Does Williams’ Dividend Hike And Transco Focus Reshape The Bull Case For WMB?

Williams Companies, Inc. WMB | 0.00 |

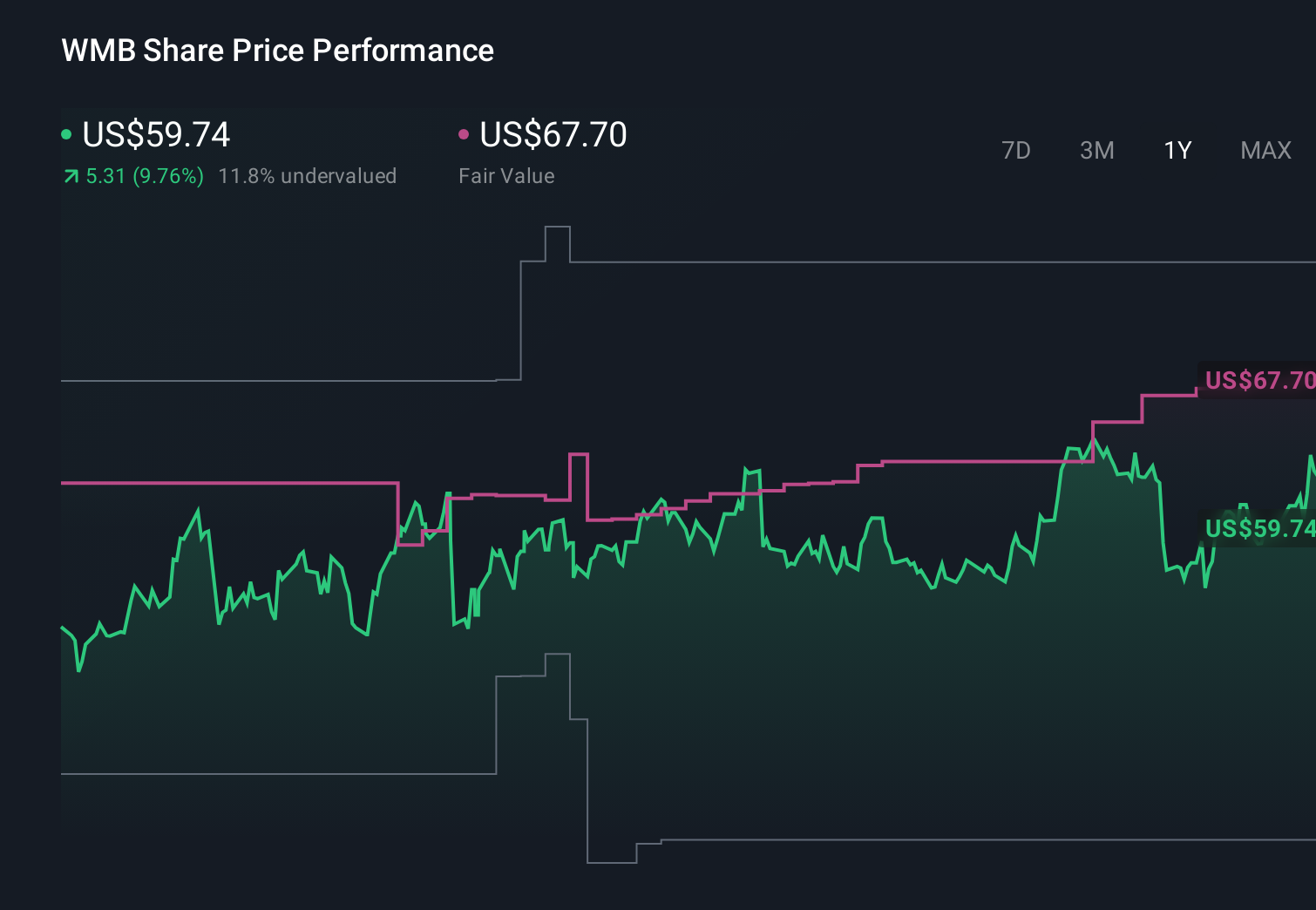

- In late April 2026, Williams Companies approved a higher regular quarterly dividend of US$0.525 per share, or US$2.10 annualized, payable on June 29, 2026, to shareholders of record on June 12, 2026, marking a 5% increase from its 2025 payout.

- This dividend hike, combined with recent analyst upgrades praising Williams’ Transcontinental Gas Pipeline and power infrastructure exposure, underscores how income returns and core gas transmission assets sit at the center of the company’s current equity story.

- Next, we’ll examine how the higher dividend and confidence in Transco’s role in power infrastructure reshape Williams Companies’ investment narrative.

AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Williams Companies Investment Narrative Recap

To own Williams Companies today, you need to believe that its core gas transmission network, especially Transco, will remain central to power and LNG flows while supporting a reliable income profile. The latest 5% dividend increase reinforces the income angle but does not materially change the key near term tug of war between growth in power and LNG driven gas demand and the risk that permitting setbacks or policy shifts slow expansion on critical corridors.

The most relevant recent development alongside the dividend hike is Goldman Sachs’ upgrade focusing on Transco and gas fired power infrastructure. That call leans into the same near term catalyst higher utilization and expansion of Williams’ existing corridors to serve LNG exports, utilities and data centers while existing risks around long cycle projects, permitting and capital intensity remain firmly in place for shareholders to watch.

But even with rising payouts and upbeat analyst views, investors should still be aware of how faster decarbonization or tougher permitting could...

Williams Companies' narrative projects $16.2 billion revenue and $3.7 billion earnings by 2029.

Uncover how Williams Companies' forecasts yield a $78.79 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming Williams could lift revenue toward about US$18.1 billion and earnings to roughly US$4.4 billion by 2029, yet the latest dividend hike and Transco focused upgrades might either support that growth friendly story or highlight how exposed those expectations are to energy transition and ESG risks, so it is worth comparing these brighter forecasts with more cautious views before you decide where you stand.

Explore 4 other fair value estimates on Williams Companies - why the stock might be worth 15% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Williams Companies research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Williams Companies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Williams Companies' overall financial health at a glance.

Contemplating Other Strategies?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Rare earth metals are the new gold rush. Find out which 31 stocks are leading the charge.

- Find 51 companies with promising cash flow potential yet trading below their fair value.

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.