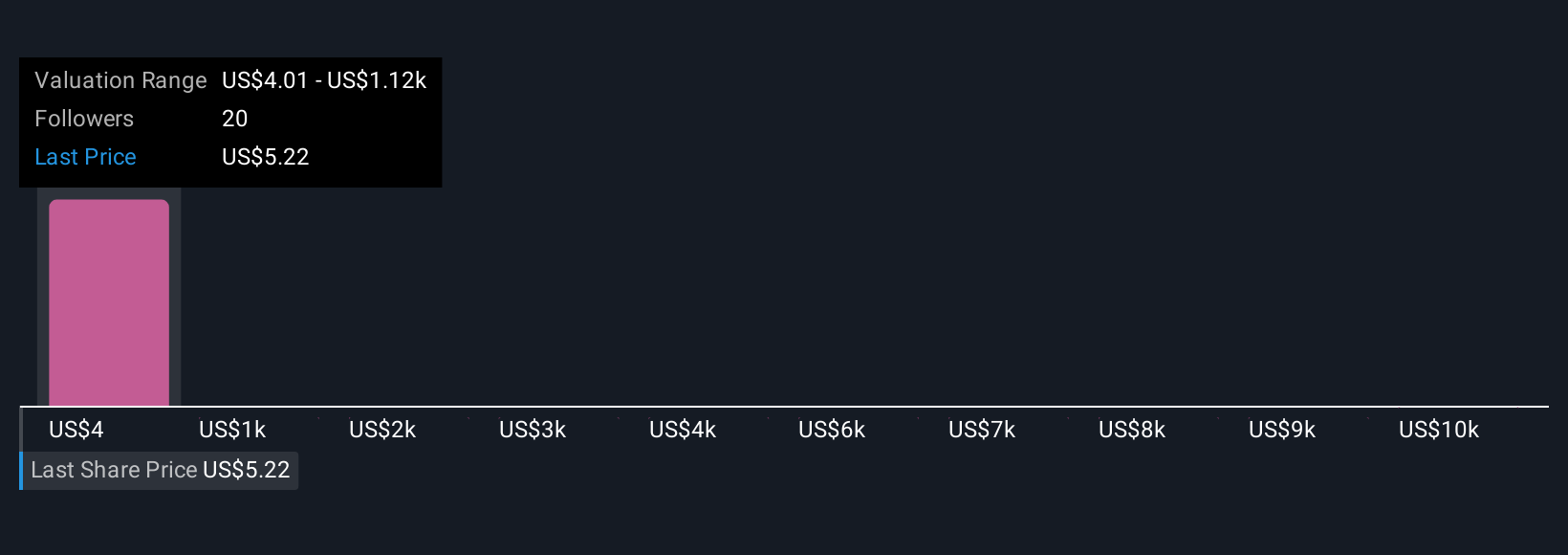

Upgrade Your Decision Making: Choose your Hertz Global Holdings Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is a simple, story-driven explanation of what you believe about a company like Hertz Global Holdings, based on your assumptions about its future growth, margins, and value. This approach turns the numbers into a story with logic you can track and revisit.

With Narratives, you connect the company's outlook and industry shifts to your own financial forecasts, creating a direct bridge from Hertz's evolving story and business trajectory to a tailored fair value estimate. This approach makes investment decisions more personal and meaningful, helping you easily decide whether the current price is high, low, or about right based on what you believe.

Narratives are easy to use and live right within Simply Wall St's Community page, where millions of investors share and compare their views on companies like Hertz. Because Narratives update automatically whenever new facts, news, or earnings arrive, your viewpoint always keeps pace with the real world, with no more out-of-date analyses or missed developments.

For example, on Hertz Global Holdings, some investors see a future upended by robotaxis and shrinking margins and set a fair value as low as $3.00 per share, while others believe digitization and fleet modernization will pay off, supporting a value as high as $6.00 per share.

Do you think there's more to the story for Hertz Global Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.