Does Vulcan’s Tech-Driven Efficiency Pivot and New Profit Targets Reshape The Bull Case For VMC?

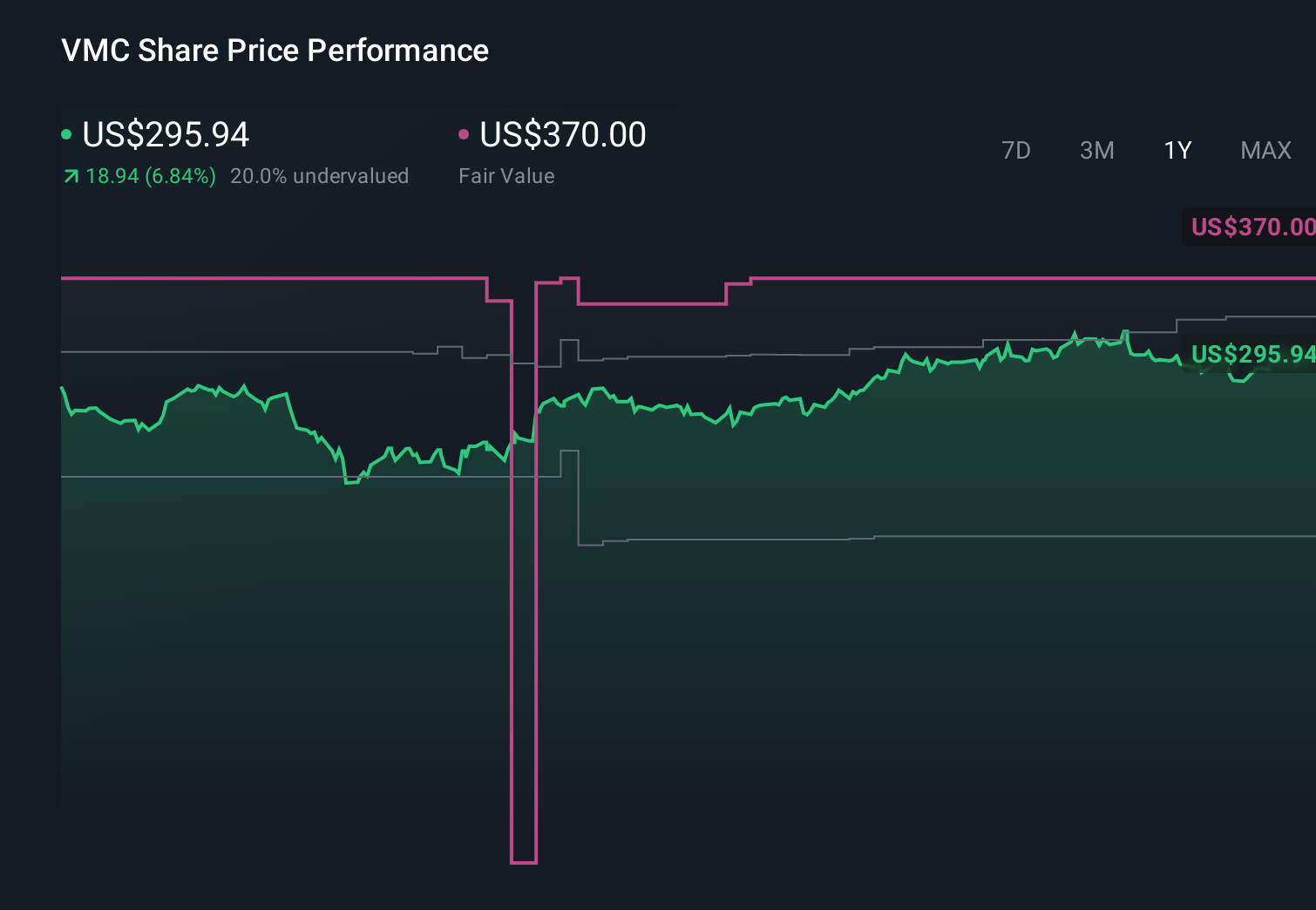

Vulcan Materials Company VMC | 291.71 | +2.08% |

- Vulcan Materials recently held its 2026 Investor Day, outlining new cash gross profit per ton and earnings targets, alongside plans to use innovation and technology to enhance profitability following earlier earnings pressure.

- Management also shared longer-term ambitions, including an EBITDA goal of between US$4.50 billion and US$5.00 billion and a focus on operational efficiencies, environmental initiatives, and resource conservation in its core aggregates business.

- Now we’ll examine how Vulcan’s heightened focus on technology-driven efficiency and new profitability targets could influence its investment narrative.

Uncover the next big thing with 32 elite penny stocks that balance risk and reward.

Vulcan Materials Investment Narrative Recap

To own Vulcan Materials, you generally have to believe in a long runway for US infrastructure and non-residential construction, and in Vulcan’s ability to convert that demand into consistent cash generation despite volume and margin swings. The recent Q4 miss and margin pressure highlight that the most immediate catalyst is how quickly profitability stabilizes, while the key near term risk remains further earnings pressure if competitive and pricing headwinds persist. The Investor Day targets do not materially change those core issues.

The most relevant recent announcement is Vulcan’s 2026 Investor Day, where management introduced new cash gross profit per ton and earnings targets and framed an EBITDA ambition of US$4.50 billion to US$5.00 billion. For investors focused on catalysts, this tightens the link between technology driven efficiency efforts and future margin improvement, but it also raises the bar: any continued cost pressure, project delays, or weather related disruptions could now be judged against a very explicit profitability roadmap.

Yet against these ambitions, investors should also be aware of the risk that extreme weather and regional concentration could...

Vulcan Materials' narrative projects $9.6 billion revenue and $1.5 billion earnings by 2028. This requires 8.1% yearly revenue growth and a $541.9 million earnings increase from $958.1 million today.

Uncover how Vulcan Materials' forecasts yield a $327.57 fair value, a 23% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already more cautious, despite assuming Vulcan might reach about US$9.5 billion of revenue and US$1.5 billion of earnings, and the latest margin disappointment could give that more pessimistic view extra traction, reminding you that reasonable people can look at the same numbers and still reach very different conclusions about what comes next.

Explore 5 other fair value estimates on Vulcan Materials - why the stock might be worth less than half the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Vulcan Materials research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Vulcan Materials research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Vulcan Materials' overall financial health at a glance.

Searching For A Fresh Perspective?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Find 48 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 14 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.