Dorman Products (DORM): Assessing Valuation After Website Upgrade and Ongoing Earnings Outperformance

Dorman Products, Inc. DORM | 0.00 |

Dorman Products (DORM) just rolled out a redesigned website featuring a more robust e-commerce platform. This upgrade is aimed at boosting both customer satisfaction and operational efficiency. The company’s pattern of beating earnings estimates highlights solid ongoing execution.

While Dorman Products’ newly upgraded website is driving buzz, the stock has faced a sharp pullback lately with a 30-day share price return of -16.7 percent. However, the broader picture is brighter as the company boasts a robust three-year total shareholder return of over 50 percent, which points to long-term strength even amid recent volatility.

If you’re looking to spot the next standout, now could be the right time to widen your view and discover See the full list for free.

With shares down in the short term but boasting healthy long-term returns and analyst price targets suggesting upside, the question is whether Dorman Products is undervalued right now or if the market already reflects future growth potential.

Most Popular Narrative: 24% Undervalued

At $131.65, Dorman Products is trading well below the narrative's fair value target of $173.50. This creates the biggest pricing gap in years. The narrative hinges on bold growth assumptions, making it worth a closer look.

The increasing average age of vehicles in North America (now 12.8 years) is supporting sustained, recurring demand for replacement parts. This is fueling year-over-year volume growth, especially in the light-duty business segment, driving top-line revenue and providing long-term visibility into the company's future revenue streams.

Curious about the surprisingly robust growth forecast underpinning that valuation? The full narrative unpacks which financial levers must work together, including sales expansion, margin trends, and a big call on future profit multiples. Want to see what really drives such a high fair value? You might be surprised which fundamentals matter most.

Result: Fair Value of $173.50 (UNDERVALUED)

However, risks remain if electric vehicle adoption accelerates or if persistent supply chain challenges further squeeze margins. These factors could potentially disrupt Dorman’s growth story.

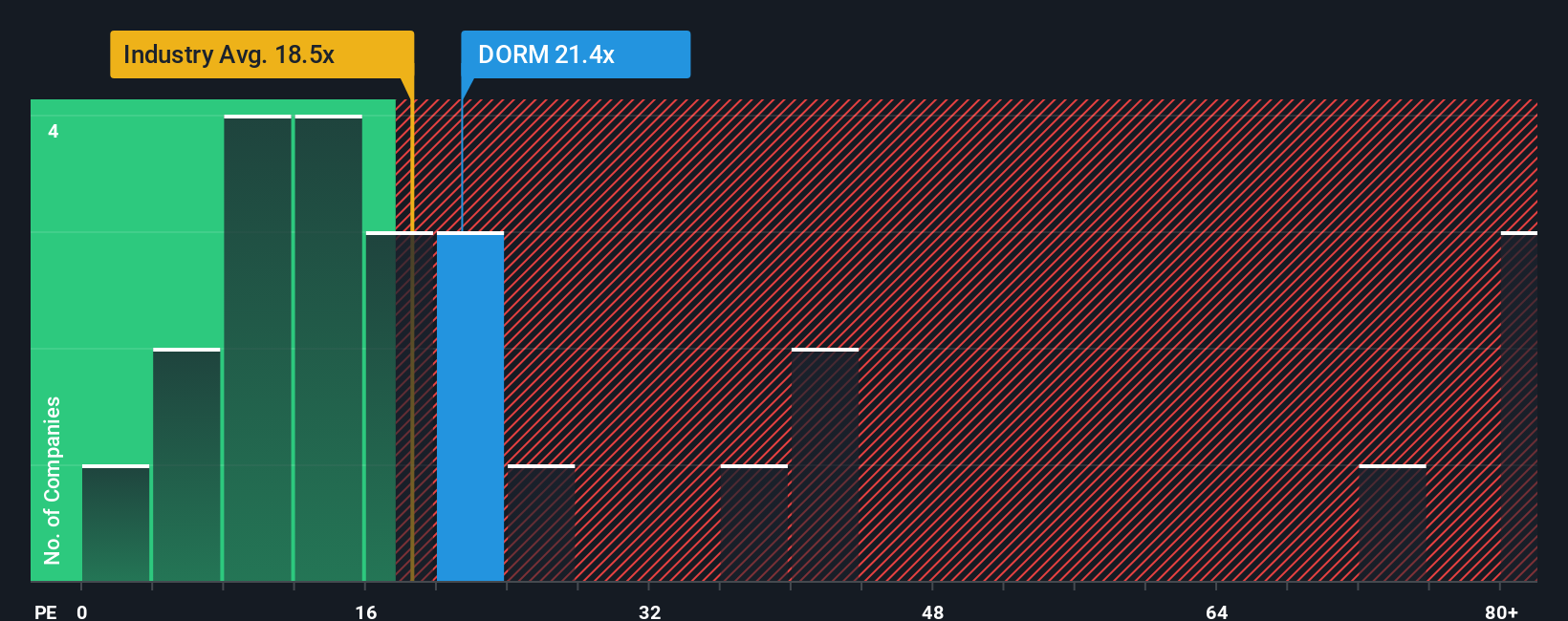

Another View: Price-to-Earnings Signals Valuation Risk

Looking beyond fair value, Dorman Products is trading on a price-to-earnings ratio of 16.3x. This is well above its peer average of 11x and also above the estimated fair ratio of 11.7x. That premium suggests investors have high hopes for future growth, but it leaves little margin for disappointment. Could the market be overestimating Dorman’s prospects?

Build Your Own Dorman Products Narrative

If you’d rather dig into the numbers or craft your own take, you can easily build a custom view of Dorman Products in just a few minutes. Do it your way

A great starting point for your Dorman Products research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Smart Investment Ideas?

Don’t let opportunity pass you by when there are game-changing stock ideas just a click away. Take action now and broaden your investing universe with these handpicked screens:

- Unlock growth potential with these 3584 penny stocks with strong financials, featuring lesser-known companies that could become tomorrow’s standout performers.

- Boost your portfolio’s income with these 14 dividend stocks with yields > 3%, showcasing stocks offering attractive yields above 3 percent.

- Capitalize on AI’s explosive impact in healthcare by tapping into these 30 healthcare AI stocks, where innovation meets solid financials.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.