DoorDash’s Canada, Empire, and SNAP Expansion Might Change The Case For Investing In DoorDash (DASH)

DoorDash DASH | 0.00 |

- In late April 2026, DoorDash expanded DashPass benefits into Canada through an enhanced partnership with Lyft and added more than 1,000 Empire Company grocery and convenience stores across 10 provinces to its marketplace, while also rolling out SNAP/EBT payments for online Kroger grocery orders at nearly 2,700 U.S. locations.

- Together, these moves extend DoorDash’s membership perks beyond food delivery, deepen its presence in everyday grocery spending across North America, and broaden access to online grocery for lower-income households.

- We’ll now examine how the Empire partnership and broader Canadian expansion could influence DoorDash’s investment narrative and long-term ambitions.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

DoorDash Investment Narrative Recap

To own DoorDash, you generally have to believe it can evolve from food delivery into a broader local commerce platform while keeping margins intact. Near term, the key catalyst is whether newer verticals like grocery and retail can sustain profitable growth, while the biggest risk remains rising labor and regulatory pressures on its gig model. The latest Canada and SNAP/EBT expansions support the platform story, but they do not materially change those core risks in the short run.

Among the recent announcements, the Empire Company partnership in Canada looks especially relevant. It sharply increases DoorDash’s grocery and convenience footprint across 10 provinces and brings four of the five largest Canadian grocers onto the platform. For investors focused on catalysts, this move ties directly into the thesis that grocery and everyday essentials can extend order frequency and help justify the premium placed on DoorDash’s scale and membership offerings.

Yet even as these partnerships broaden DoorDash’s reach, investors should be aware of the growing risk that higher labor and regulatory costs could...

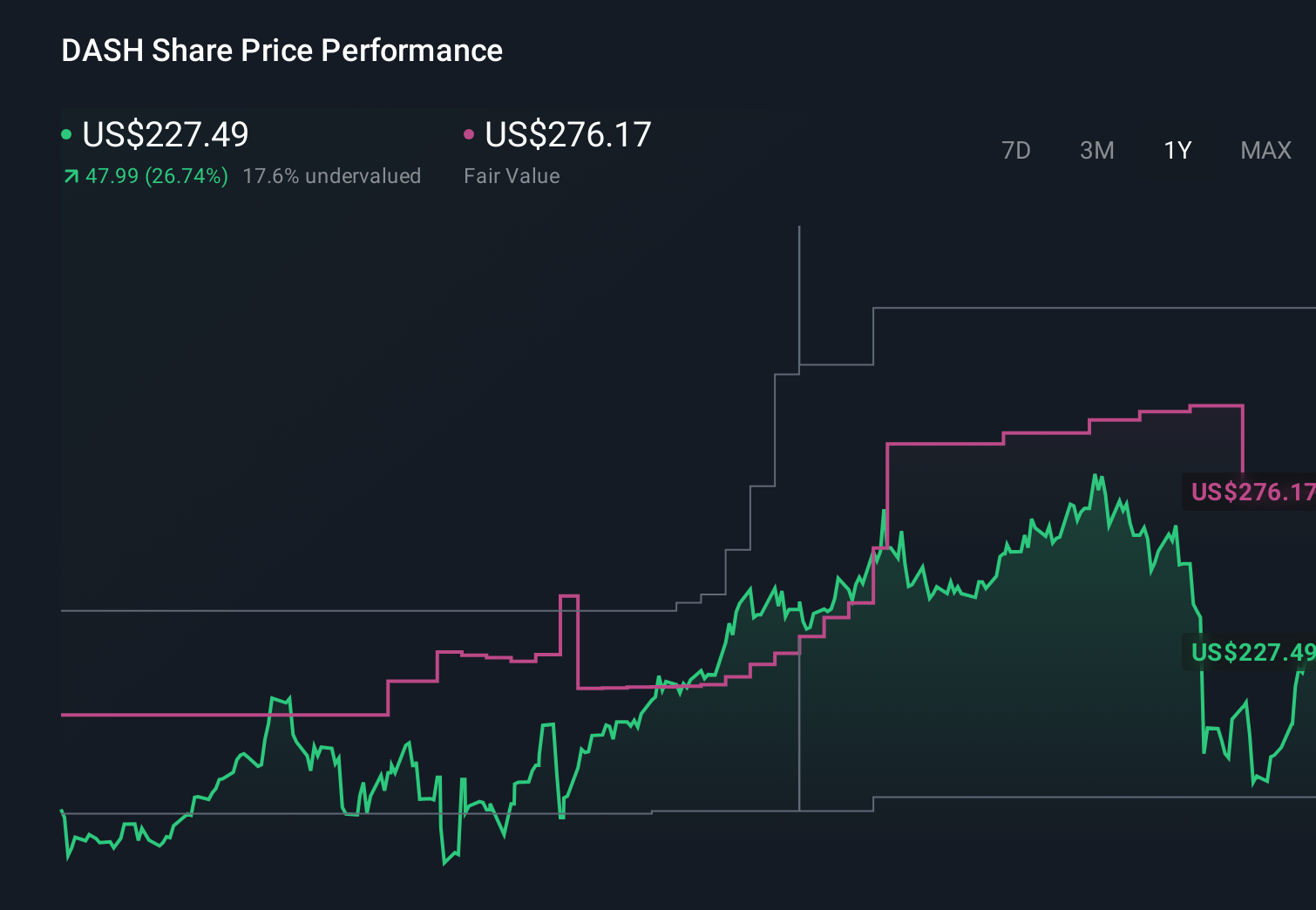

DoorDash's narrative projects $25.2 billion revenue and $3.0 billion earnings by 2029.

Uncover how DoorDash's forecasts yield a $250.93 fair value, a 45% upside to its current price.

Exploring Other Perspectives

By contrast, the most pessimistic analysts were already baking in risks like tougher labor rules while still assuming revenue could reach about US$23.7 billion and earnings US$2.3 billion by 2029, so this latest expansion could push their cautious view to evolve in ways you may want to compare with the more optimistic case.

Explore 13 other fair value estimates on DoorDash - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your DoorDash research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free DoorDash research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate DoorDash's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Uncover the next big thing with 21 elite penny stocks that balance risk and reward.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 18 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.