Dorchester Minerals (DMLP) Stock Looks Strong On Returns But Rich On Earnings

Dorchester Minerals, L.P. DMLP | 0.00 |

Dorchester Minerals has rewarded long term holders with a 165.4% return over the past 5 years. However, at around US$25.83 the stock screens as relatively expensive on Simply Wall St’s broader valuation checks, which may give some investors pause after such a run.

- The 165.4% 5 year return highlights how strongly Dorchester Minerals has rewarded patience, which can raise the bar for what counts as a reasonable entry price today.

- The planned acquisition of approximately 3,100 net royalty acres in the Williston Basin can support long term royalty income, while issuing 850,000 new common units as consideration may introduce dilution risk that matters for valuation.

- With a value score of 2 out of 6, Dorchester Minerals does not currently stand out as a clear bargain on the broader set of valuation checks.

The issue now is whether Dorchester Minerals’ current price still offers an appealing balance between its past returns, new royalty assets, and the relatively low value score.

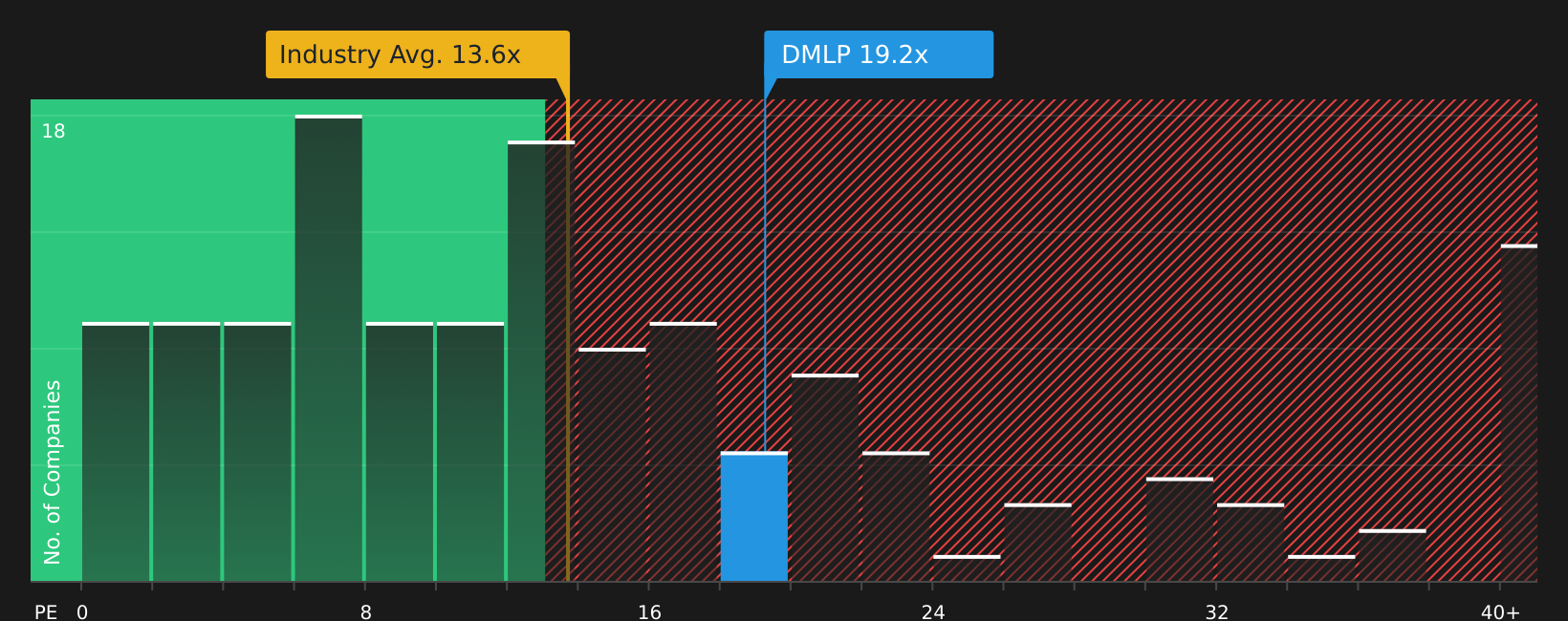

Has Dorchester Minerals Run Too Far on Earnings?

P/E is a useful lens for Dorchester Minerals because its business model is geared around turning royalty income into distributable earnings. At around 18.7x earnings, Dorchester Minerals trades at a clear premium to the Oil and Gas industry average P/E of about 13.4x and a peer group average of roughly 14.5x, so the stock carries a higher earnings multiple than many sector peers.

Despite the pending Williston Basin royalty acquisition, which some investors may see as a support for longer term cash flows, the current P/E still prices Dorchester Minerals above typical sector levels. That premium suggests the market is already assigning a higher value to its earnings stream, leaving less room for investors who prefer entry points closer to industry norms.

Based on the P/E multiple alone, Dorchester Minerals stock currently screens as overvalued compared with both its industry and peer averages.

The Dorchester Minerals Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Dorchester Minerals pick up where the P/E puzzle leaves off. On the Community page, they spell out which future paths for growth, margins and earnings would line up with a stock price that is meaningfully higher or lower than today. Instead of stopping at a single ratio or model output, they describe the future that number relies on so you can watch how Dorchester Minerals' actual progress compares with those underlying assumptions.

If you have a number driven view on whether Dorchester Minerals' planned acquisition of approximately 3,100 net royalty acres in the Williston Basin ultimately delivers on its promise, consider adding your narrative to the Simply Wall St community so others can see how your thesis compares.

Set out your case on Dorchester Minerals' valuation and drivers today, then track how it holds up as new results and updates emerge over time.

Do you think there's more to the story for Dorchester Minerals? Head over to our Community to see what others are saying!

The Bottom Line

Dorchester Minerals currently screens as overvalued on market multiples, with investors paying a premium relative to industry peers for its earnings stream. The low value score underlines that, across broader checks, this is not a clear-cut value opportunity and leaves less margin for error if expectations ease. From here, the key question is whether Dorchester Minerals can sustain the earnings profile and income appeal that justify a higher P/E or whether the valuation eventually settles closer to sector norms.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.