DT Midstream (DTM) Faces Weaker Q2 EBITDA, Is The Upside Already Priced In?

DT Midstream, Inc. DTM | 0.00 |

DT Midstream (DTM) is in focus as the company is expected to report weaker sequential Q2 EBITDA, with seasonal demand patterns and planned maintenance activities likely weighing on quarterly profitability and investor expectations.

DT Midstream's share price has climbed 8.74% over the past 90 days and 20.78% year to date, while its 1 year total shareholder return of 46.05% points to strong longer term momentum despite near term EBITDA pressures.

If this kind of steady energy infrastructure exposure interests you, it could be a good moment to see what else is out there with the 36 power grid technology and infrastructure stocks

After a strong run and with weaker Q2 EBITDA expected, investors now have to weigh whether DT Midstream still offers enough upside for the risk taken or if the recent move has already done most of the work.

Most Popular Narrative: 5.2% Undervalued

DT Midstream's most followed narrative pegs fair value at $154.20, slightly above the $146.13 last close, which puts more focus on the assumptions behind that gap.

Surging U.S. power demand, driven by electrification, manufacturing onshoring, and data center/AI investments, particularly in Midwest/PJM and MISO regions where DT Midstream operates, provides structural tailwinds for pipeline and storage utilization, directly benefiting long-term revenues and earnings.

Want to see what sits under that fair value call? Revenue stepping up, margins edging higher, and a future earnings multiple that leans far above the sector. The full narrative lays out how those moving parts connect.

Result: Fair Value of $154.20 (UNDERVALUED)

However, the DT Midstream narrative could be challenged if decarbonization or regulatory shifts curb long term gas demand, or if costly modernization only keeps assets treading water.

Another Take On DT Midstream’s Valuation

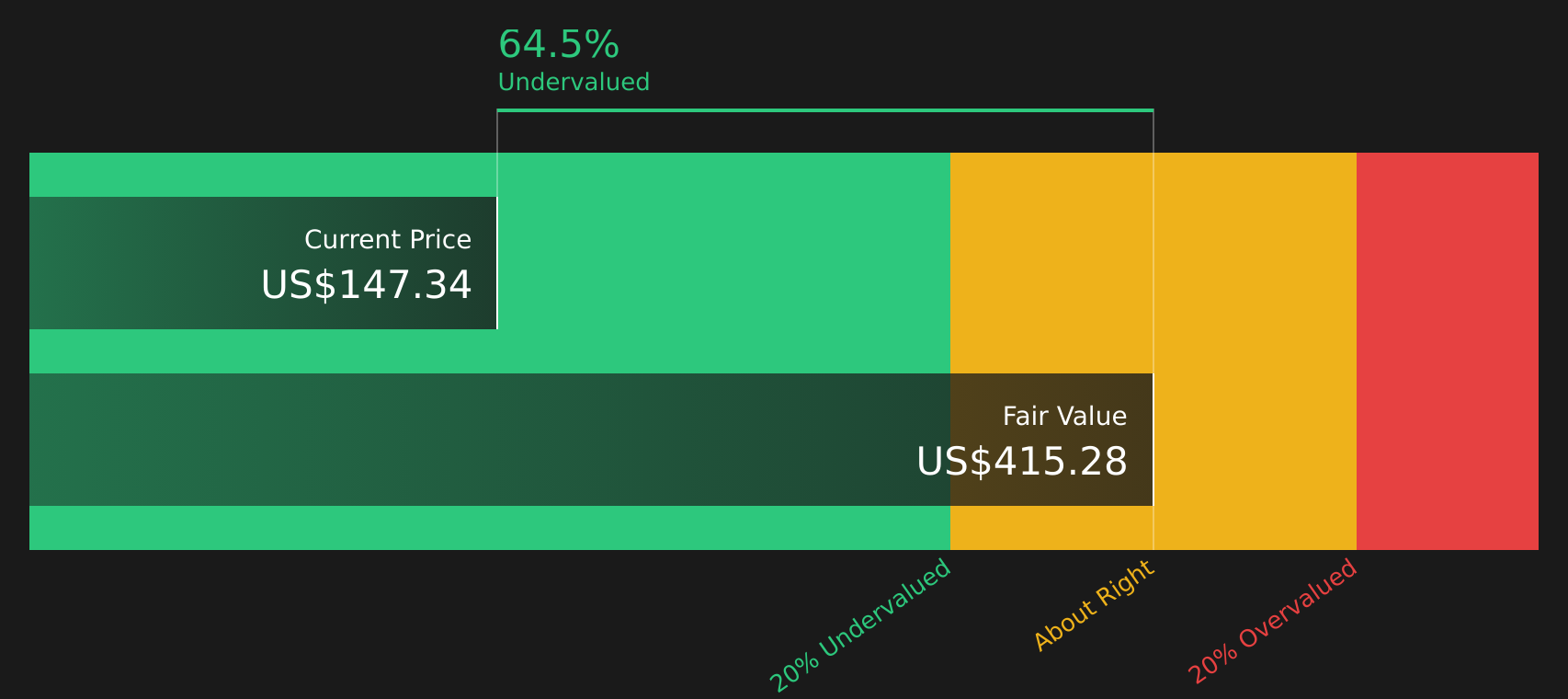

While the Simply Wall St DCF model suggests DT Midstream is undervalued, with an estimate of future cash flow value at $415.28 versus the $146.13 share price, the model itself depends heavily on long term cash flow and discount rate assumptions that can shift as conditions change. How much weight do you want to give that compared with the market’s current pricing?

Next Steps

If the mix of optimism and concern around DT Midstream leaves you undecided, act promptly and compare the numbers, risks, and upside claims with your own view using the 3 key rewards and 1 important warning sign

Looking for more investment ideas beyond DT Midstream?

Do not stop your research with DT Midstream, broaden your watchlist using the Simply Wall St Screener to compare different risk, income, and valuation profiles side by side.

- Target reliable cash generators by checking companies with the solid balance sheet and fundamentals stocks screener (47 results) that pair sturdier finances with room for future decisions.

- Hunt for potential bargains by filtering for 45 high quality undervalued stocks where price and fundamentals may not fully line up.

- Spot early opportunities by scanning the screener containing 18 high quality undiscovered gems that have solid underlying metrics but limited attention from the wider market.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.