Does Walker & Dunlop’s ESOP Shelf And Arno Financing Reframe The Bull Case For WD?

Walker & Dunlop, Inc. WD | 0.00 |

- In May 2026, Walker & Dunlop filed a US$53.81 million shelf registration for 1,000,000 common shares tied to an ESOP offering, while also arranging US$128.5 million in acquisition financing for The Arno, a luxury multifamily community in Houston’s River Oaks area.

- These actions, set against commentary on Denver’s real estate perception issues and a multi‑year decline in profitability metrics, highlight how Walker & Dunlop is balancing employee ownership, capital markets access, and multifamily financing activity amid operational headwinds.

- We’ll now examine how the highlighted profitability pressures and capital management challenges may influence Walker & Dunlop’s existing investment narrative.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

Walker & Dunlop Investment Narrative Recap

To own Walker & Dunlop, you need to believe that its multifamily and commercial real estate platform can convert transaction activity into sustainably higher earnings despite recent margin compression and weaker returns. The new US$53.81 million ESOP shelf registration and The Arno financing do not appear to materially change the near term picture, where the key catalyst remains a recovery in profitable deal flow and the main risk is continued pressure on net interest income and returns on equity.

The ESOP related shelf registration stands out here, because it sits alongside a history of dividend growth and a new US$75 million buyback authorization. Together, these moves frame an active capital management story at a time when earnings, tangible book value per share, and profitability metrics have been under strain, which may sharpen investor focus on whether future transaction volumes translate into stronger per share outcomes.

Yet behind the appeal of multifamily deal headlines, investors should be aware of how prolonged weakness in net interest income and shrinking profitability metrics could...

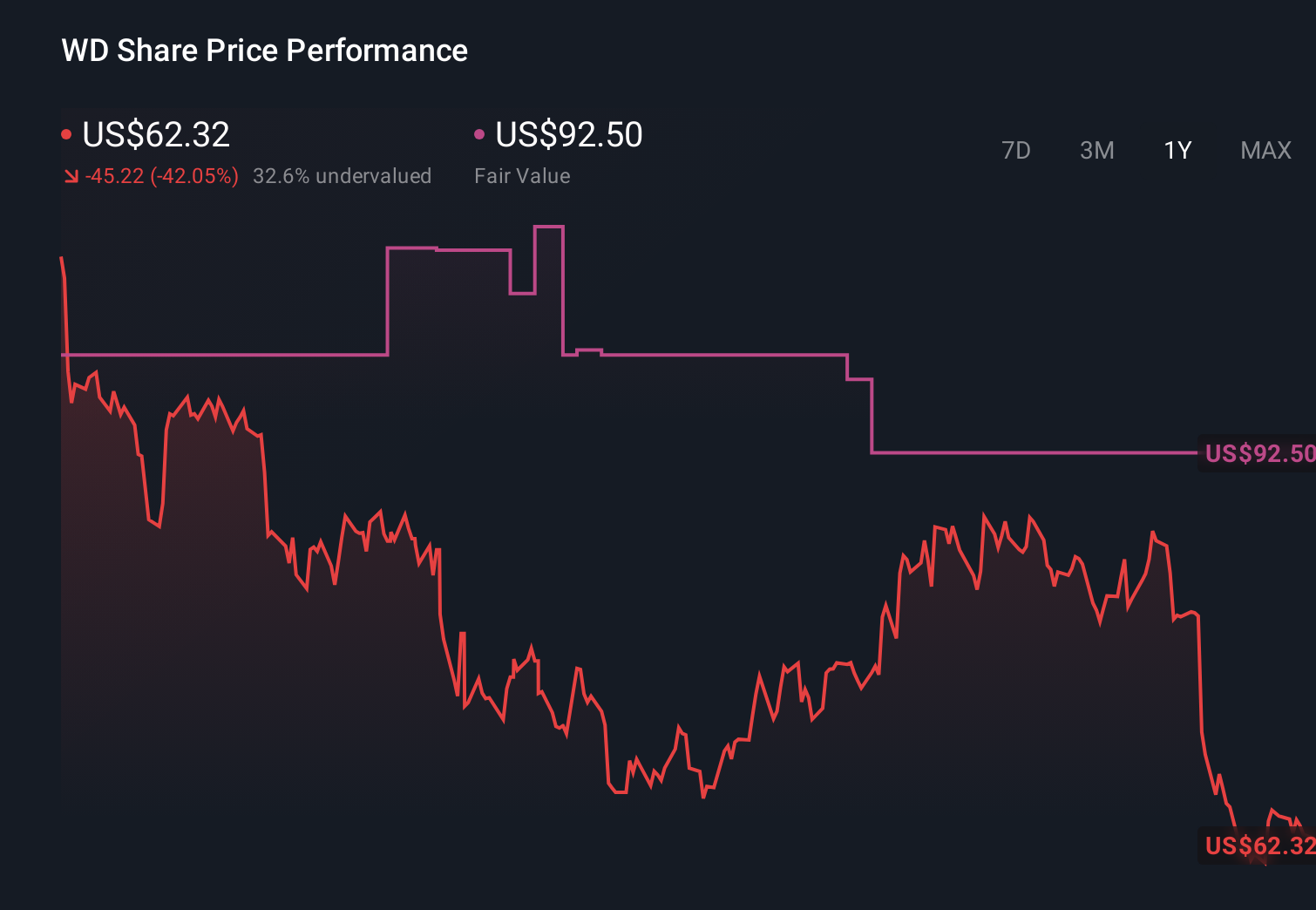

Walker & Dunlop's narrative projects $1.7 billion revenue and $214.2 million earnings by 2029. This requires 12.2% yearly revenue growth and about a $145.9 million earnings increase from $68.3 million today.

Uncover how Walker & Dunlop's forecasts yield a $68.67 fair value, a 36% upside to its current price.

Exploring Other Perspectives

Three Simply Wall St Community fair value estimates span roughly US$31 to US$69, showing how far apart individual views on Walker & Dunlop can be. When you set that against recent multi year declines in net interest income and earnings per share, it underlines why many readers may want to compare several independent viewpoints on the company’s prospects.

Explore 3 other fair value estimates on Walker & Dunlop - why the stock might be worth 38% less than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Walker & Dunlop research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Walker & Dunlop research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Walker & Dunlop's overall financial health at a glance.

Seeking Other Investments?

Our top stock finds are flying under the radar-for now. Get in early:

- Find 49 companies with promising cash flow potential yet trading below their fair value.

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.