Earnings Preview: Is Now the Time to Buy Apple? Goldman Sachs Sees a Buying Opportunity Ahead of Earnings After Eight Weeks of Decline

Apple Inc. AAPL | 0.00 | |

Arm Holdings ARM | 0.00 | |

Taiwan Semiconductor Manufacturing Co., Ltd. Sponsored ADR TSM | 0.00 | |

Broadcom Limited AVGO | 0.00 | |

QUALCOMM Incorporated QCOM | 0.00 |

Apple Inc.(AAPL.US) is set to announce its fourth fiscal quarter results for 2025 after the market closes on January 29, Eastern Time. (Note: Apple uses a non-calendar fiscal year system, which begins on October 1 and ends on September 30 of the following year. Therefore, the first fiscal quarter of 2025 corresponds to Q4 of the calendar year 2025.)

According to Bloomberg analysts, Apple’s revenue for the first quarter of fiscal year 2026 is expected to be $138.36 billion, marking an 11% year-over-year increase. Earnings per share are anticipated to be $2.66, reflecting a 13% growth compared to the previous year.

In the previous quarter, Apple delivered impressive results, with both revenue and profit exceeding market expectations. The data shows that Apple's revenue reached $102.466 billion, a year-over-year increase of 7.94%. The gross margin was 47.18%, and net income attributable to the parent company was $27.466 billion. Adjusted earnings per share were $1.85, up 12.81% from the previous year.

The growth in profits was primarily driven by product mix optimization and the high margins of the services segment. In terms of the main business structure, iPhone revenue was $49.025 billion, accounting for approximately 47.85% of total revenue. The services segment generated $28.750 billion, representing about 28.06%. This creates a dual-pillar development model with a strong hardware base and stable cash flow contributions from services.

What to Watch in Apple's Earnings Report: Can iPhone Revenue Hit a Record High? Rising Memory Chip Costs May Pressure Margins

As Apple prepares to release its first-quarter results for fiscal year 2026, key areas of focus for the market include iPhone and services revenue, as well as developments in artificial intelligence and management changes.

- iPhone Revenue: Strong Performance in Peak Season

The first fiscal quarter each year is crucial for Apple, coinciding with the launch of new iPhones in the fall. Historically, this quarter accounts for over 30% of annual revenue, serving as a core performance driver.

Goldman Sachs predicts that Apple's revenue for this quarter will reach $137.4 billion, an 11% year-over-year increase. The iPhone segment is expected to be the main growth engine, with projected revenue of $78 billion, up 13%. This growth is driven by a 5% increase in unit sales, including a 26% surge in shipments in China, and an 8% rise in average selling price (ASP).

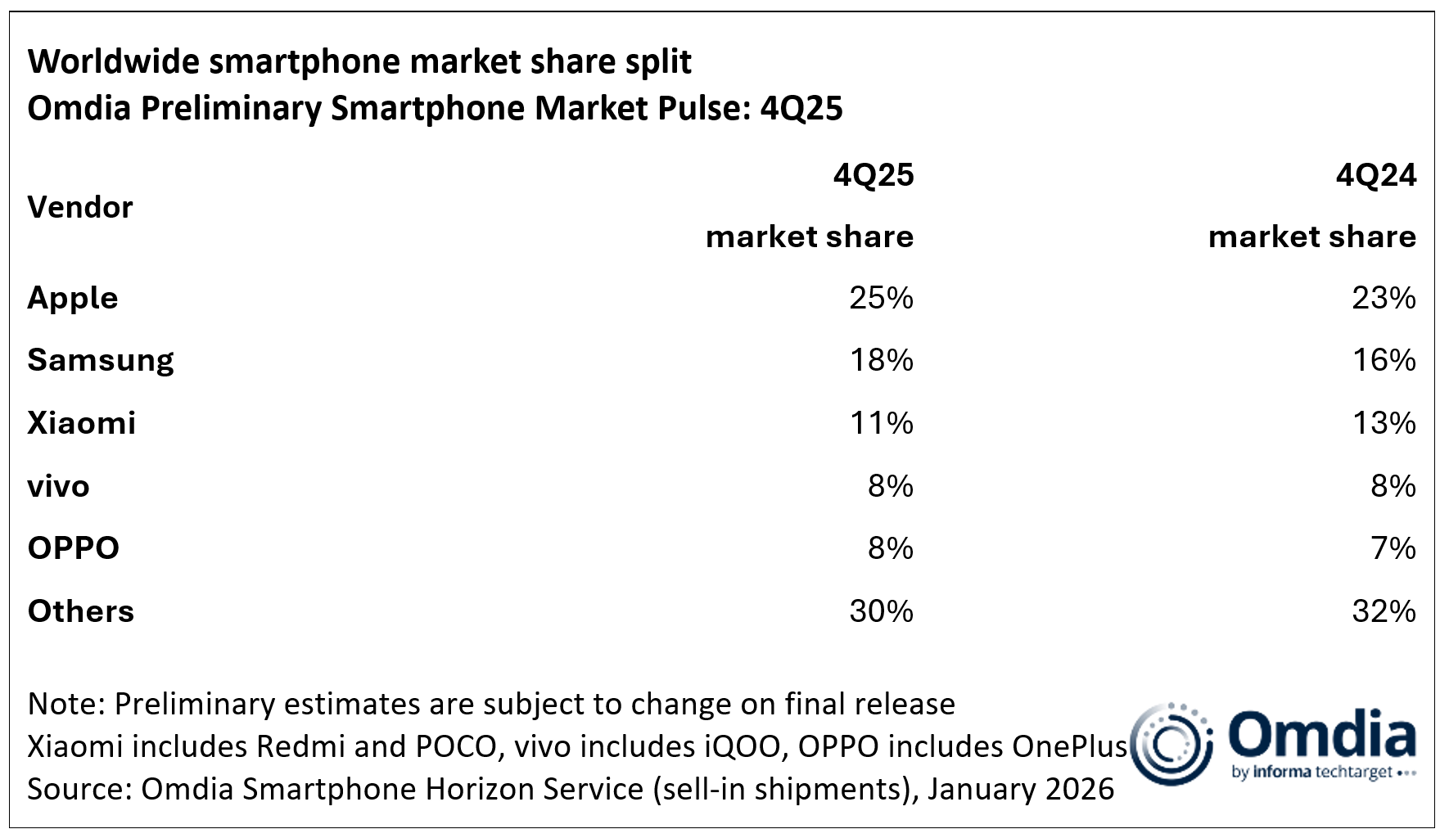

Data from Omdia supports the strong performance of the iPhone, showing a 4% year-over-year increase in global smartphone shipments in Q4 2025. Apple achieved a 25% market share, the highest for the quarter, and maintained its position as the global annual sales leader for the third consecutive year, thanks to strong demand for new and existing models.

- Services Revenue: The Only Clear Structural Growth Source

While the iPhone remains a major revenue contributor, the services segment is the sole clear structural growth highlight in this earnings report.

Goldman Sachs forecasts a 14% year-over-year increase in services revenue, reaching $30 billion. Although App Store revenue growth is expected to slow to 7% in Q1 2026, the overall growth is driven by factors like traffic acquisition costs (TAC), iCloud+, AppleCare+, and subscription services.

Addressing investor concerns about App Store third-party payment issues and macroeconomic impacts, Goldman Sachs offers a positive outlook: iCloud+ is set to benefit from increased data storage demand due to AI feature adoption and high-quality media needs; Apple TV+ subscription price hikes will further boost revenue; and improvements in Google search traffic will support long-term TAC revenue growth, highlighting the user retention advantage of browser searches over AI chatbots.

- AI Initiatives: Major Siri Overhaul Targeting Core AI Entry Point

Apple's moves in AI are drawing attention. Recently, Apple announced plans to upgrade Siri into an AI chatbot, aiming to establish a core AI strategic entry point. Previously, Apple collaborated with Google to use the Gemini model to bolster Siri's next-generation capabilities, addressing its AI model shortcomings and supporting the integration of AI across the iOS/App Store ecosystem and iPhone 18 promotion.

Wedbush anticipates the new Siri will launch in March or April, competing with products like ChatGPT. Apple also plans to introduce AI-driven subscription services this summer and recruit external AI talent to enhance its technical capabilities.

- Management Stability: Cook to Remain CEO Through 2027 to Advance AI Strategy

Amid rumors of Tim Cook's imminent departure, analysts have refuted these claims, asserting he will remain CEO until at least the end of 2027. This period is critical for Apple to formulate and execute its AI revolution strategy. The company is adopting an aggressive approach by attracting top external AI talent to strengthen its technological prowess.

- Potential Risks: Rising Memory Chip Costs May Pressure Margins

In 2025, global smartphone shipments are expected to reach 1.25 billion units, a 2% year-over-year increase, reflecting a "low-to-high" recovery trend. However, rising memory costs and supply shortages could constrain industry growth, with LPDDR4/5 DRAM supplies particularly tight. Citi has lowered Apple's target price to $315, predicting a 2026 average price increase of 88% for DRAM and 74% for NAND. If DRAM procurement costs rise by 50%, Apple's gross margin could be pressured by 100 basis points.

UBS also warns of a potential 50-100 basis point downside risk in gross margin guidance for the June and September quarters. Nonetheless, Apple's premium positioning and supply chain advantages can mitigate these impacts, with long-term growth resilience supported by AI upgrades and the launch of a foldable iPhone.

Apple's Stock Declines for Eight Consecutive Weeks! Goldman Sees a Buying Opportunity Before Earnings

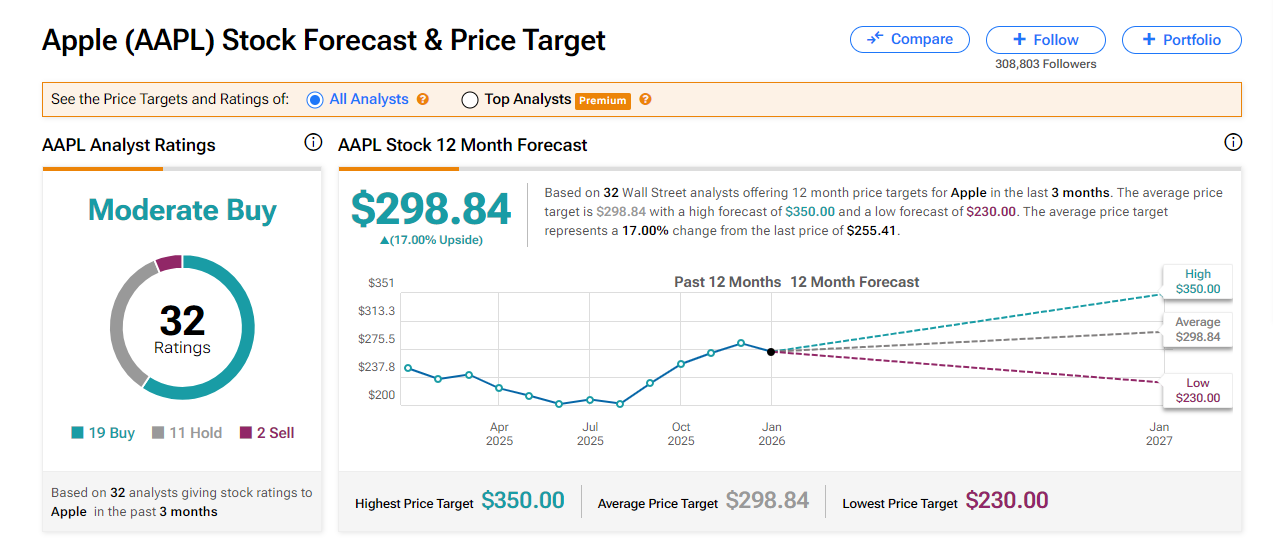

According to the latest data from TipRanks, several major Wall Street banks have raised their price targets for Apple ahead of its earnings report. Currently, 59% of institutions have a "buy" rating, with an average price target of $298.84 and a high of $350 per share.

Is It Time to Buy Apple? Goldman Says Recent Weakness Presents a Buying Opportunity

Apple's stock has fallen for eight consecutive weeks, and Goldman Sachs believes this presents a buying opportunity before the earnings report. They are optimistic about Apple's F1Q26 performance, expecting iPhone revenue to grow by 13% year-over-year. Key drivers include the ongoing upgrade cycle, the anticipated launch of foldable phones, and AI feature integration. Apple can offset memory chip cost pressures through supply chain management, product redesigns, and price increases.

Goldman forecasts earnings per share (EPS) of $2.66, aligning with market consensus, and a gross margin of 47.7%, within the midpoint of the company's guidance, accounting for $1.4 billion in tariff costs.

iPhone 17 Leads the Way, UBS Expects Better-Than-Expected Q1 FY26 Results

The iPhone 17 series has shown exceptionally strong market reception. UBS projects Apple's iPhone revenue will reach approximately $79 billion, a 14% year-over-year increase, surpassing the previous estimate of $77.58 billion and the market consensus of $78.5 billion. The average selling price is expected to rise to around $930 due to a more premium model mix, leading to an optimistic outlook for the quarter.

This better-than-expected performance is attributed to two main factors: the technical upgrades in the iPhone 17 have significantly driven market demand, and Apple may have preemptively ramped up production to lock in costs amid rising memory prices (DRAM and NAND), slightly shifting sales forward within the quarter.

Focus on Related Investment Targets

With Apple's earnings report approaching, which stocks in the Apple supply chain should investors keep an eye on?

- ARM Holdings PLC Sponsored ADR(ARM.US)

- Taiwan Semiconductor Manufacturing Co., Ltd. Sponsored ADR(TSM.US)

- Broadcom Limited(AVGO.US)

- QUALCOMM Incorporated(QCOM.US)

- Micron Technology, Inc.(MU.US)

- Texas Instruments Incorporated(TXN.US)

Apple-Related ETFs:

Investors may consider the following ETFs:

- Direxion Daily AAPL Bull 2X Shares(AAPU.US)

- GraniteShares ETF Trust GraniteShares 2x Long AAPL Daily ETF(AAPB.US)

- T-Rex 2X Long Apple Daily Target ETF(AAPX.US)

- Direxion Shares ETF Trust Direxion Daily AAPL Bear 1X Shares(AAPD.US)

These stocks and ETFs provide various ways to gain exposure to Apple's performance and its broader ecosystem.