DuPont De Nemours (DD) Could Be 23% Undervalued Following WAVE PRO Update

E. I. du Pont de Nemours and Company DD | 0.00 |

WAVE PRO update puts DuPont de Nemours (DD) water tools in focus

DuPont de Nemours (DD) has updated its Water Application Value Engine, WAVE PRO, an online modeling platform that now supports integrated design across ultrafiltration, ion exchange resins, reverse osmosis and nanofiltration systems.

Despite the WAVE PRO announcement, DuPont de Nemours' recent share price momentum has been soft. The stock is down 8.37% over the past 30 days and 5.27% over 90 days. However, its 1 year total shareholder return of 43.85% points to stronger longer term performance.

If this kind of digital tooling in water and infrastructure interests you, it could be worth broadening your watchlist to include 34 power grid technology and infrastructure stocks

For DuPont de Nemours, the recent pullback sits awkwardly next to solid 1 year and multi year returns. The key question now is whether the price is cooling because the business has changed or because sentiment has.

Most Popular Narrative: 23% Undervalued

The most followed narrative on DuPont de Nemours puts fair value at $172.07 per share versus the last close of $132.66, so it treats the recent pullback as out of step with its long term earnings potential.

Persistent strength and investment in Healthcare & Water, driven by surging global demand for clean water solutions and healthcare products, leverages favorable demographic, sustainability, and infrastructure trends to drive above peer organic revenue growth and margin stability. The company's renewed portfolio focus post Qnity spin and recent divestitures in non core segments enables greater resource allocation to high growth specialty businesses, contributing to improved operating margin and increased earnings stability.

Want to see what sits behind that confidence in DuPont de Nemours, from revenue pacing to margin rebuild and future earnings multiples? The full narrative lays out the growth rates, profitability targets, and valuation assumptions that support that $172.07 figure.

Result: Fair Value of $172.07 (UNDERVALUED)

However, this DuPont de Nemours narrative could be derailed if PFAS related liabilities weigh on cash flows or if portfolio changes leave the company with more volatile earnings.

Another View on DuPont de Nemours Valuation

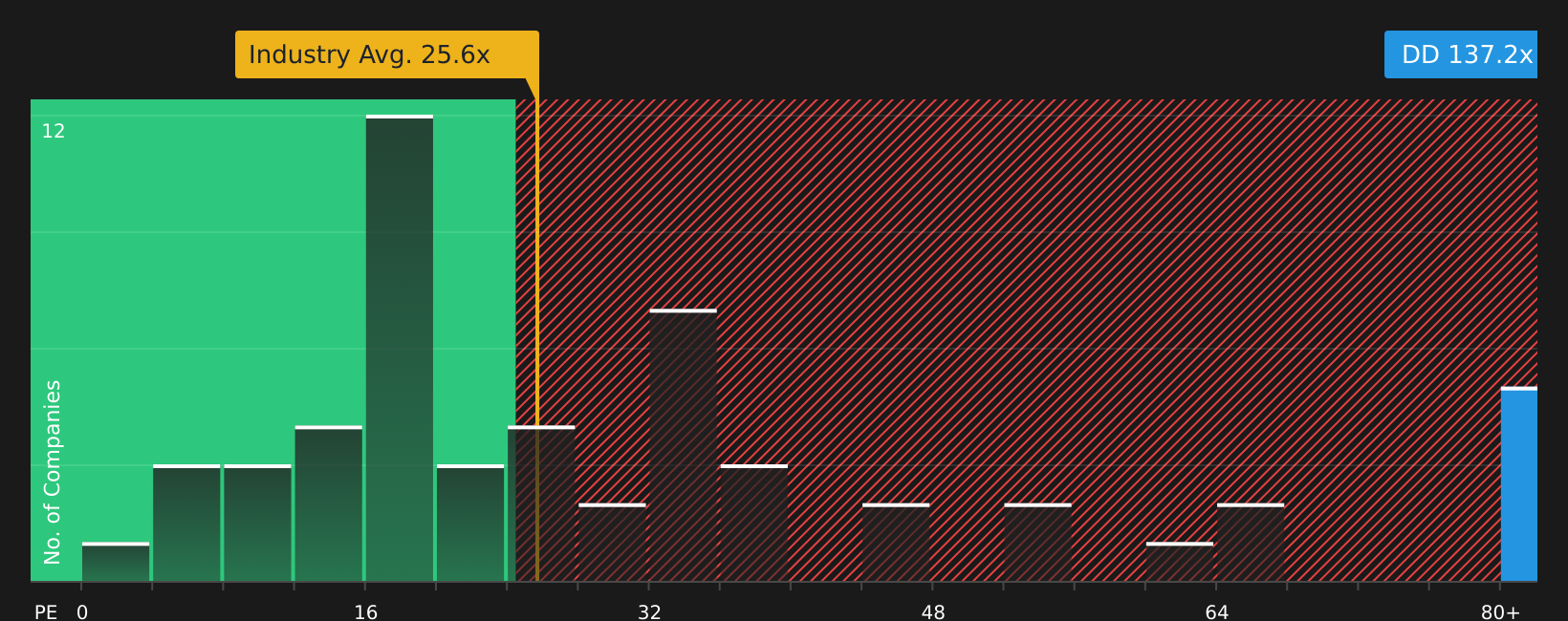

The analyst narrative and DCF style fair value of $172.07 for DuPont de Nemours sits alongside a very different signal from its current P/E. At a P/E of 135.7x versus a fair ratio of 29x and a US Chemicals peer average of 21.1x, the stock screens as expensive, which raises the question of which yardstick you want to lean on.

Next Steps

Given the mixed signals around DuPont de Nemours, it makes sense to move quickly, review the numbers directly, and weigh both the upside and the downside shown in the 4 key rewards and 2 important warning signs.

Looking for more investment ideas beyond DuPont de Nemours?

If DuPont de Nemours has sharpened your focus on quality and valuation, now is a good time to widen your search before the next opportunity moves out of reach.

- Target resilience by checking out companies highlighted in the 80 resilient stocks with low risk scores that may help steady your portfolio when conditions get choppy.

- Hunt for potential mispriced opportunities by scanning the 46 high quality undervalued stocks that line up quality fundamentals with more modest market expectations.

- Strengthen your income stream by reviewing the 8 dividend fortresses that combine higher yields with a focus on durability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.