EastGroup Properties (EGP) Stock Could Be 6.9% Undervalued After Strong Results

EastGroup Properties, Inc. EGP | 0.00 |

EastGroup Properties (EGP) is back in focus after reporting higher year over year revenue and net profit, alongside strong operating efficiency and a top tier financial health ranking within Residential & Commercial REITs.

At a share price of $199.97, EastGroup Properties has eased slightly over the past month with a 1 month share price return of down 2.5%. Its 90 day share price return of 9.2% and 1 year total shareholder return of 20.6% point to momentum that has generally been building alongside improving financial metrics and increased institutional interest.

If EastGroup Properties has you looking closer at real asset exposure, it can be useful to see what other listed owners and operators are doing with capital and growth. To broaden your search across high conviction opportunities backed by management, check out 20 top founder-led companies

With EastGroup Properties combining rising revenue and net profit, strong financial health, and increased institutional interest, the key question now is whether the current US$199.97 price leaves upside on the table or if the market is already pricing in future growth.

Most Popular Narrative: 6.9% Undervalued

With EastGroup Properties last closing at $199.97 against a narrative fair value of $214.89, the current pricing sits a step below that central estimate, and the narrative turns on what growth and margins might look like several years out.

Structural US population growth and migration to Sunbelt markets continues to underpin robust demand for modern industrial/logistics properties, directly benefiting EastGroup's core portfolio and positioning the company for sustained revenue and NOI growth as these regions outpace national averages. Persistent e-commerce expansion and ongoing supply chain modernization are ensuring elevated leasing spreads and high occupancy in EastGroup's infill, last-mile logistics facilities, supporting above-average rental rate growth and driving resilient net margins.

Want to understand why this fair value sits above the current price? The narrative leans on firm revenue expansion, healthy margins, and a richer future earnings multiple. Curious which specific growth path and profit profile justify that view? The full narrative lays out the assumptions line by line.

Result: Fair Value of $214.89 (UNDERVALUED)

However, the EastGroup Properties narrative could be challenged if tenant health weakens in key regions or if sustained high interest rates restrict affordable capital for new projects.

Another View: What EastGroup Properties’ P/E Is Signaling

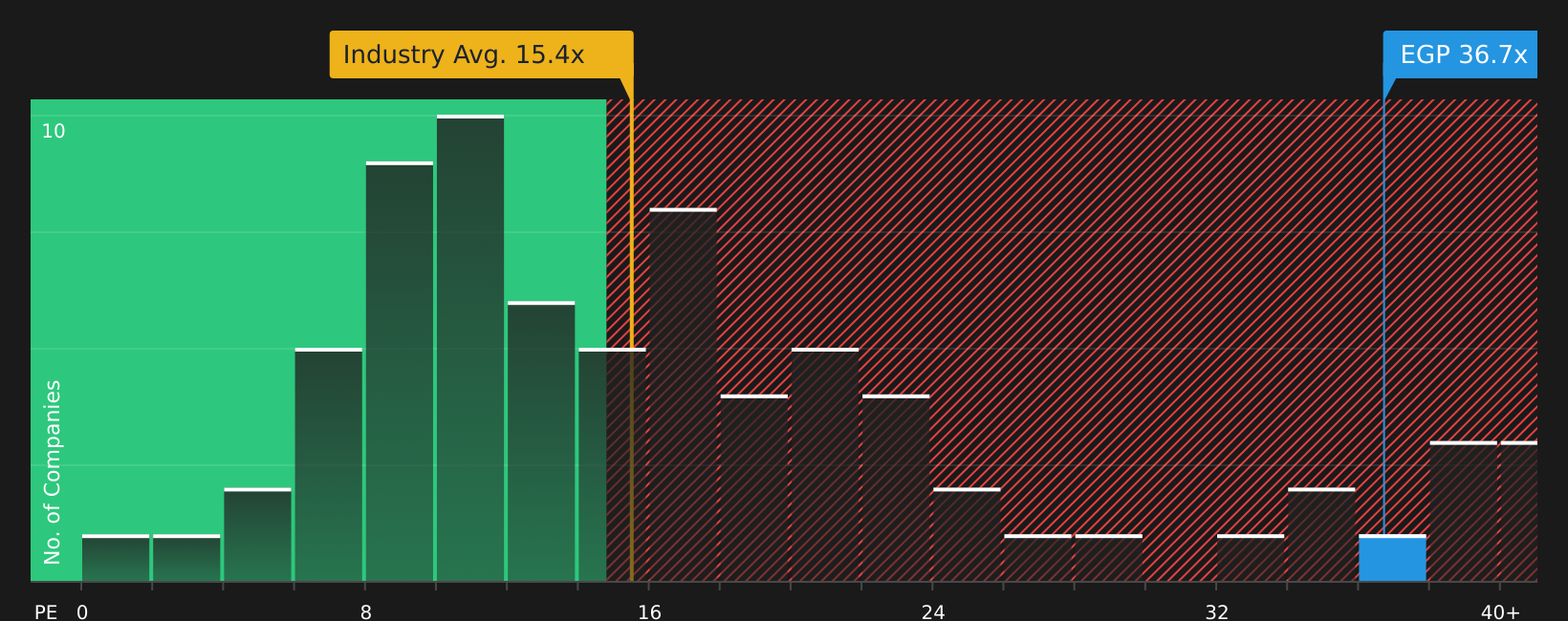

While the fair value narrative points to EastGroup Properties trading about 6.9% below a $214.89 estimate, the current P/E of 36.7x tells a different story. It sits above the estimated fair ratio of 34x, the US Industrial REITs peer average of 25.9x, and the broader global Industrial REITs average of 15.4x. This suggests the stock carries a clear valuation premium that could either compress or be sustained depending on how future results line up with expectations.

For a closer look at how this valuation gap is built up from the earnings multiples and fundamentals, and what that might mean for risk or opportunity, see the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With a mix of positives and concerns around EastGroup Properties in mind, now is a good time to review the data directly and form your own stance, then weigh both sides by checking the 3 key rewards and 1 important warning sign

Looking for more investment ideas beyond EastGroup Properties?

If EastGroup Properties has sharpened your focus on quality, do not stop here. Use the Simply Wall St screener to uncover more targeted opportunities across the market.

- Target potential mispricing by scanning for companies trading below their implied value through the 45 high quality undervalued stocks

- Strengthen your income stream by reviewing companies that offer robust yields and payout profiles via the 8 dividend fortresses

- Prioritise resilience by finding companies with healthier balance sheets and fundamentals using the solid balance sheet and fundamentals stocks screener (48 results)

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.