Does Vulcan Materials’ Pause in Buybacks Reshape Its Capital Allocation Narrative for VMC Investors?

Vulcan Materials Company VMC | 279.88 | -0.09% |

- Vulcan Materials recently announced its second quarter and six-month 2025 results, reporting year-over-year growth in both sales and net income, with sales for the quarter reaching US$2,102.4 million and net income rising to US$320.9 million.

- An interesting aspect is that while the company completed its buyback program, repurchasing more than 11.59 million shares over several years, it did not buy any shares in the most recent quarter.

- We'll examine how Vulcan’s ongoing earnings growth and recent completion of its buyback program impact the company’s investment narrative.

The end of cancer? These 26 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Vulcan Materials Investment Narrative Recap

To be a shareholder in Vulcan Materials, you need to believe that infrastructure and construction demand, boosted by long-term government spending, will outweigh near-term market headwinds and regional volatility risks. The latest news, showing steady earnings growth and the completion of its share buyback program, does not materially shift the company's most important near-term catalyst (infrastructure spending momentum) or biggest risk (persistent residential construction weakness); these factors still drive the core investment thesis.

The earnings announcement on July 31 is most relevant here, as it highlights another quarter of rising sales and net income, reinforcing optimism around sustained operational execution. Continued progress in sales, along with incremental profit growth despite a challenging backdrop for residential markets, directly aligns with infrastructure-led volume and margin catalysts that underpin investor interest in Vulcan.

Yet, in contrast, investors should not overlook the risk associated with Vulcan’s reliance on timely public infrastructure funding and the potential impact of...

Vulcan Materials is projected to reach $9.6 billion in revenue and $1.5 billion in earnings by 2028. This outlook requires 8.1% annual revenue growth and an increase in earnings of approximately $541.9 million from the current $958.1 million.

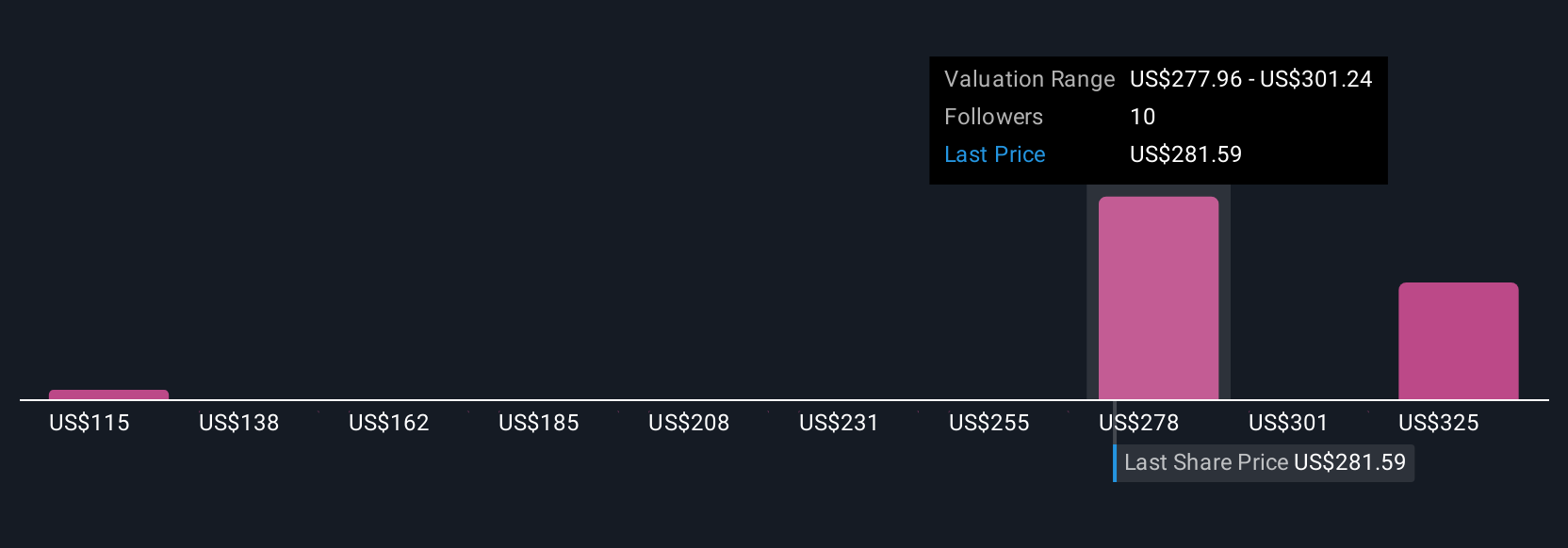

Uncover how Vulcan Materials' forecasts yield a $300.00 fair value, a 5% upside to its current price.

Exploring Other Perspectives

Three Simply Wall St Community members have published fair value estimates for Vulcan Materials, ranging from US$115 to US$344 per share. These differing views stand alongside concerns about ongoing challenges in residential construction volumes, inviting you to compare a variety of perspectives on the company’s outlook.

Explore 3 other fair value estimates on Vulcan Materials - why the stock might be worth less than half the current price!

Build Your Own Vulcan Materials Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Vulcan Materials research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Vulcan Materials research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Vulcan Materials' overall financial health at a glance.

No Opportunity In Vulcan Materials?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Rare earth metals are the new gold rush. Find out which 26 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.