Does Zscaler's (ZS) EVP Exit Reshape Its AI Security Strategy Or Reinforce Its Zero Trust Focus?

Zscaler, Inc. ZS | 135.28 | -0.16% |

- In April 2026, Zscaler, Inc. announced that EVP of Corporate Strategy and board member Raj Judge resigned effective April 15, 2026, with severance expected under the company’s existing Change of Control and Severance Policy.

- Judge’s departure comes as Zscaler is gaining attention for AI-focused security offerings and industry recognition, including Google Cloud’s 2026 Partner of the Year Award for Security in the Application category.

- Next, we’ll examine how Zscaler’s Google Cloud security award could influence its zero trust and AI-centric investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 38 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Zscaler Investment Narrative Recap

To own Zscaler, you need to believe its Zero Trust cloud platform and AI-focused security can keep winning share even as competition and cloud-provider offerings intensify. The biggest near term catalyst remains broader adoption of its Zero Trust and AI security modules, while a key risk is rising pressure on margins as the company spends to stay ahead. Raj Judge’s resignation appears more of a governance and leadership continuity consideration than a change to that core thesis.

The most relevant recent announcement is Zscaler’s 2026 Google Cloud Partner of the Year Award for Security in the Application category. This aligns directly with its AI and Zero Trust narrative by highlighting traction on a major hyperscaler, which could support customer confidence and deal activity. At the same time, it sits against a backdrop of intensifying competition from larger cloud and security vendors that are expanding their own integrated platforms.

But against this upside, investors should also be aware that intensifying competition from both cloud providers and large security platforms could...

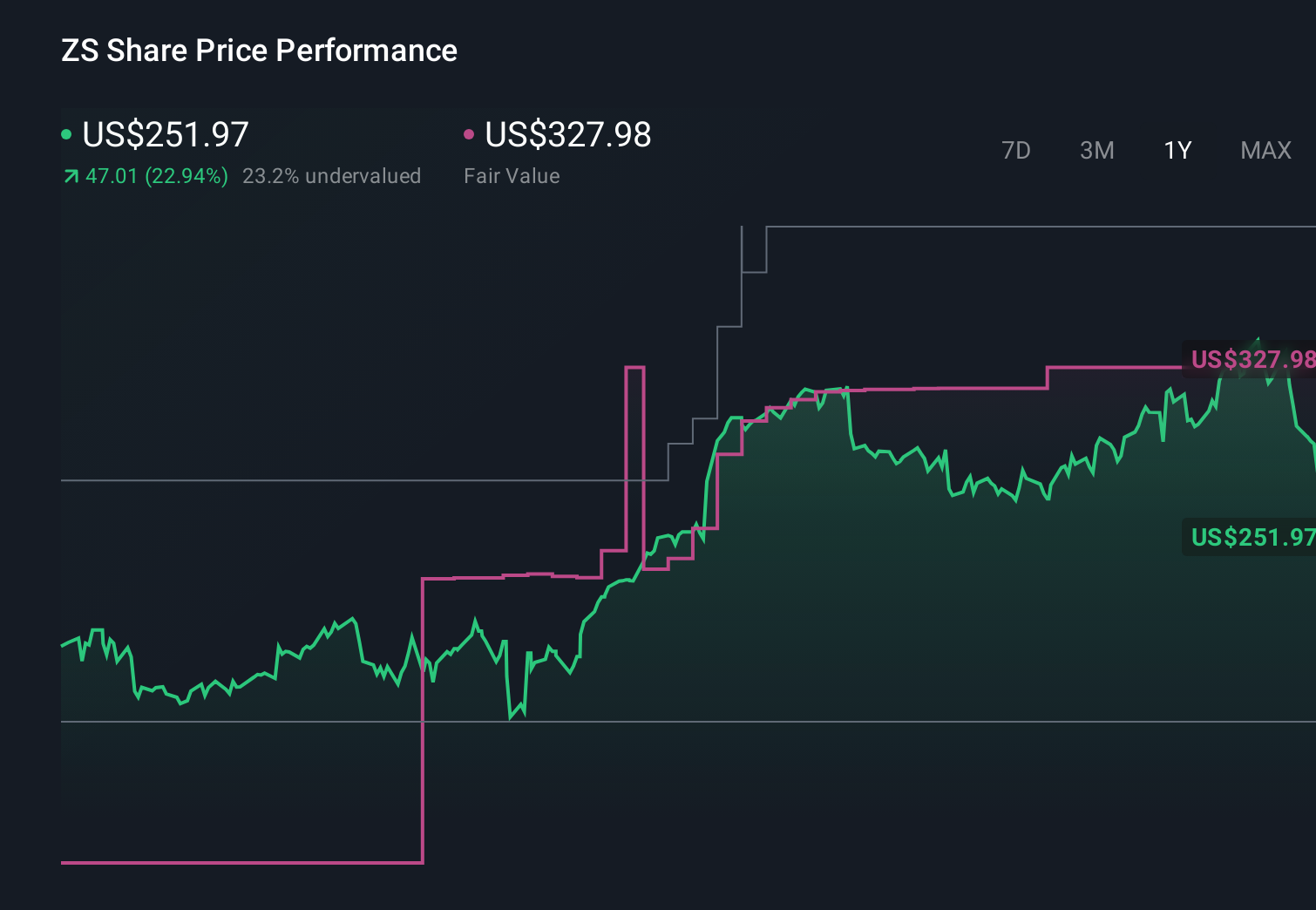

Zscaler's narrative projects $5.2 billion revenue and $152.9 million earnings by 2029. This requires 19.9% yearly revenue growth and about a $220.5 million earnings increase from -$67.6 million today.

Uncover how Zscaler's forecasts yield a $230.45 fair value, a 62% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts paint a far more cautious picture, assuming about 19.7% annual revenue growth and no profitability within three years, which contrasts sharply with the recent Google Cloud win and highlights how differently you might weigh execution and integration risks before this leadership change potentially reshapes expectations.

Explore 8 other fair value estimates on Zscaler - why the stock might be worth over 2x more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Zscaler research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Zscaler research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Zscaler's overall financial health at a glance.

Interested In Other Possibilities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Find 61 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 26 elite penny stocks that balance risk and reward.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.